For more than a decade, Australia has been a significant supplier of hardwood and softwood chips to North Asia’s pulp and paper producers. Strong plantation resources, established trade routes, and deep relationships with China and Japan supported consistent export flows. But now the data is telling a different story – one of slowing demand, shifting trade patterns, and rising competitiveness.

From Peak to Pullback: The Decline in Export Volumes

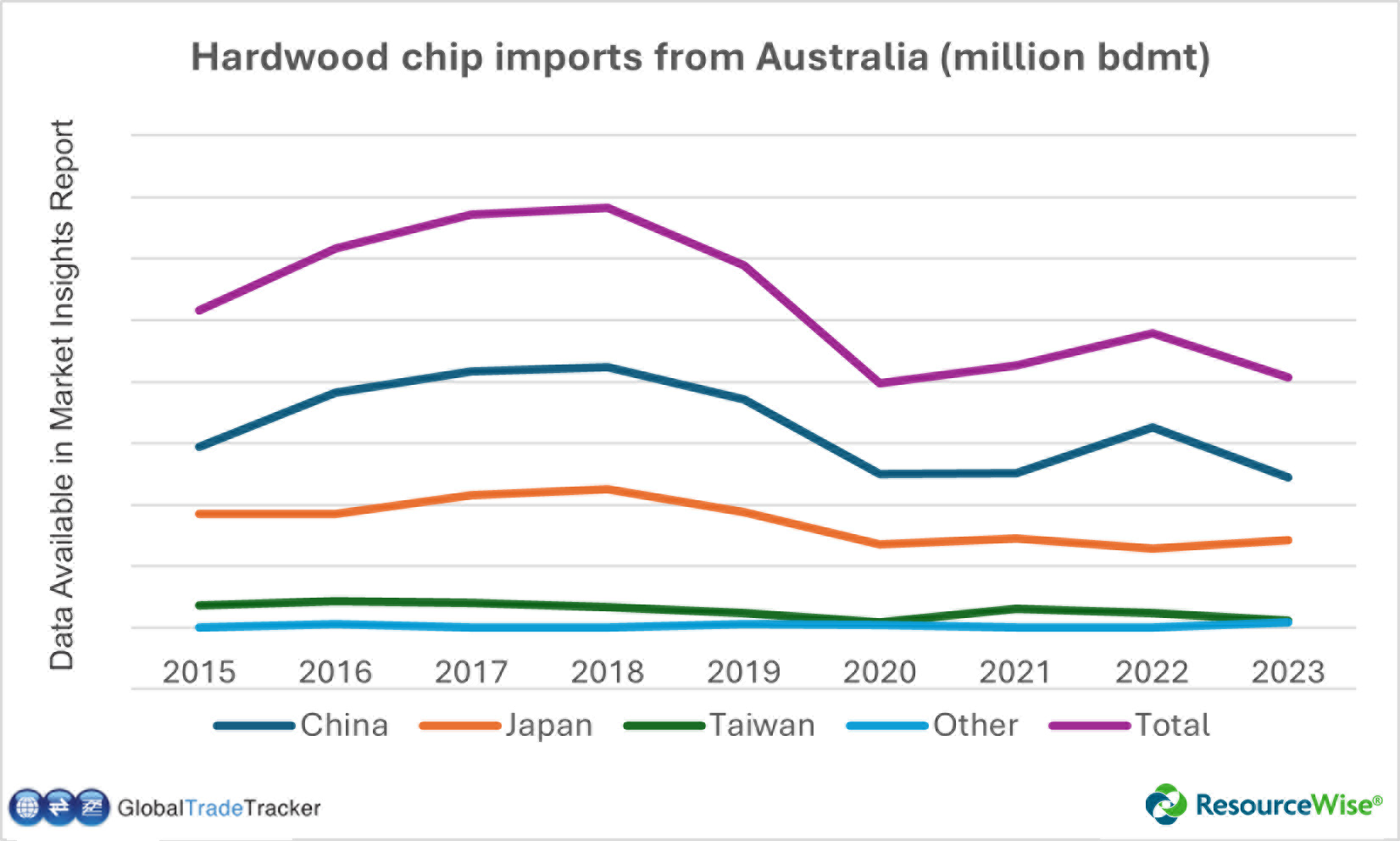

Australia’s hardwood chip exports hit a peak of 6.8 million bdmt in 2018. Since then, exports have dropped significantly. By 2025, total hardwood chip volumes fell by 45% from the 2018 peak, and shipments to China decreased by 33%. Japan’s imports from Australia dropped even more dramatically – down 65% between 2018 and 2025.

However, these are not circular dips; instead, they indicate deeper structural shifts in the region’s pulp and paper industry, which are transforming fiber demand patterns throughout the Pacific Rim.

China’s Overcapacity Is Reshaping Fiber Trade

China has long been the anchor market for Australian hardwood chips. However, rapid and ongoing expansion in China’s pulp and paper industry has created overcapacity and structural imbalance. As mills ramped up production, fiber procurement strategies evolved.

At the same time, China has increased the availability of domestic wood fiber — including woodchips — reducing dependence on imports. The result is a measurable shift in trade flows. Demand for imported hardwood chips from Australia has softened, and pricing has come under pressure.

In the second half of 2025, the average export price for Australian hardwood chips was 5% lower year-over-year, with prices to China down 3% compared to the prior year. For exporters already grappling with declining volumes, pricing weakness compounds the challenge.

A Market in Transition

The factors influencing the market—such as overcapacity in China, increased domestic fiber supplies, price competition, rising demand in Southeast Asia, and heightened regional rivalry—indicate more than just short-term fluctuations. They suggest a fundamental shift in the structure of Asia’s wood fiber trade.

For producers, exporters, traders, and investors, understanding these shifts is critical. Where will sustainable demand growth come from? How durable is China’s structural surplus? Can emerging markets offset North Asian declines? And what do pricing trends signal for 2026 and beyond?

To dive deeper into the data, trade flows, pricing movements, and competitive outlook, download our full Market Insights report, “Australia’s Wood Chip Exports at a Crossroads: Trade Shifts in the Asia-Pacific Fiber Market.”

.png)

Cross-Border Trade in Resource Industries: Structuring for Risk and Compliance

Explainer: Getting to Know the USDA's Feedstock CI Calculator

Navigating the Shifting Currents of Australia's Hardwood Chip Sector

Known for its rich biodiversity and vast natural landscapes, Australia is a globally significant exporter of hardwood chips, which represent around...

Global Wood Markets Shift as China Lifts Timber Ban on Australia

Global wood markets will see another changeup in the coming months. Australian exporters can again ship logs to China following a 2.5-year ban. But...

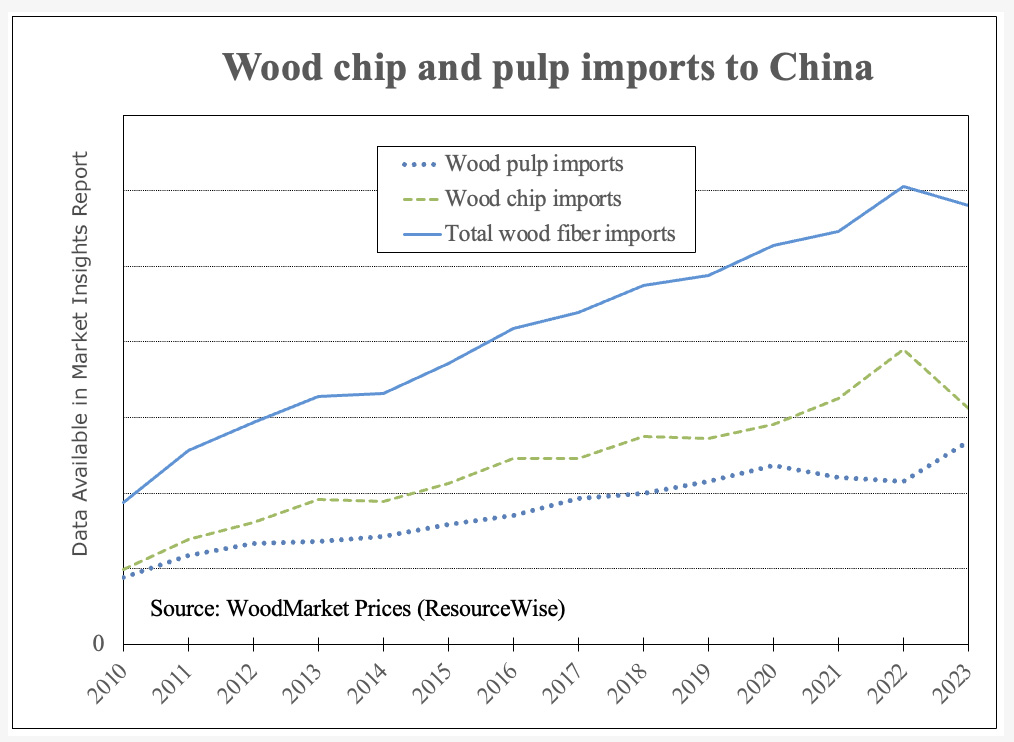

A Look at China's Fiber Import Trends

China's paper industry heavily depends on a combination of local and imported pulp and wood chips to fulfill its fiber requirements. The balance...