Daniel Stuber

Daniel Stuber

Similar to concerns being voiced today regarding the emergence of the wood pellet export industry, the rapid proliferation of chip mills in the US South between 1985 and 2000 generated considerable controversy. Much like today, environmentally minded non-governmental organizations (NGOs) were concerned about impacts to forest resources and habitat while competing users of feedstock were concerned about 1) erosion of margin due to price increases and 2) that feedstock was being diverted to export markets.

As federal policies (most notably the Endangered Species Act) began restricting harvests on federal land in the Northwest, the resulting supply constraints forced the closure of more than 200 Northwest sawmills closed between 1989 and 2004[1]. At the same time, forested acres in the US South were increasing, the result of regeneration and afforestation on abandoned agricultural land. Forests in the South—more than 80 percent of them privately owned—offered an abundant, fast growing supply. The convergence of these two factors led to the migration of the forest products industry from the Pacific Northwest to the South beginning in the 1990s.

As more production capacity flowed to the South, the needs of pulp and panel manufacturers to optimize their supply chains led many of them to replace their pulpwood yards and on-site chipping facilities with fiber from remote chip mills. In this new model, pulpwood is chipped at a standalone, satellite facility and then shipped to the manufacturing facility as needed for a much lower cost.

Concurrently, Japanese hardwood pulp producers were ramping up production. With limited domestic resources, these producers began targeting and securing wood fiber from southern export chip mills. Prior to 1985, 32 chip mills existed in the South; as a result of incremental demand from both the migration of Pacific Northwest production to the South and exports to Japan, by 2000, that number had increased to more than 150[2].

This rapid proliferation of the chip mill model generated considerable controversy. Organizations like the Dogwood Alliance emerged in the environmental movement fighting chip mills. The arguments of these organizations included:

“Chip mills have encouraged massive, industrial-scale clearcutting across the South.”[3]

“Since the mid-1980’s, at least 100 chip mills have sprung up like measles across the landscape of the South, causing unprecedented forest destruction.”4

“Although only a small percentage of the wood chips produced in the South are exported, exports are unnecessarily increasing the burden on our forest resources and have a negative impact on jobs. Sawmills have already had to close down because of the increase in prices driven by the export markets.”[4]

These arguments proved to be hyperbolic and even false in the end. Chip mills were not a source of forest destruction, a reduction in harvest timing did not occur, and they did not put undue burden on forest resources in the South. A study commissioned by the State of North Carolina in 2000, for instance, concluded that while they did find that wood chip mills increased the forest areas harvested in the state, the actual impacts were much “lower than commonly presumed or publicized in popular literature opposing wood chip mills. Even with increased harvests experienced in the 1990s, the state as a whole would generally have sustainable inventory and removal levels in the foreseeable future based on simple growth to removal ratio analyses for the addition of wood chip mills alone.” [5]

And by looking at historical data now, the dire consequences predicted did not materialize.

The main focus of the attacks on chip mills, which used 88% hardwoods and 12% softwoods6, was that they were clearcutting hardwood forests and replacing them with pine plantations. Today, hardwood comprises 59% of the timber inventory in the South, and more than 148 million acres are natural hardwoods. In addition, natural hardwoods in the South have a growth to removals ratio of 2.45, which means that for every ton of natural hardwood that is harvested each year, the forest is growing an additional 2.45 tons of volume.

Today, roughly 70 chip mills remain in the South. The real market drivers behind the drop in the number of mills include:

-

Japanese demand for hardwood chips peaked in 1998 and then dropped precipitously when Japan started sourcing wood from the southern hemisphere.

-

Hardwood pulpwood demand decreased in the South as demand for paper fell in the wake of technological advancements.

-

With the advent of the sawhead shear in 1994, logging production increased and it became unnecessary to manage satellite operations to provide surge capacity for mills.

-

Mill consolidation meant fewer pulp mill companies could fully utilize chip mills (for example, instead of two competing chip mills running at 50% capacity, one—operated by the consolidated company—could run at 100%)

-

The chip mills built in the 1980s and 1990s had a chipping capacity of 200-300,000 tons per year. New ones operate at 750,000 to 1,000,000 tons annually.

Arguments similar to those leveled at chip mills are now being floated about the effects of the industrial wood pellet industry on southern forest resources. Our view is the result will be much the same: we’ll find that anti-pellet claims will be, in Shakespeare’s words, “full of sound and fury, signifying nothing” in the end.

Read the full report, Wood Supply Market Trends in the US South: 1995 – 2015.

[1] Welch, C. (2004, 04 11). Old-growth logging nearing a standstill in dramatic shift. Seattle Times. Retrieved from http://community.seattletimes.nwsource.com/archive/?date=20040411&slug=forestplan11m

[2] Jehl, D. (2000, August 8). Loggin's Shift South Brings Concern on Oversight. New York Times.

[3] Smith, D. (1998, Winter). The Infestation of Chip Mills in the Southern U.S. Synthesis/Regeneration, pp. 15-17. Retrieved from www.greens.org/s-r/15/15-17.html

[4] Manuel, J. (1999, August). Do Wood Chip Mills Threaten the Sustainability of North Carolina Forests? North Carolina Insight, pp. 66-91.

[5] Dodrill, J. D., Cubbage, F. W., Schaberg, R. H., & Abt, R. C. (2002, Nov-Dec). Wood chip mill harvest volume and area impacts in North Carolina. Forest Products Journal. Retrieved from www.freepatentsonline.com/article/Forest-Products-Journal/96121846.html

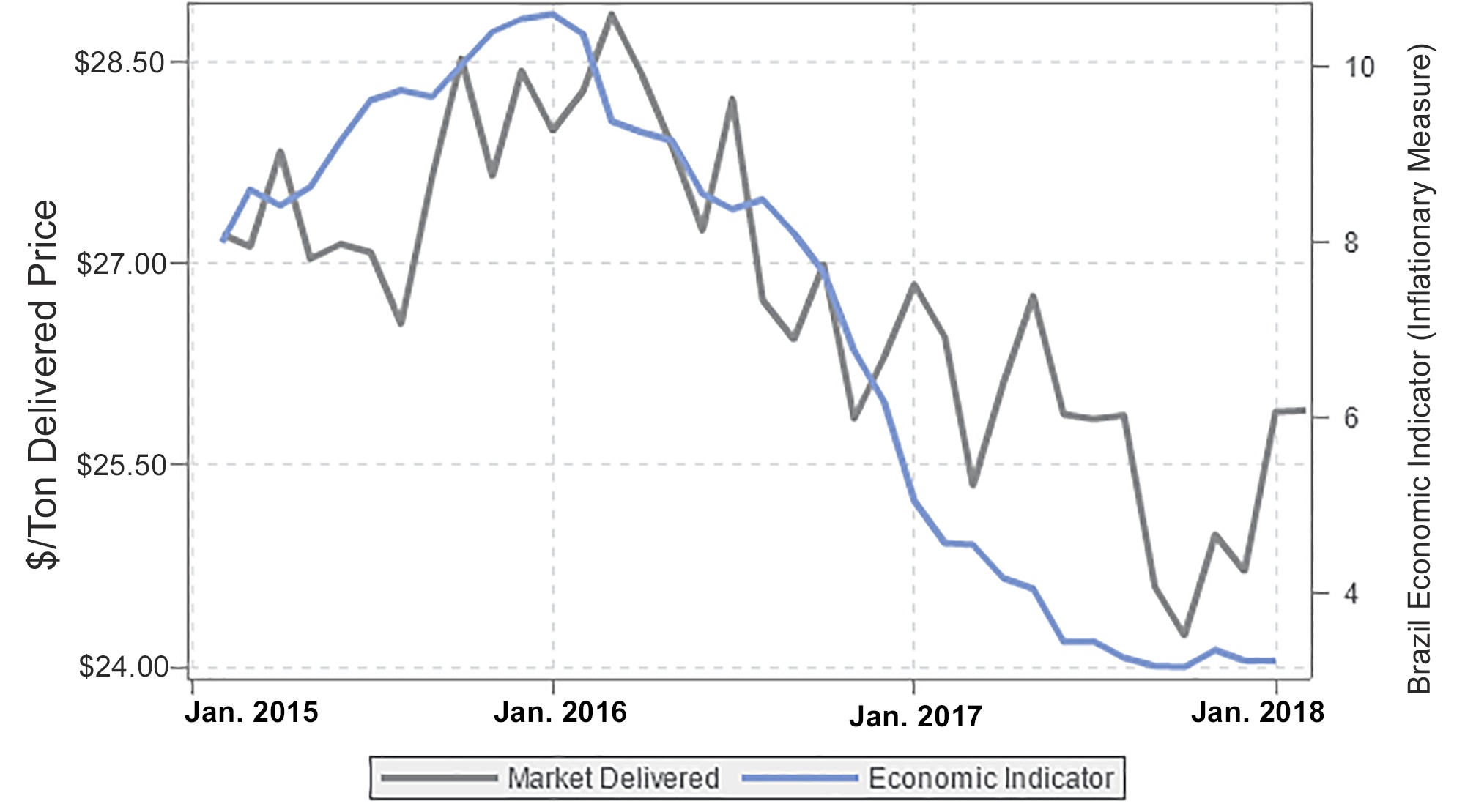

The Conversion of Planted Forests in Paraná, Brazil and its Effects on the Market

The conversion of planted forests to agricultural land in Brazil’s southern region of Paraná is not a recent phenomenon. Over the last several years,...

TISSUE: Panic Buying Not Just a Local Phenomenon

Panic buying, hoarding or establishing a “personal inventory,” however you want to describe it, the buying of tissue – especially toilet paper – has...

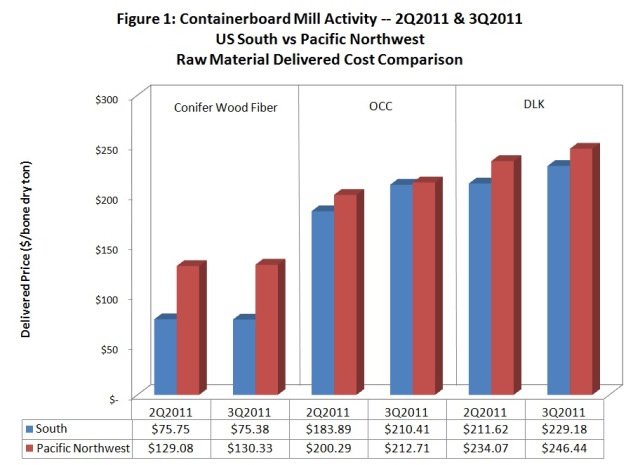

3Q2011 Containerboard Mill Activity – US South and Pacific Northwest

Containerboard mills in the US South and Pacific Northwest experienced increased raw material costs in 3Q2011. Figure 1 compares 3Q and 2Q prices for...