Bruce Janda

Bruce Janda

1 min read

Under Energy-Price Pressure Germany’s Slow-Growth Stage Sees Its Decarbonization Rate Accelerate

When we last focused on Germany's tissue market more than two years ago, the world was dealing with the severe disruptions of the Covid-19 pandemic....

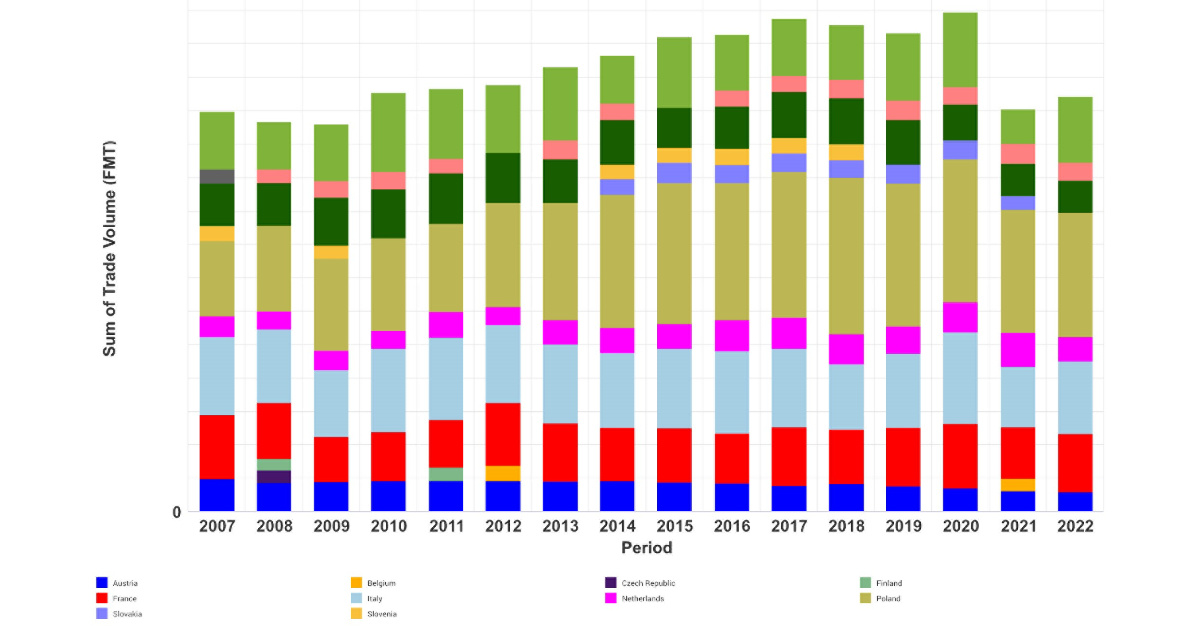

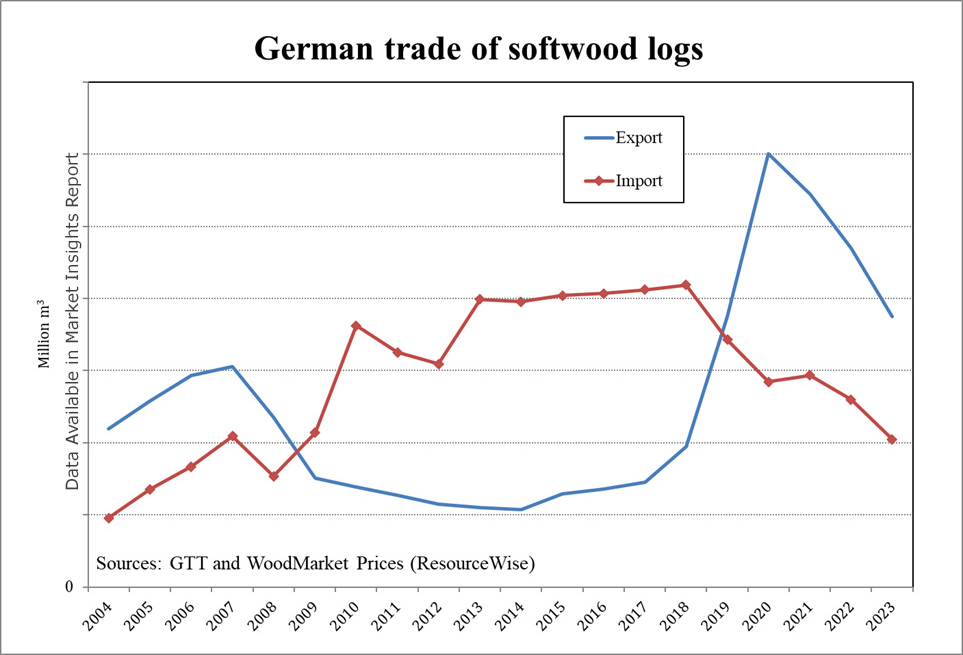

Germany's Softwood Log Market: Trends and Challenges

Understanding the complexities of the international market for softwood logs can be a daunting task. However, it’s crucial for anyone involved in the...

Germany’s Softwood Log Market Tightens as Prices Rise and Trade Shifts

Germany remains one of Europe’s most influential forest products markets. As the backbone of domestic sawmilling and a key driver of regional trade...