5 min read

The forest products market remains a vital component of the global economy, driving growth through a diverse range of sectors including timber, paper, and bioenergy. Understanding the current economic landscape is crucial for stakeholders to navigate market trends that shape supply and demand dynamics.

Economic Overview and Market Trends

The US economy has shown resilience, rebounding steadily from the impacts of COVID-19. After a significant dip in 2020, GDP growth rates have stabilized, with a promising 3% expected for the second half of 2024.

Despite this rebound, the forest economy has experienced fluctuating price trends. The instability is particularly evident in the softwood lumber and wood pulp sectors.

Some areas have seen price declines which have persisted for several months. Others, such as engineered wood products, are witnessing a growth in demand.

Following an extended period of rising stock prices, the US homebuilding sector encountered a slowdown in housing starts during the second quarter of 2024. This deceleration has reduced lumber demand and subsequent capacity adjustments in mills.

Housing affordability, supply availability, and the direction of FED rate action have remained challenges throughout the year. However, demand for innovative wood products like cross-laminated timber (CLT) and glulam beams is anticipated to rise, driven by their applications in sustainable construction.

What Can We Learn from the Past Five Years?

Over the past five years, valuable insights have emerged to guide the forestry industry's progress:

1. Prioritize Efficiency and Cost Reduction

The focus on prioritizing efficiency and cost reduction has led mills to embrace advanced technologies like AI-driven machinery, robotics, and optimized cutting systems.

These technological advancements have significantly enhanced operational efficiency by reducing waste and boosting productivity. Precision manufacturing in particular has enabled sawmills to extract maximum yield from each log, producing more lumber with minimal waste. This approach not only amplifies profitability but also endorses sustainability.

Additionally, mills are exploring innovative uses for wood byproducts in bioenergy and other bio-based products, thereby fostering a circular economy and minimizing waste. These measures collectively ensure that the mills remain competitive and forward-thinking in an ever-evolving market.

2. Invest in Expanding and Transforming Product Lines

Sawmills have strategically expanded their product lines to include engineered wood products, addressing the growing demand for mass timber construction. This diversification has unlocked new revenue streams and bolstered the industry's market position amid fluctuating demands in traditional sectors.

The surge in e-commerce and global shipping has led to an increased need for packaging materials, especially corrugated cardboard. This product has helped counterbalance declines in traditional paper products.

Many mills have pivoted to focus on converting operations from conventional paper production to packaging materials, seizing the opportunity to meet the heightened market demand. By integrating recycled feedstocks, mills can effectively balance supply and demand. Doing so ensures sustainable and resilient growth in the region's forest products sector.

3. Promote the Growth of Mass Timber Construction

Mass timber construction, particularly with cross-laminated timber (CLT), has seen a rapid rise in popularity throughout the US. The growth has transformed the materials landscape of both residential and commercial projects.

Its appeal extends beyond just aesthetics. The environmental benefits of using mass timber, such as reduced carbon footprint and renewable sourcing, align with growing sustainability goals.

Additionally, local governments and building codes are increasingly supportive, adapting to incorporate taller wood buildings and streamlined permitting processes. This makes mass timber a feasible choice for larger-scale developments.

The momentum is evident with over 1000 mass timber projects currently announced or underway in the US. These projects reflect a remarkable shift towards environmentally conscious building practices.

Mitigating Supply Chain and Market Challenges

Along with opportunities come challenges. Identifying areas that require additional focus can help mitigate disruptions. We've outlined some of the challenges we've seen below:

Supply Chain Imbalances and Disruptions

The forest products sector is currently navigating challenging supply chain imbalances, largely influenced by environmental factors and regulatory changes. An increase in wildfire frequency and severity, such as the 2023 conflagrations that swept through Oregon and Washington, has disrupted the raw material supply. It has caused delayed operations and directly impacted timber availability.

In tandem with these environmental challenges, more stringent sustainability requirements, including the European Union Deforestation Regulation (EUDR), have imposed additional compliance burdens on exporters aiming to meet European market demands. These factors combined create a volatile environment, demanding adaptive strategies from industry stakeholders to ensure continued supply chain resilience and market competitiveness.

Economic and Market Volatility

The forestry market in the Northwest US and Canada has experienced significant fluctuations in timber prices, partly driven by trade uncertainties that have created an unpredictable economic environment. These market disturbances have forced stakeholders to navigate significant volatility, making strategic planning more complex.

As the use of sawmill byproducts like chips and residues for pulp feedstock increases, the demand for traditional roundwood pulpwood and whole tree chips has sharply declined. This shift has created significant challenges for landowners, loggers, and wood dealers, particularly those dependent on pulpwood sales to support forest thinning and timber stand improvement efforts.

With fewer buyers in the pulpwood market, landowners are often left with underperforming timber stands, while suppliers face reduced opportunities to sell lower-grade materials. The result is mounting pressure on the entire wood supply chain, threatening both profitability and long-term forest health in the region.

United States South Softwood Pulplog Prices

Source: WoodMarket Prices

Compounding these challenges are labor and workforce issues, the most recent being the US port strikes announced on October 1st. These strikes have further impacted the market by disrupting supply chains and exacerbating existing logistical difficulties, prompting the industry to address labor relations and workforce stability to secure its future resilience.

The Shifting Landscape of the Forest Products Sector

Recently, the forest products industry has seen significant consolidation with larger corporations frequently acquiring smaller businesses. This trend helps companies achieve economies of scale, streamlining operations and cutting costs. However, it also leads to less competition and fewer opportunities for smaller, independent operators who may struggle against the industry's giants.

Another trend influencing the industry is the relocation of operations. Many companies are moving to the US South, attracted by stable feedstock costs and lower labor and energy expenses. This strategic shift is spurring reinvestment and revitalization in the area, making it a significant player in the forest products sector.

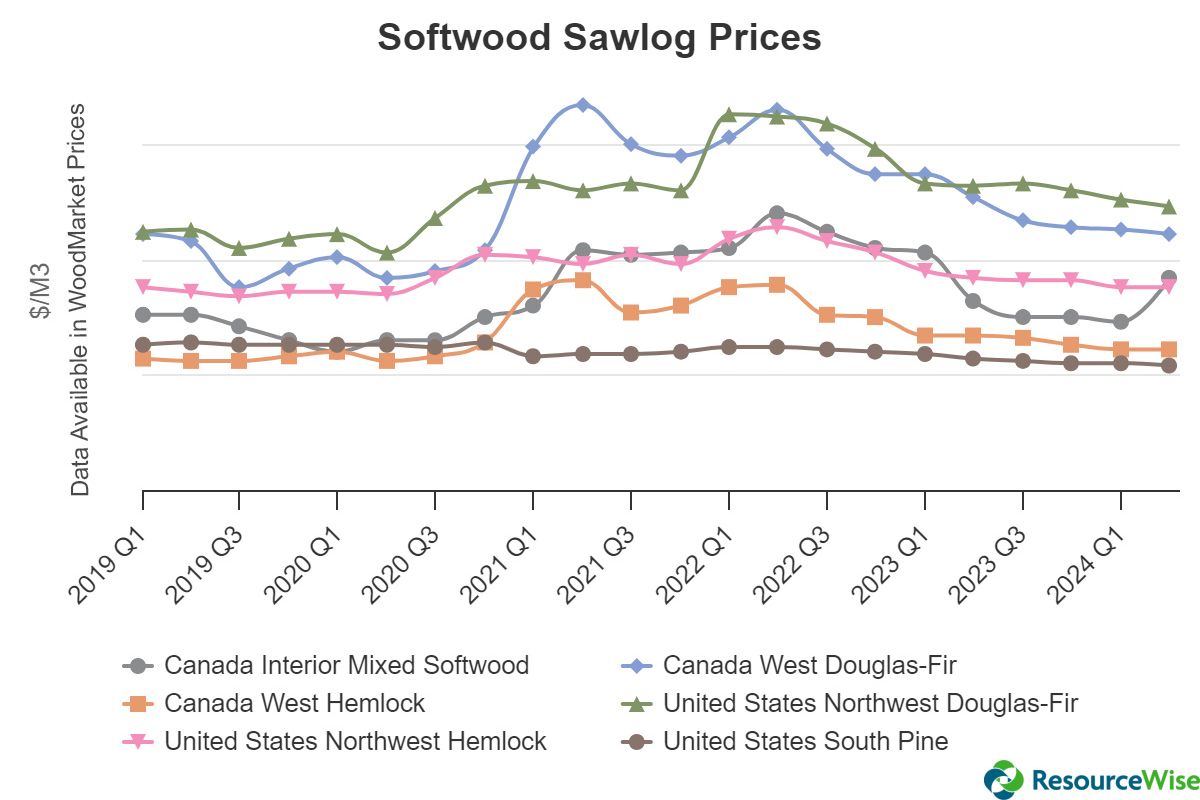

ResourceWise data shows a significant difference in market dynamics between regions. For instance, sawlog prices in the Northwest have demonstrated noticeable volatility compared to the prices in the South. This economic fluctuation places additional pressure on high-cost mills, particularly in the Northwest, where we have witnessed a number of sawmill and pulp and paper mill closures throughout 2024.

Source: WoodMarket Prices

Unlocking New Value in Wood Beyond Pulp and Lumber

Looking forward, the forest products industry is poised to play a crucial role in the markets focused on decarbonization. This includes the development of sustainable aviation fuel (SAF), biochar, pellets, carbon capture storage, and e-fuels.

The question arises: Does wood offer more value than merely being a source for pulp or lumber?

The answer is increasingly affirmative, especially with government incentives like the Inflation Reduction Act (IRA) opening new revenue streams for producers. Pellets, in particular, have emerged as a vital component of biofuels, serving as a renewable energy source that helps reduce reliance on fossil fuels.

As the United States maintains its status as the world's largest exporter of pellets, this market presents a significant opportunity for growth and innovation. With heightened regulation and a global shift towards sustainable energy solutions, the demand for pellets, biochar, and SAF is expected to positively impact the forest products sector. It underscores the strategic importance of these resources in our transition to a more sustainable future.

Source: WoodMarket Prices

Strategic Growth in the Forest Products Value Chain

Despite the presented challenges, the forest products industry's future holds promising opportunities. Emerging markets in bioenergy, biochar, and mass timber offer new pathways for growth. With a focus on efficiency, innovation, and sustainable practices, the industry can navigate current challenges and capitalize on these opportunities to ensure a resilient and profitable future.

As we move forward, monitoring these trends will be essential for making informed decisions and achieving strategic objectives in the forest products value chain.

Iran War Oil Market Turmoil is Quietly Supercharging Biofuel Profit

Biofuels Market Update: Iran War, Tariff Strikedown, and 45Z Updates

Key Trends and Challenges to Watch in the Finnish Forest Products Industry

The Finnish forest products sector plays a crucial role in the global pulp, paper, and forest products market. Its unique landscape is shaped by...

ResourceWise's 2025 Forest Products Industry Predictions

The forest products industries faced a year of significant change in 2024, marked by shifting market dynamics and unexpected challenges. From...

Reviewing ResourceWise’s 2025 Forest Products Industry Predictions

Each year, ResourceWise publishes a set of predictions outlining how we expect the forest products industry to evolve over the coming year. As we do...