William Bann

William Bann

What the UCO Market Reveals About Crude Tall Oil Demand

What's Next for Asia's Largest Wood Pellet Supplier?

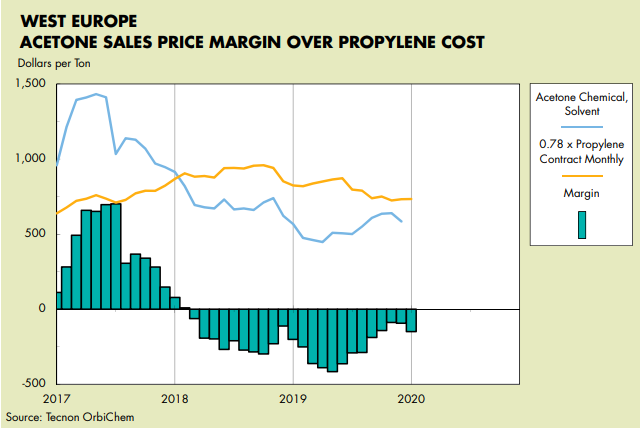

Reversal of Fortune for Acetone?

Acetone prices have been in perpetual hell for the last 18 months - values plunged to historical lows in mid to late 2019, falling significantly...

As the Chinese UPR Market Starts to Put Out Green Shoots: the US and Europe Face Frosty Demand

The Chinese UP resin market started to show some recovery in March after coming to a standstill in late January and remaining virtually shut down...

Coronavirus - What Has Happened So Far?

The novel coronavirus, a variant of the virus that caused SARS and MERS, was first identified in Wuhan in Hubei province, China, in December 2019. By...