Ongoing debate continues among economists as to whether we’re actually seeing a “true” recession. Some analysts split hairs as to how we define a recession. Others take a broader look across all major areas of the economy to see some bright spots.

Looking at the facts, our perspective seems clear from this angle. We’re definitely seeing the major indicators of a recession starting up.

Related: 2023 Brings More Pulp and Paper Mill Closures – Do You Have the Right Data?

Related: Further Declines in Manufacturing Will Impact Forestry

What will this mean in the forestry industry beyond the struggles we’ve already reported on this blog such as mill closures and major drops in wood product demand?

Rolling Recession or Full-on Economic Downturn?

In light of the somewhat resilient GDP in Q1 2023, debate continues over whether a soft or hard economic “landing”—or any landing at all—might be in the offing.

Rather than an economy-wide recession, analyst Ed Yardeni argues “we really have been in a recession since early last year—it’s just been what I call a ‘rolling recession’ hitting different industries at different times.”

Moreover, Yardeni believes a full-blown downturn may be avoided by combining several factors:

- Fiscal stimulus (e.g., infrastructure spending and “onshoring” of manufacturing)

- Lagged effects of monetary stimulus (e.g., M2 money supply and pandemic-relief checks)

- Aging Baby Boomers spending down their $73 trillion of accumulated wealth

Yardeni’s thesis is an attractive one, but we cannot ignore the plethora of indicators that suggest otherwise:

- Increased corporate bankruptcies

- Surging “junk” loan defaults, and tightening of lending standards

- Spike in bank collapses and bank

These components have historically been associated with onset of recession and are presently “flashing red.” Despite arguments qualifying the type or conditions or definition of “recession,” these factors are hard to ignore.

Our perspective is that the U.S. economy is presently in phase 1 of the Incrementum Recession Phase Model.

Phase 1 presents like the smoke before a major fire. We're seeing an increased volatility in the financial markets. The market is now price correcting in anticipation of the full-on dip. This phase can last around 6 months, and we’re already well into the process.

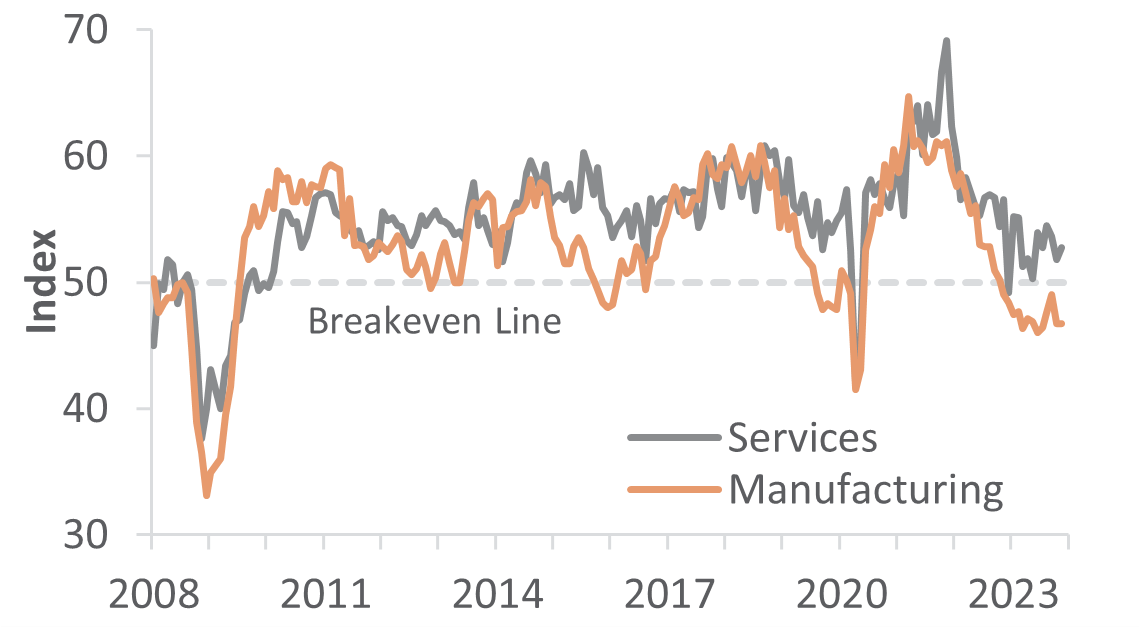

Manufacturer Surveys Show Clear Signs of Recession

The Institute for Supply Management’s (ISM) monthly sentiment survey of U.S. manufacturers for June indicates that sector is firmly in the grip of a recession. The PMI registered 46.0% (see table), down 0.9PP from May. 50% is the breakpoint between contraction and expansion.

All subindexes are below 50, with most falling further in June. Concurrent activity in the services sector expanded more rapidly (+3.6PP, to 53.9%), although half of the subindexes either are below 50 or decelerated relative to May.

With regard to services, numbers were considerably more optimistic. Services did not see a dip like manufacturing. GDP growth slowed in June, keeping things relatively solid.

Cost growth has led to some concerns within this sector, however. This comes as employers must increase wages to attract and retain a strong workforce. The cat-and-mouse between wages and costs may keep selling-price inflation elevated as we move more directly into phase 2 of the recession.

Consumer & Producer Price Indices Break Even While Forest Products See Drops

The consumer price index (CPI) rose 0.1% in May (+4.0.% YoY) after increasing 0.4% in April. Meanwhile, the producer price index (PPI) declined 0.3% in May (+1.1% YoY) following a 0.2% MoM rise in April and 0.4% drop in March.

The PPI’s MoM retreat was attributed to prices for final-demand goods, which fell 1.6% (led by gasoline at -13.8%). Conversely, services increased 0.2% (especially auto retailing at +4.2%).

Updates on Price Indices for Forest Products

In the forest products sector, numbers reflect much of the downturn we've seen in other economic areas. Recent data showed the following price indices in forest products:

- Pulp, Paper & Allied Products: The price index for pulp, paper and related allied products fell 0.1%, a +1.1% YoY increase.

- Lumber & Wood Products: Lumber and other wood products dipped -0.3%, marking a -15.9% YoY decrease.

- Softwood Lumber: Softwood lumber sales experienced a -0.3% drop to amplify the already alarming -40.4% YoY contraction.

- Wood Fiber: Finally, wood fiber dropped only -0.1%, just a -2.7% YoY decrease.

Credit Tightens Up, Keeps FFR Unchanged for Now

At the conclusion of its June 13-14 meeting, the Federal Reserve’s Open Market Committee (FOMC) left the federal funds rate (FFR) unchanged at a range between 5 and 5.25%.

“In light of how far we’ve come in tightening policy, the uncertain lags with which monetary policy affects the economy, and potential headwinds from credit tightening,” Fed Chair Jerome Powell said during a press conference. “We judged it prudent to hold the target range steady to allow the Committee to assess additional information and its implications for monetary policy.”

The FOMC’s concerns about headwinds from credit tightening appear to be warranted. A Fed study concluded the recent increase in interest rates could put an unprecedented number of distressed (defined as close to defaulting) companies out of business.

At the end of 2022, at which point the impacts of rising rates were in early stages, 37% of non-financial U.S. companies were in financial distress. The number reflects a higher share than during most previous tightening episodes since the 1970s.

According to Fed researchers, these interest and credit changes have created distress for many companies:

"Our results suggest that in the current environment characterized by a high share of firms in distress, a restrictive monetary policy stance may contribute to a marked slowdown in investment and employment [i.e., recession] in the near term. The effects in our analysis peak around one or two years after the [credit-tightening] shock, suggesting that these effects might be most noticeable in 2023 and 2024."

- FEDS Notes, June 23, 2023

Will We See More Interest Rate Hikes in 2023?

Despite the concerns brought up by this study, interest rates will still see more changes in the coming months. Chairman Powell stated that they expect the Fed to raise interest rates at least two more times in 2023. The FOMC’s willingness to keep raising rates can be interpreted as being driven by concerns over so-called "sticky" inflation.

Sticky inflation means ongoing hikes in both consumer wages and prices. Long-term, this can shift into persistent inflation with a host of additional economic concerns.

In deference to the idea the Fed is engaged in more than just a fight against inflation, we have applied 0.25PP increases to July, September, and December. We also think the Fed will then hold rates steady through mid-2024.

Our models call for QoQ changes in the CPI to fluctuate between +1.9% and +3.4% annualized rates, for an overall average of +2.7%. Concurrent changes to the PPI will range between -1.4% and +3.8, averaging +1.4% overall.

Get Key Economic Insights and Data Across the Forest Value Chain

ResourceWise provides subscribers with a robust set of tools and forecasting products tailored to those within forestry industry.

This post was a small excerpt from our monthly Economic Outlook report. The EO is a macroeconomic indicator forecast highlighting general economic trends and related data. It also includes expert insights and predictions about what to expect in several critical economic areas.

By understanding these economic indicators, you’ll get direct insight into elements such as potential future stumpage prices, buying and selling windows and more. Your business can develop more informed strategies on how to manage sales, negotiate purchases and better manage inventories in times of uncertainty.

Get in touch with our team to learn more about the EO and other forecasting tools to help your business do more.

What the UCO Market Reveals About Crude Tall Oil Demand

What's Next for Asia's Largest Wood Pellet Supplier?

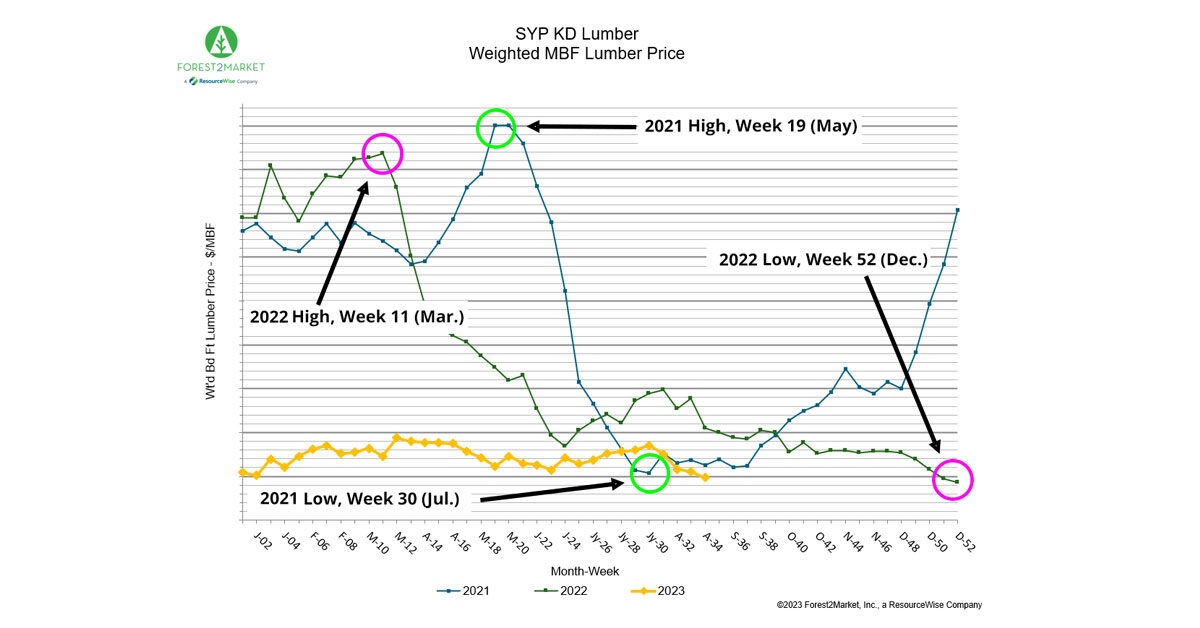

SYP Lumber Prices Fall to Lowest Level This Year

Reported SYP KD lumber prices have dropped to the lowest level so far this year. According to ResourceWise data, the price dipped just under...

Manufacturing and Industrial Production Show Very Slight Increases

Recession still looms over the economy. But a few small upticks in economic indicators show some life as we move into the 4th quarter of 2023.

Economic Conditions Remain Unchanged, How Does This Impact the Forest Products Industry?

With economic conditions showing little variation, the forest products industry finds itself at a crucial juncture due to global conflicts and...