Håkan Ekström

Håkan Ekström

Global trade of hardwood chips rose in early 2022, driven by increased fiber demand by Chinese pulpmills.

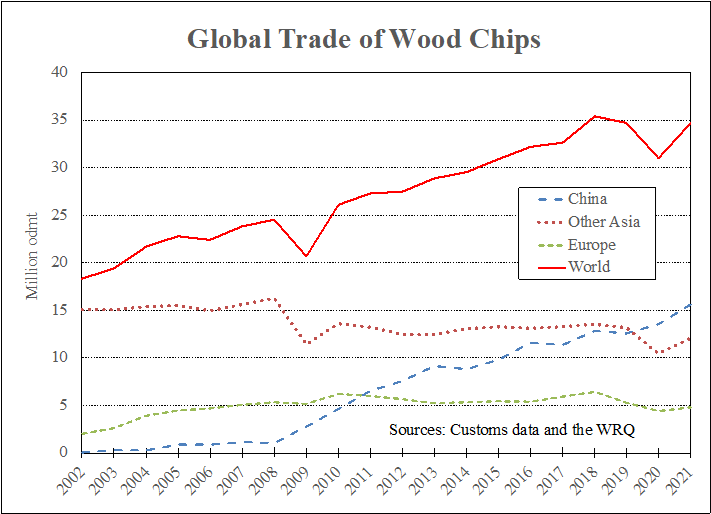

In 2021, the world’s shipments of wood chips reached almost 35 million m3, close to the highest on record.

Significant expansion of pulp capacity in China combined with a lack of domestic wood fiber has driven the global increase in traded wood chips over the past decade (see chart).

About four-fifths of the trade was hardwood chips in 2021, predominantly destined for pulpmills in Asia. The remaining volume was softwood chips.

According to Wood Resource Quarterly, importation to China reached a new record-high of 14.8 million odmt in 2021, a 12 % increase from the previous year. This rise was a continuation of an unprecedented upward trend that started in 2008 when China imported only one million odmt.

During the first four months of 2022, China’s wood fiber demand continued to rise and was 10% higher than during the same period in 2021. This accounted for 56% of the world’s hardwood chip imports.

Wood Chip Trade Beyond China

Outside of China, the trade of wood chips has been relatively stable over the past ten years, ranging between 19-21 million tons annually. The only exception was for 2020 when total shipments fell to just over 17 million tons. This decline is attributable to the short-term supply chain disruptions due to COVID-19 rather than a change in forest production trends.

In early 2022, total imports to Asia (excluding China) and Europe were practically unchanged from 2021. When the investments in large-scale pulp mills in China began to take place in 2008, the preferred wood fiber was predominantly lower-cost and lower-quality Acacia wood chips from Vietnam, Thailand, and Indonesia.

Continuing Evolution of Chinese Pulpmill Markets

This started to change in 2013-2014 when pulpmills saw the cost and quality benefits of using higher density wood chips such as Eucalyptus Nitens and Eucalyptus Globulus from Australia and Chile. As a result, from 2012 to 2017, the high-yield fiber share of total imports dramatically increased from 11% to 47% of the total import volume.

However, in 2018, this five-year rise in market share leveled off and fell during 2019-2022 to only 30% in 1Q/22. With the supply of hardwood fiber becoming tighter around the Pacific Rim, the fiber sourcing by Chinese pulpmills will likely continue to evolve, including the possibility of new regions coming into play.

This is a preview post of our Market Insights report from Wood Resources International (WRI). For the past 13 years, Wood Resources International has distributed Market Insights on a regular basis to over 8,000 forest industry executives, analysts, investors, consultants and journalists worldwide. These Market Insights have covered the most recent developments in regard to global wood supply, forest industry production, forest products trade, and pricing of sawlogs, pulpwood, wood chips, lumber and biomass.

The Industries of Chemicals: How Key Markets Shape Global Demand

How China’s Pulp Overcapacity Is Impacting the Australian Wood Chips Market

For more than a decade, Australia has been a significant supplier of hardwood and softwood chips to North Asia’s pulp and paper producers. Strong...

Global Pulplog and Wood Chip Prices Up 10% Since 2021

Tight wood fiber supply and record high pulp prices have pushed the worldwide costs for pulplogs and wood chips upward 10% the past year. Wood fiber...

Finland’s Forest Industry Repositions for Growth

Finland’s forest products industry stands at a pivotal moment. Global market shifts, tightening EU regulations, and domestic restructuring are...