Hira Saeed

Hira Saeed

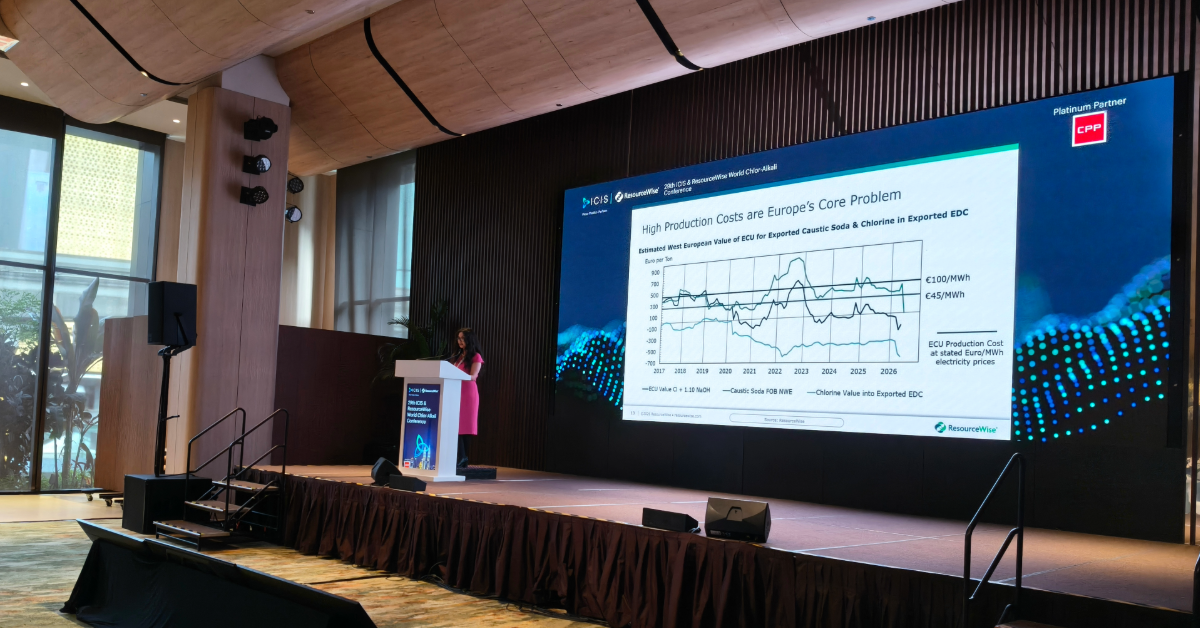

World Chlor-Alkali Conference Day 1 Debrief: Global Markets Adjust to a More Complex Landscape

Day 1 of the World Chlor-Alkali Conference brought together market experts, producers, and industry participants to examine how chlor-alkali, PVC,...

PET and Raw Materials: 2025 Review and 2026 Outlook

The global polyester value chain entered 2025 under mounting pressure, shaped by chronic overcapacity, unsustainably low profitability, and...

1 min read

Glycols and Glycol Derivatives: 2026 Market Outlook

Macroeconomic and Industry Environment: Slow Growth and Structural Length Global macroeconomic indicators suggest a subdued yet moderately improving...