Håkan Ekström

Håkan Ekström

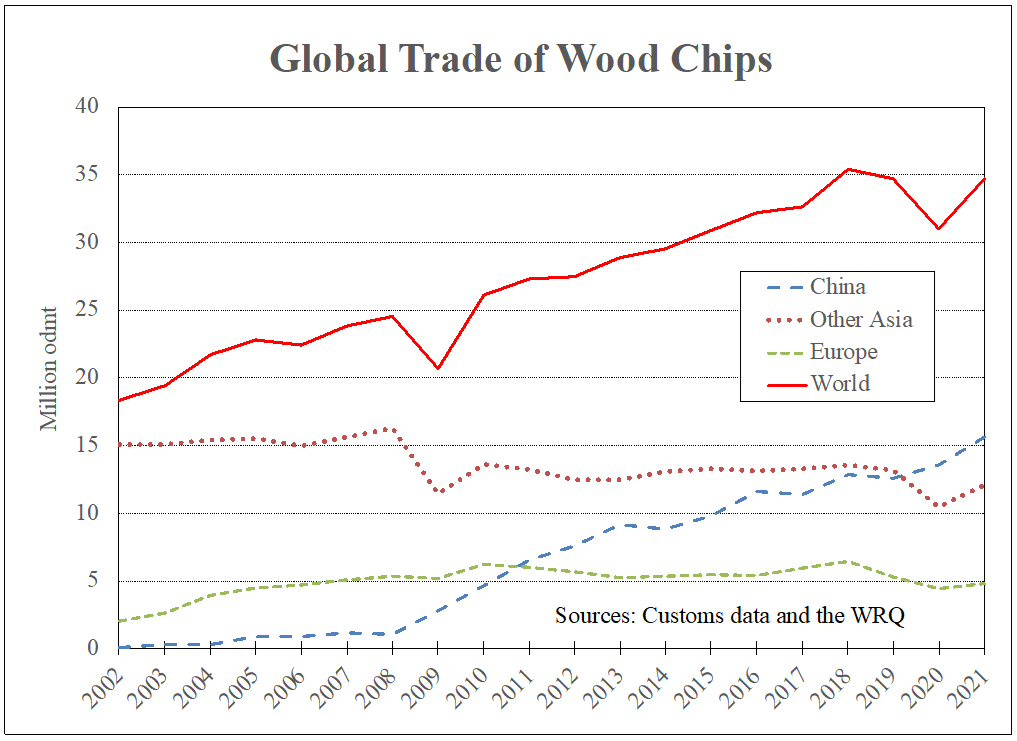

In 2021, the world’s shipments of wood chips reached almost 35 million m3, close to the highest on record. Significant expansion of pulp capacity in China combined with a lack of domestic wood fiber has driven the global increase in traded wood chips over the past decade (see chart). About four-fifths of the trade was hardwood chips in 2021, predominantly destined for pulpmills in Asia, while the remaining volume was softwood chips.

According to the Wood Resource Quarterly, importation to China reached a new record-high of 14.8 million odmt in 2021, a 12 % increase from the previous year. This rise was a continuation of an unprecedented upward trend that started in 2008 when China imported only one million odmt. During the first four months of 2022, China’s wood fiber demand continued to rise and was 10% higher than during the same period in 2021, accounting for 56% of the world’s hardwood chip imports.

Outside of China, the trade of wood chips has been relatively stable over the past ten years, ranging between 19-21 million tons annually, except for 2020, when total shipments fell to just over 17 million tons. This decline is attributable to the short-term supply chain disruptions due to COVID-19 rather than a change in forest production trends. In early 2022, total imports to Asia (excluding China) and Europe were practically unchanged from 2021.

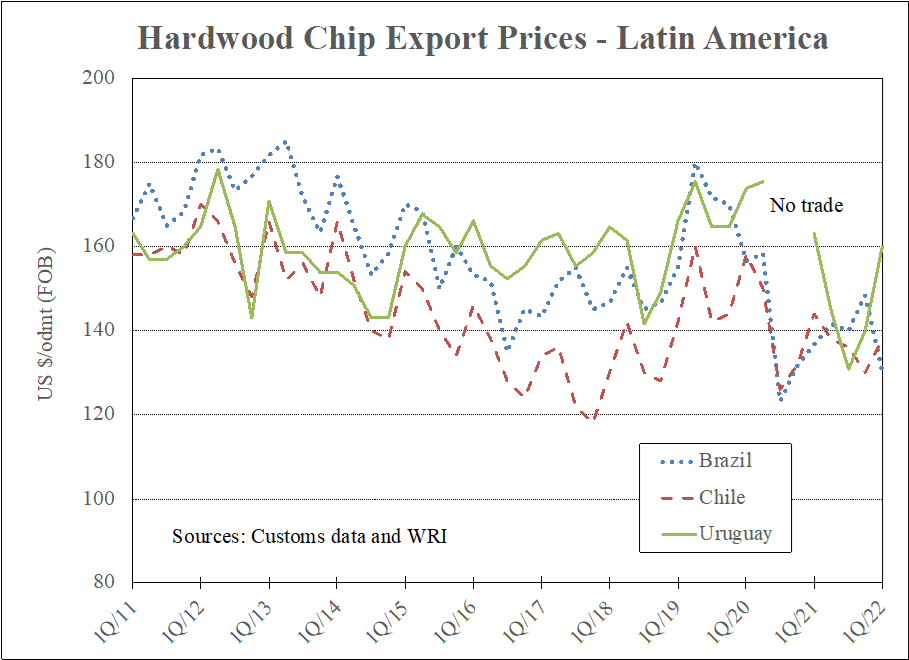

When the investments in large-scale pulp mills in China began to take place in 2008, the preferred wood fiber was predominantly lower-cost and lower-quality Acacia wood chips from Vietnam, Thailand, and Indonesia. This started to change in 2013-2014 when pulpmills saw the cost and quality benefits of using higher density wood chips such as Eucalyptus Nitens and Eucalyptus Globulus from Australia and Chile. As a result, from 2012 to 2017, the high-yield fiber share of total imports dramatically increased from 11% to 47% of the total import volume.

However, in 2018, this five-year rise in market share leveled off and fell during 2019-2022 to only 30% in the 1Q/22. With the supply of hardwood fiber becoming tighter around the Pacific Rim, the fiber sourcing by Chinese pulpmills will likely continue to evolve, including the possibility of new regions coming into play.

Are you interested in worldwide wood products market information? The Wood Resource Quarterly (WRQ) is a 70-page report established in 1988 and has subscribers in over 30 countries. The publication tracks prices for sawlog, pulpwood, lumber & pellets and reports on trade and wood market developments in most key regions worldwide. For more insights on the latest international forest product market trends, please go to www.WoodPrices.com

What the UCO Market Reveals About Crude Tall Oil Demand

What's Next for Asia's Largest Wood Pellet Supplier?

Pacific Rim Wood Chip Market Shows Drops in Both Soft and Hardwood

Softwood chips play a major role in global wood markets, but hardwood chips far surpass softwood in terms of volume. The majority of global wood chip...

Trends in China's Pulp, Paper, and Forestry Industry

A Brief Snapshot of the Global Paper Industry The global pulp and paper industry continues to thrive, with a strong focus on the packaging sector...

Wood Chip Exports From Brazil and Uruguay Hit Record Levels

Eucalyptus plantations in Latin America are a significant supply source to pulpmills in China and Japan. However, the Latin American share of total...