3 min read

The forest products industries faced a year of significant change in 2024, marked by shifting market dynamics and unexpected challenges. From fluctuating demand and pricing to an increasing emphasis on biofuel innovations, the sector underwent remarkable transformations.

As part of our annual tradition, ResourceWise is proud to share our key insights and forecasts for the year ahead. Here are eight pivotal predictions that will shape the forest products industry in 2025.

2025 Predictions

-

The Year of Supply Chain Transparency

2025 is poised to become a pivotal year for supply chain transparency, particularly for forest product companies and landowners. A wave of new regulations is on the horizon, coupled with the gradual rise of voluntary compliance requirements. What does this mean?

Although the European Deforestation Regulation (EUDR) was delayed until January 2026, it remains a priority, with the EU Parliament reaffirming its commitment to the initiative. While the industry has gained an additional year to comply, the pressure to adapt is building. Moreover, end users of forest products, especially consumer facing companies, are committing to increased transparency.

Voluntary carbon markets continue to play a key role in corporate ESG strategies. While physical decarbonization is considered more effective and credible, there isn’t enough supply to meet the growing demand. As a result, the market for carbon credits and offsets—often criticized for credibility issues—will require greater transparency to thrive.

At the same time, the traditional timberland value model, centered on stumpage, is evolving (see Prediction 3). Landowners will increasingly need to adopt voluntary carbon standards to unlock new revenue streams from their forests. This shift will demand heightened transparency, marking a significant transformation in the industry. -

Eastern and Western Economies Drift Further Apart Amid Renewed Trade Tariffs

The decoupling of Eastern and Western Hemisphere economies is set to continue, driven by a potential “second wave” of Trump-era trade tariffs targeting heavily subsidized economies. This is in addition to European trade actions banning or penalizing imports of Chinese made goods, most notable electric vehicles. This shift could have several key implications:

-

- China’s paper industry: Already facing overcapacity, China’s paper sector may experience further declines in demand if manufacturing offshoring accelerates. To prevent deflation, the country will need to address its existing excess production capacity.

-

- European investment in North America: European companies, grappling with the risks of deindustrialization due to stringent regulations and energy policies, are increasingly diversifying beyond the EU. For example, SAICA’s plans to establish a paper mill in Ohio, highlights this growing trend of investment in the North American market.

- European investment in North America: European companies, grappling with the risks of deindustrialization due to stringent regulations and energy policies, are increasingly diversifying beyond the EU. For example, SAICA’s plans to establish a paper mill in Ohio, highlights this growing trend of investment in the North American market.

-

-

Timberland Values Pivot to Carbon Amid Shifting Market Dynamics

The value of timberland is increasingly shifting from traditional stumpage uses to carbon and environmental services. In many cases, new timberland investors are assigning substantial value to carbon as a key factor in underwriting timberland assets. This trend is largely driven by stagnant wood fiber markets and long-term forecasts showing that tree growth will far exceed harvest rates in the years to come.

-

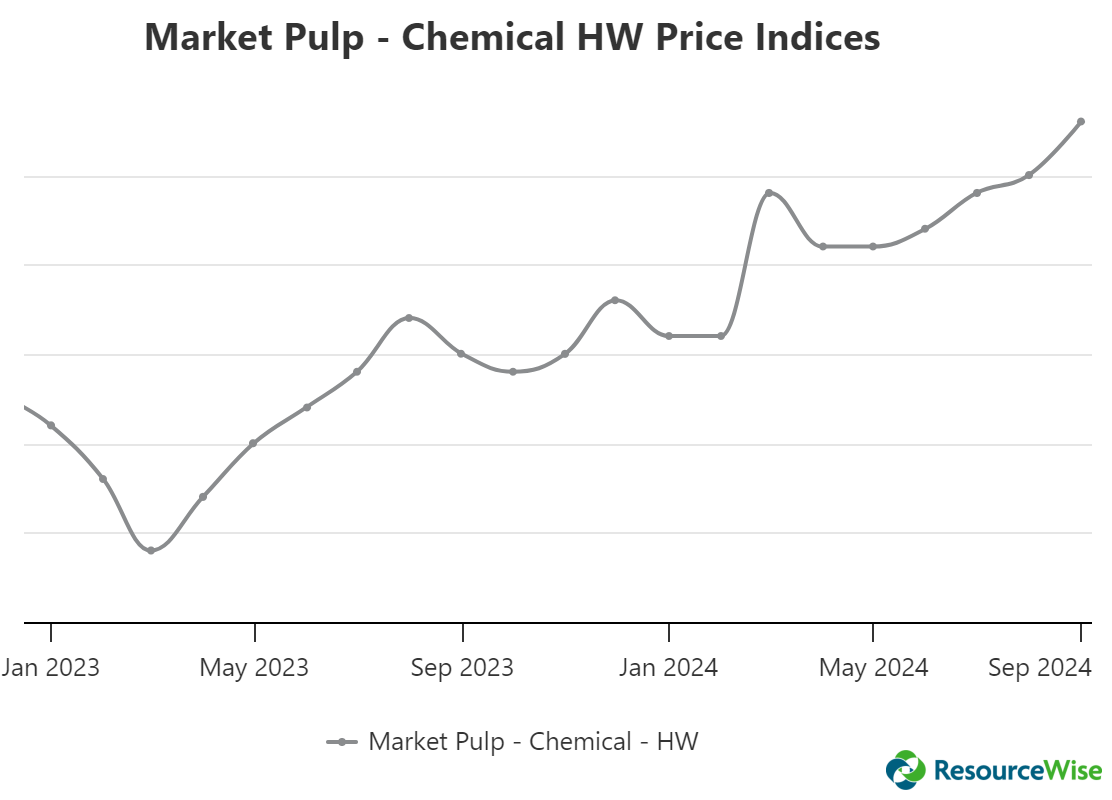

The U.S. South Will Attract Global Attention with Competitive Pulp Mill Prospects

The U.S. South boasts the lowest risk-adjusted softwood costs globally, making it a prime location for investment. Combined with low energy costs, growing markets for pulp mill byproducts such as carbon CDRs and e-fuels, and its proximity to the world’s largest consumer market, the region is set to attract significant investment in pulp mills, including an announcement for a greenfield pulp mill. Many domestic companies (Green Bay, Georgia Pacific) have announced significant investments — will a foreign company follow with the first North American greenfield pulp mill in 20 years? -

Lumber Market to Rebound in Late 2025 with New Mill Announcements on the Horizon

The lumber market is projected to rebound in the latter half of 2025, driven by anticipated declines in interest rates and a resurgence in construction activity. Across North America, over 2 billion board feet of production capacity were shut down in 2023 and 2024. By the end of 2025, we expect announcements of new mill openings to signal a revival in the industry. -

Global Investors Will Eye the U.S. Forest Products Market Due to Competitive Advantages

The U.S. forest product manufacturing sector is attracting significant interest, and we expect a major acquisition by a Latin American or European forest products company in 2025. The U.S. market remains highly appealing to investors, particularly those in the forest products industry, due to its abundant and competitively priced wood raw materials. With the economy growing at a steady 3%, the U.S. provides a favorable environment for investment. Additionally, concerns over tariffs are encouraging companies to establish a foothold in the U.S. market to avoid being excluded. In contrast, Europe faces slower economic growth and a regulatory and business climate that shows little sign of improvement. -

High Fiber Costs in the Nordics Will Force Pulp Mill Closures Amid Russia-Ukraine Crisis

Persistently high wood fiber costs in the Nordics, driven by the ongoing Russia-Ukraine war, are expected to lead to the closure of pulp mills in the region. The industry will be compelled to adjust its operations to align with the limited availability of affordable fiber. -

AI Won’t Take Over the World

While AI won’t completely take over the world, it does represent a transformative shift in productivity—arguably even more significant than the personal computer revolution. This shift will further widen the valuation gap between industries that adopt AI and those that resist it. If our industry fails to embrace AI, we risk being left behind. The consequences will be clear: diminished investment, declining efficiency, and a resulting drop in both profits and growth.

Keep Up with Developments in the Forest Products Market

Despite the possibility of ongoing fluctuations in the near future, we are optimistic to see what lies ahead for the forest products industry in 2025. To stay updated on all the latest discussions surrounding the global forest products industry, be sure to subscribe to our weekly blog updates.

The Pulp Mill as a Biorefinery: Unlocking New Revenue Streams

Bio-Bunker Premiums Rebound as Oil Market Disruption Eases

Reviewing ResourceWise’s 2025 Forest Products Industry Predictions

Each year, ResourceWise publishes a set of predictions outlining how we expect the forest products industry to evolve over the coming year. As we do...

Unlocking the Power of FIA Data with ResourceWise’s Timber Supply Analysis 360 and Carbon 360

The USDA Forest Service's Forest Inventory and Analysis (FIA) program is the backbone of forest resource intelligence in the United States. Described...

Reviewing ResourceWise's 2024 Forest Products Industry Predictions

As we near the end of 2024, it's time to reflect on the insightful predictions made by ResourceWise's CEO, Pete Stewart, and Chief Revenue Officer,...