Recession still looms over the economy. But a few small upticks in economic indicators show some life as we move into the 4th quarter of 2023.

Manufacturing Contraction Slows Down with Modest Rise in Index

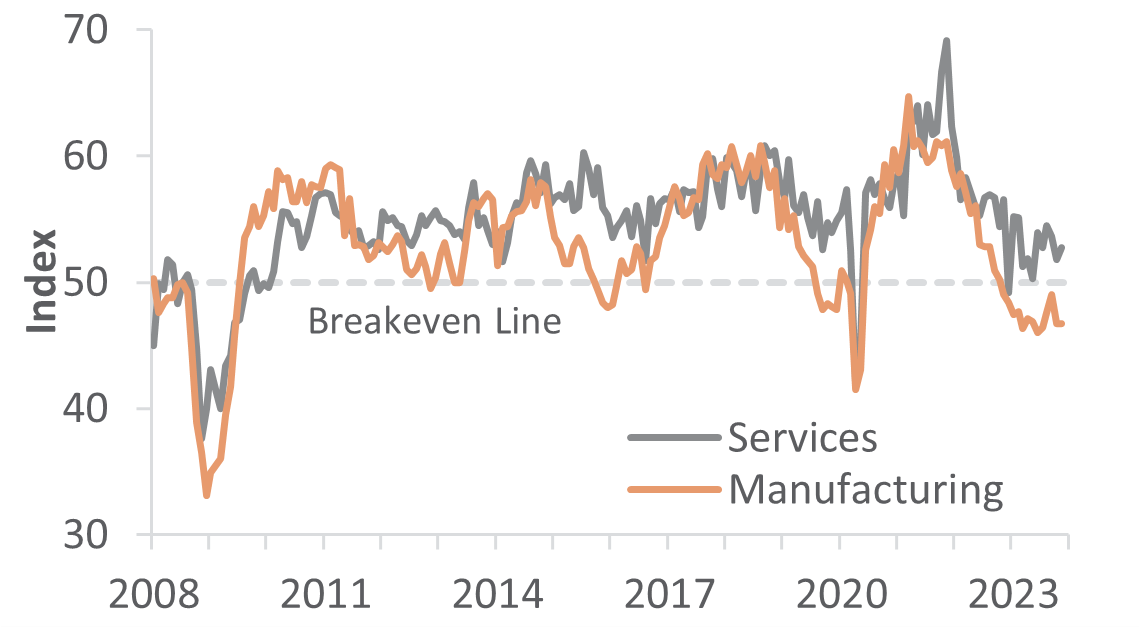

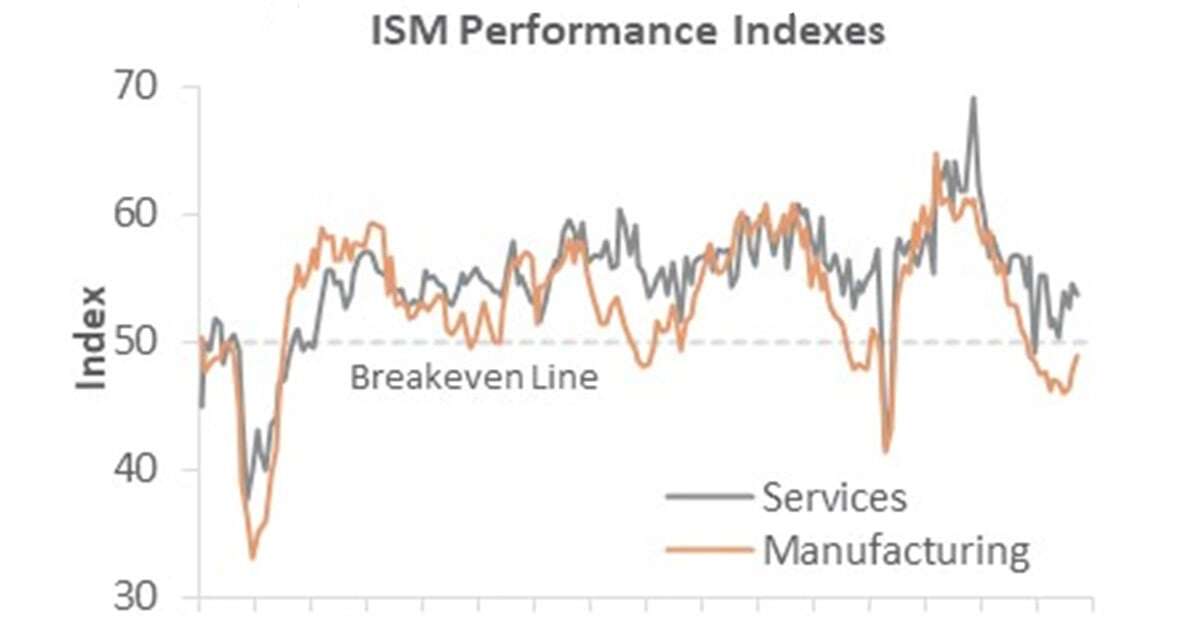

The Institute for Supply Management’s (ISM) monthly sentiment survey of U.S. manufacturers reflected a slower contraction in the sector during August.

The PMI registered 47.6%, up 1.2PP from July’s reading. 50% is the breakpoint between contraction and expansion.

All subindexes remained at or below 50. The largest changes occurred among the following:

- Prices Paid (+5.8PP).

- Employment (+4.1PP).

- Slow deliveries (+2.5PP).

Concurrent activity in the services sector accelerated +1.8PP to 54.5%. Order backlogs (‑10.3PP), inventories (+7.3PP), and inventory sentiment (+4.9PP) exhibited the largest changes.

“Sixty-two percent of manufacturing GDP contracted in August, down from 92% in July, a positive trend for the economy,” ISM’s Timothy Fiore remarked. Furthermore, manufacturing PMI numbers at 45% or below dropped to 15% in August. This figure is much lower than July’s 25% and June’s 44%.

The decreasing numbers here are a good thing. According to Fiore, it indicates a strengthening of manufacturing in the economy.

Other survey headline results diverged quite a bit from those of ISM. They showed manufacturing contraction occurring faster. Services narrowly avoided outright contraction with the weakest activity in seven months. Some of this divergence likely comes from the ISM including the public sector in its data.

Industrial Production Sees a Rise After 2 Months of Decreases

In July, total industrial production (IP) increased 1.0% (-0.2% year-over-year/YoY) following declines in the previous two months. The index for mining moved up +0.5%. Utilities also went up +5.4% as July temperatures vaulted the demand for cooling.

After downward revisions to the prior three months, manufacturing output rose 0.5% in July. This came thanks to a 5.2% jump in the production of motor vehicles and parts. Meanwhile, factory output elsewhere edged up 0.1%.

Altogether, the index for manufacturing in July was 0.6% below its year-earlier level. Meanwhile, the indexes for durable and nondurable manufacturing increased 0.8% and 0.1%, respectively.

New factory orders declined by 2.1%. If excluding the ever-volatile airplanes and automobiles, however, new orders rose by 0.8%. Less encouraging, business investment spending decelerated to +0.1% (+0.5% YoY).

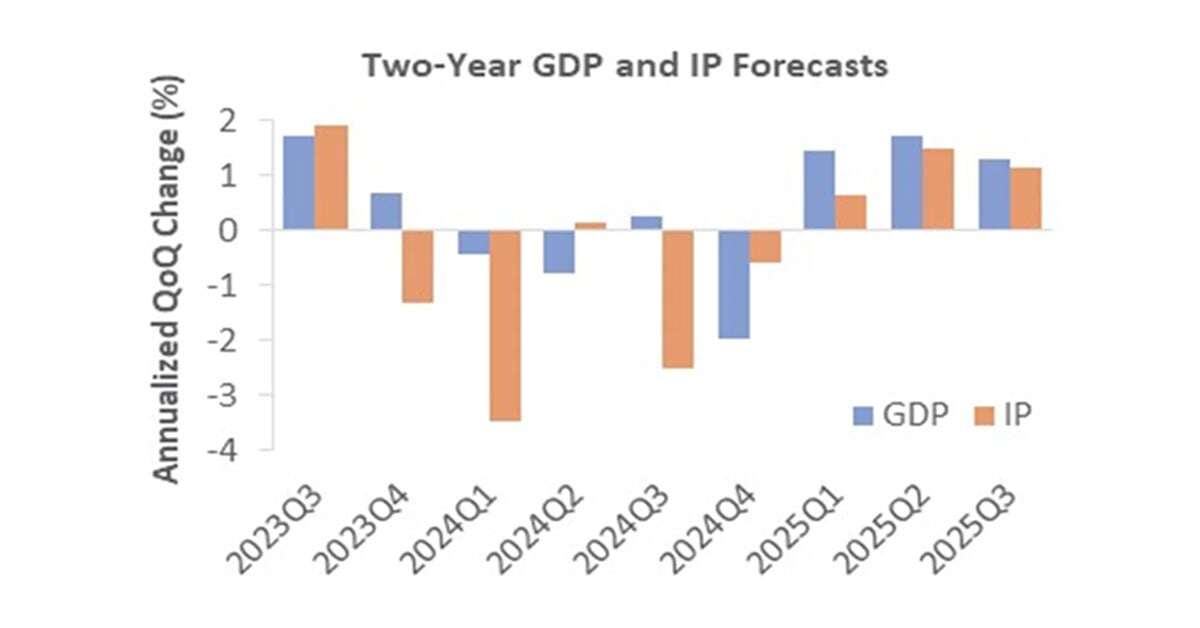

Our Predictions for Total IP

As the graph below shows, ResourceWise forecasts quarter-over-quarter (QoQ) changes in total IP to range between ‑3.5% and +1.9% annualized rates during the next 24 months. We predict the overall average at -0.3%.

Consumer and producer Price Indexes Remain Relatively Consistent Since June

The consumer price index (CPI) rose 0.2% in July (+3.2% YoY), the same increase as in June. The index for shelter was by far the largest contributor at over 90% to the monthly all-items increase at +0.4% MoM. The index for motor vehicle insurance also contributed significantly.

The food index accelerated to +0.2% in July from +0.1% in June. The energy index also rose 0.1% in July as the major energy component indexes were mixed.

Meanwhile, the producer price index (PPI) increased 0.3% MoM (+0.8% YoY) after being unchanged in June and declining 0.3% MoM in May. The July increase in final demand prices was led by a 0.5% rise in the index for final demand services. Much of this was attributed to a 7.6% rise in prices for portfolio management and related fees.

Prices for final demand goods edged up 0.1%, concentrated in meats at +5.0%.

Forest Products Price Indexes

In the forest products sector, the price indexes were measured as follows:

- Pulp, Paper & Allied Products: -0.3% (-0.4% YoY).

- Lumber & Wood Products: +0.3% (-8.9% YoY).

- Softwood Lumber: +4.4% (-17.3% YoY).

- Wood Fiber: -0.5% (-3.8% YoY).

FOMC Remains Focused Primarily on Addressing Inflation

There was no August meeting of the Federal Reserve’s Open Market Committee (FOMC). As a result, the federal funds rate (FFR) remained unchanged between 5.25 and 5.5%—a 22-year high.

No post-FOMC press conference meant the markets turned their attention to Fed Chair Jerome Powell’s remarks at the annual Jackson Hole, WY symposium. Powell’s speech seemed to appear less certain of the way forward than had been the case in the past.

On the one hand, he insisted that the Fed was still very much supporting a "restrictive" policy to help get inflation back down to 2%. On the other, Powell appealed to the uncertainty of the market as a big reason why they haven't reached that goal yet.

He concluded by saying the FOMC is proceeding with caution. Whether or not they add more restrictions or hold the rates as-is will depend on the next few weeks ahead.

Powell was careful never to explicitly mention any sort of rate cuts. Could these cuts be coming? And how might this affect our assessment that we’re in the starting stages of a recession?

Subscribe to ResourceWise Forest Products blog for news and commentary on economic factors impacting forestry, pulp & paper and other related industries.

What the UCO Market Reveals About Crude Tall Oil Demand

What's Next for Asia's Largest Wood Pellet Supplier?

Economic Conditions Remain Unchanged, How Does This Impact the Forest Products Industry?

With economic conditions showing little variation, the forest products industry finds itself at a crucial juncture due to global conflicts and...

The Verdict’s Out: We’re in the Starting Phase of a Recession

Ongoing debate continues among economists as to whether we’re actually seeing a “true” recession. Some analysts split hairs as to how we define a...

Economic Contraction Slows, but Remainder of 2023 Brings Uncertainty

Economic conditions have inched up in several key indicators. But global conflicts and persistent inflation position us on the brink of recessionary...