George West

George West

Bio-Bunker Premiums Rebound as Oil Market Disruption Eases

45Z Final Rules are Coming in November. Now is the Time to Plan.

.png)

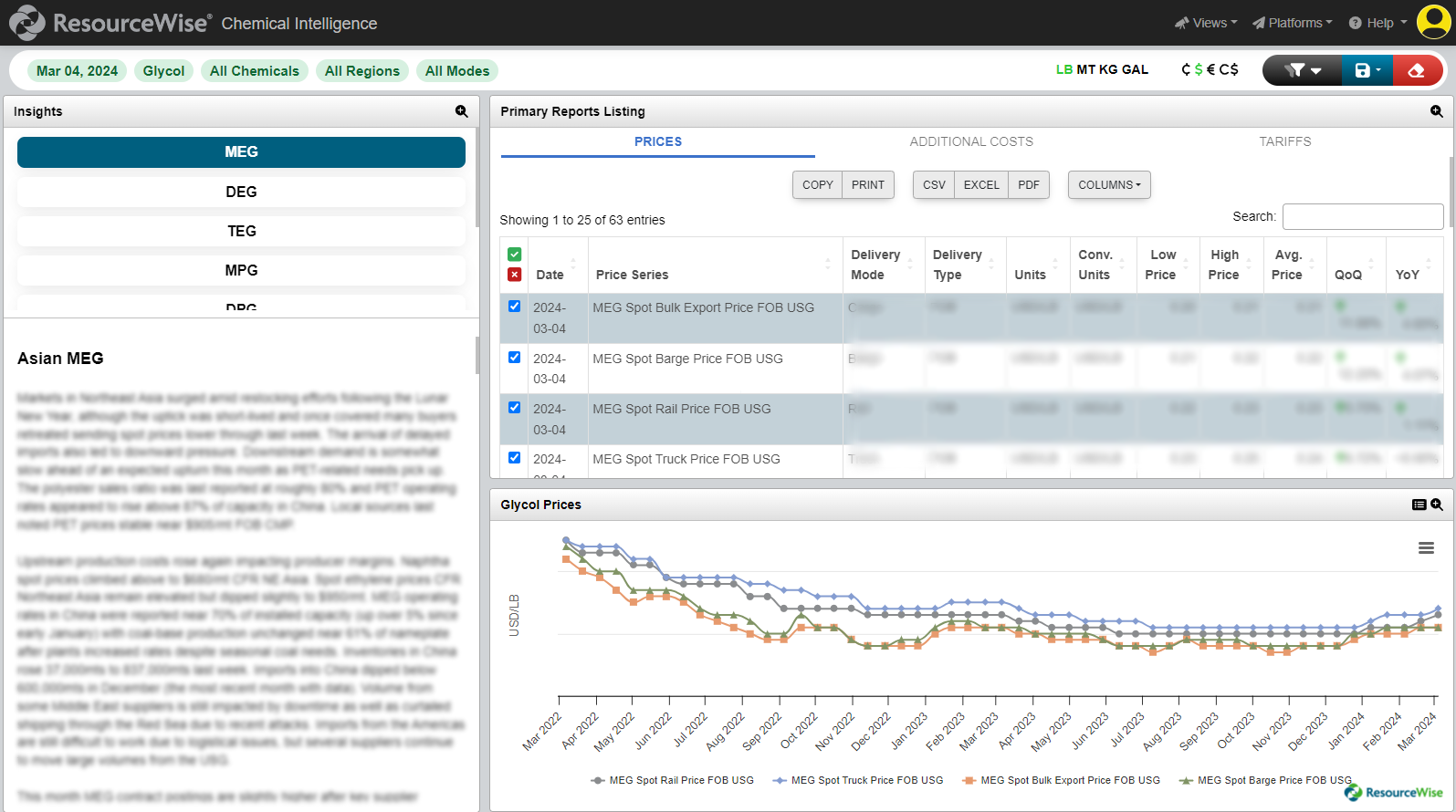

Glycols and Glycol Derivatives: 2025 Market Review

Monoethylene Glycol (MEG) A Tight Start to 2025 North American MEG entered 2025 in a relatively tight and higher-priced position. MEGlobal’s...

Glycolipid Market Expands as Production Technology Improves

Several biotechnology and specialty chemical companies are ramping up marketing and commercialization of microbial-based surfactants, especially...

Methanol, Glycols, and Solvents Market Intelligence: Life on the ChemEdge360

Global trade and markets for methanol, glycols, and solvents became more visible and transparent. With the launch of its second chemicals pricing,...