Marko Summanen

Marko Summanen

UPM and Sappi have signed a non-binding letter of intent to form a graphic paper joint venture, combining UPM Communication Papers with Sappi’s European graphic paper business. The proposed entity would be owned 50/50 by UPM and Sappi and operate as an independent company responsible for its own operations and strategic decisions within agreed shareholder boundaries.

A major goal of this merger, as pointed out in the press release, is “securing long-term resilience and sustainability.”

But what could this mean for the European paper market?

Why This Joint Venture Matters

Historically, UPM and Sappi competed heavily, particularly in coated grades. Pricing considerations was often secondary to maintaining volume, and spot market competition occasionally pushed prices downward.

In this context, the proposed joint venture represents a significant structural shift.

This JV could be a much-needed development to secure the European paper industry's competitiveness, especially given the industry's scattered ownership structure. Without consolidation, the European paper industry risks slowly shrinking itself through fragmentation and chronic overcapacity.

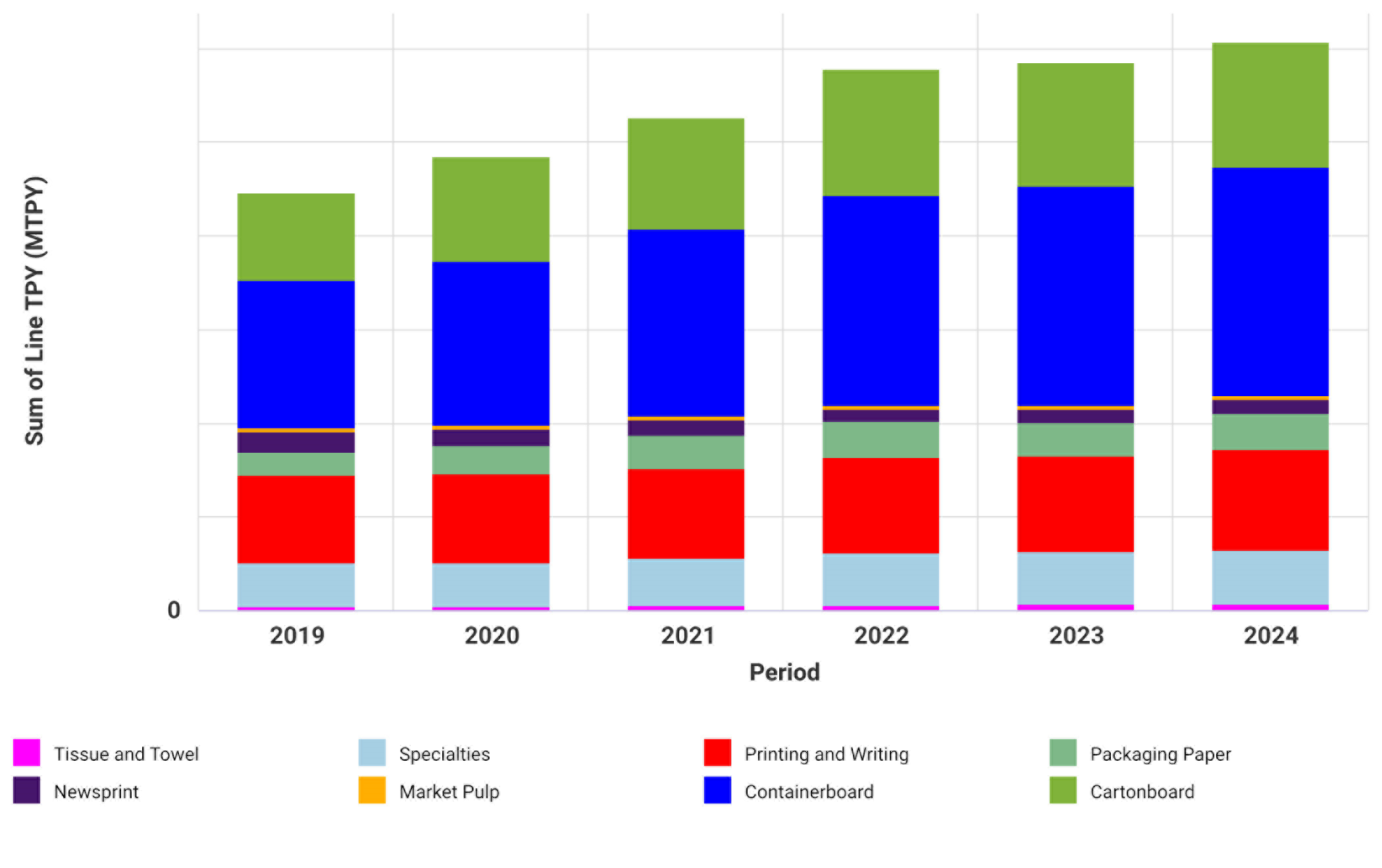

The chart below illustrates the relative scale of European graphic paper capacity by company and grade, highlighting the size of the potential UPM–Sappi joint venture within the broader competitive landscape.

Projected European Graphic Paper Capacity After Joint Venture

Source: FisherSolve

Structural Challenges This Upcoming JV Must Address

This joint venture will enter a market facing significant structural pressures:

- Demand decline: Graphic paper demand in Europe is falling 6-10% annually, depending on grade.

- Persistent overcapacity: Particularly in coated mechanical and coated woodfree segments.

- Rising energy and carbon costs: ETS 1 and the upcoming ETS 2 significantly impact energy-intensive mills.

- Increasing imports: Especially coated woodfree from Asia and South America.

- Customer resistance: Large publishers and printers benefit from competition and may increase imports to maintain leverage.

In short, the JV must operate in a structurally declining market while managing rising costs and increasing global competition.

What Must Be the JV’s True Agenda?

To become stronger than its individual parts, the JV must deliver on five critical priorities:

Commercial Synergies: Immediate Opportunities

A unified commercial organization could create immediate opportunities and improvements:

- Reduced internal competition: Historically, the two companies occasionally competed directly. The JV structure eliminates this internal pressure.

- Improved fiber sourcing: Fiber represents the largest cost contributor. Harmonized sourcing strategies could create meaningful savings.

- Contract stability: Unified contract structures could reduce exposure to volatile spot markets and improve contract stability.

- Better positioned to compete with imports: A larger entity with a coordinated strategy may better counter low-priced imports.

Asset Rationalization: The Real Battlefield

When any joint venture occurs, the most important decisions involve which assets remain competitive and which do not.

Portfolios should prioritize machines that offer:

- Large scale

- High energy efficiency

- Low capex requirements

- Low carbon footprint

- Strong customer positioning

At the same time, companies may consider exiting assets that are:

- Smaller and older coated machines

- High fixed-cost mills

- Sites requiring major energy reinvestment

- Overlapping capacity in declining grades

Understanding Asset Competitiveness

Benchmarking tools, such as FisherSolve’s M&A scenario analysis, allow industry professionals to simulate the effects of company mergers.

By merging assets virtually, users can analyze:

- Production capacity

- Asset performance

- Benchmark rankings

- Potential restructuring scenarios

The Market Dynamics of Capacity Closures

In soft market conditions, reducing capacity can allow market prices to temporarily decline further.

This happens because when prices approach the cost floor, the highest-cost producers begin exiting the market, effectively lowering the floor price.

This situation can be overwhelming for high-cost mills that cannot boost their competitiveness through investments, leading to additional closures across the competitive asset base.

Some mills already face difficulties because they lack viable energy solutions—either low-carbon fuels are unavailable or the necessary investments cannot be justified. Specifically, weak sites with no biomass access, district heating, or feasible electrification are increasingly at existential risk.

Carbon Is the New Competitive Dimension

Today, the industry faces an additional challenge in becoming truly competitive: decarbonization. Carbon emissions are increasingly becoming a second dimension of the cost curve.

Regardless of input costs, maintaining a low CO2 footprint is essential to remain competitive within the peer group. This challenge becomes even more severe when the energy transition cannot be solved economically.

A difference of nearly one ton of CO2 per ton of paper can translate into approximately €100 per ton in additional cost. This difference is significant in an industry where EBITA margins are often below 10%.

Synergies in Reducing Costs

The new JV will evaluate its assets as a single portfolio, which fundamentally changes the perspective.

Fiber sourcing is a major cost driver, and because the partners come from very different starting points, this shift will influence which mills appear more or less attractive than before. As costs and synergies are reassessed from a unified viewpoint, some mills may lose competitiveness while others gain it.

A key strategic question will be how vertical integration influences asset competitiveness.

UPM brings substantial fiber security to the equation:

- Over 500,000 hectares of forest in Finland

- Extensive plantations in Uruguay exceeding 500,000 hectares

This provides strong fiber security and cost stability.

Whether the JV can leverage this advantage across the combined asset base may become one of the most important strategic questions moving forward.

This ultimately determines:

- The JV’s cost curve

- Which mills survive

- Where synergies come from

- How much restructuring is needed

Could Some Graphic Paper Machines Transition to Packaging?

Another strategic question concerns the potential future role of certain graphic paper machines.

Both UPM and Sappi have established positions in flexible packaging and specialty paper markets, and some of the machines currently producing graphic grades already have the technical capability to produce barrier or flexible packaging papers.

At the same time, regulatory pressure to reduce plastic packaging and increase the use of fiber-based alternatives could create new demand for these grades.

This raises an important strategic question for the joint venture:

Could regulatory and market developments enable some graphic machines to transition into long-term sustainable packaging assets?

However, such a shift would also introduce strategic complexity. Expanding packaging production within the joint venture could potentially overlap with UPM Specialty Papers and Sappi’s existing packaging businesses.

The challenge, therefore, becomes balancing new growth opportunities with portfolio alignment across the parent companies.

How Could Competitors Respond?

The joint venture’s greatest structural advantage may come from the ability to evaluate its mills as a single combined asset portfolio. This allows the new entity to improve competitiveness primarily through portfolio optimization, rather than through significant new capital investment. By closing weaker or overlapping assets, the JV could improve its cost position relatively quickly.

Competitors may face more difficult choices. Without the same scale advantages, they may need to:

- Invest to upgrade assets

- Exit certain grades

- Or pursue their own consolidation strategies

In some segments, particularly coated grades, consolidation opportunities may already be limited. However, the move could potentially trigger additional strategic discussions among producers in adjacent grades, including uncoated woodfree.

What Will Ultimately Determine Success

This UPM and Sappi joint venture will not be judged on the short- or even medium-term growth. It will be judged on:

- How many machines it closes

- At what pace closures occur

- Whether it will be better positioned to compete with imports

If executed decisively, this JV could define the European graphic paper market. If execution is slow, it risks becoming simply a larger version of today’s structural problem.

Determining how much capacity must exit the market to restore structural balance will be one of the most critical decisions the new JV will face.

Together with our partner STE Analytics, ResourceWise has developed advanced system-dynamic models that are back-tested against historical data to replicate how the market behaves under different conditions. These models allow us to understand not only how the market is likely to react, but also the consequences that each strategic decision may trigger once implemented.

The example simulation below illustrates alternative capacity-adjustment scenarios and the impact of timing those adjustments.

This type of modeling provides a foundation for well-justified, data-driven strategic decisions.

ResourceWise-STE Market Model Scenario for Capacity vs Price

Data-Driven Decisions Will Shape the Industry’s Future

As the European graphic paper market continues to evolve, strategic decisions around capacity, energy transition, and asset competitiveness will only become more complex. At ResourceWise, our platforms help industry leaders simulate consolidation scenarios, evaluate mill competitiveness, and understand the potential impact of strategic decisions before they are implemented. In a market defined by structural decline and rising cost pressures, data-driven insight is becoming the most important competitive advantage.

To learn more, check out our solutions page.

The Pulp Mill as a Biorefinery: Unlocking New Revenue Streams

Bio-Bunker Premiums Rebound as Oil Market Disruption Eases

India's Pulp and Paper Industry: Opportunities and Challenges

India's pulp and paper market is currently experiencing a significant transformation fueled by a mix of economic, demographic, and technological...

Three Major Moves Reshaping Pulp and Paper Right Now

The pulp and paper industry has seen several notable announcements in April 2026. Taken together, they point to a few important themes: continued...

Pulp and Paper News: Top Industry Headlines of the Week

In partnership with MarketIntel News, FisherSolve™ provides one of the most extensive paper industry news services. Subscribers receive daily emails...