Bio-Bunker Premiums Rebound as Oil Market Disruption Eases

45Z Final Rules are Coming in November. Now is the Time to Plan.

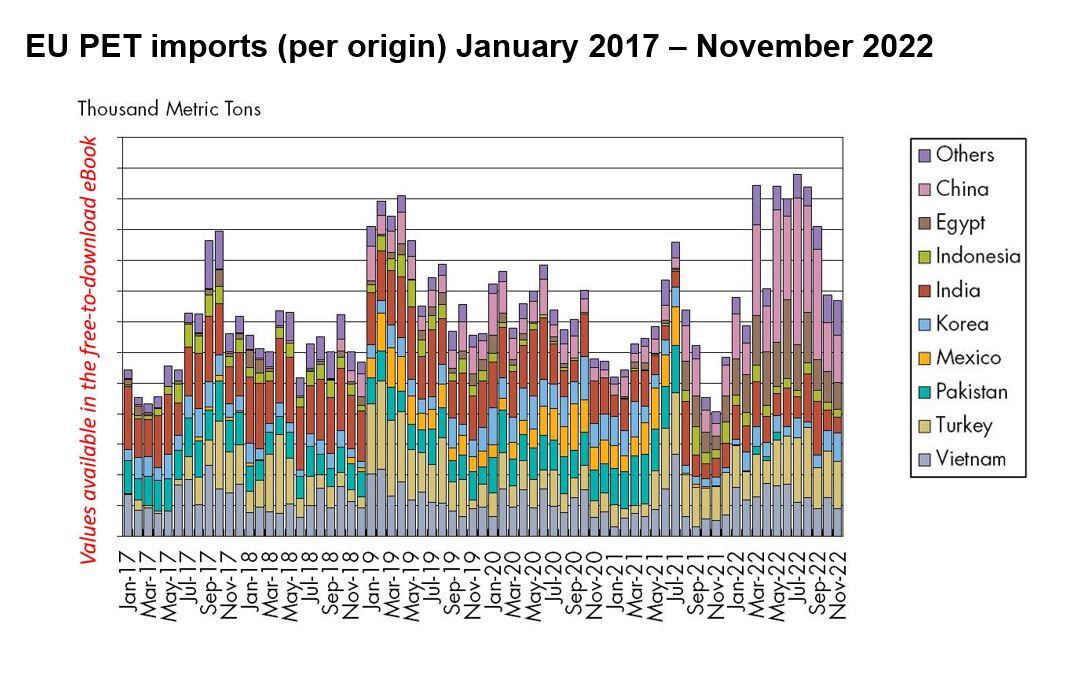

PET & Its Raw Materials: Outlook for 2023, & 2022 in Review

As we look to the PET sector's high season - Q2 2023 - market participants will be keen to lower the paraxylene cost disparity compared to Asia. It...

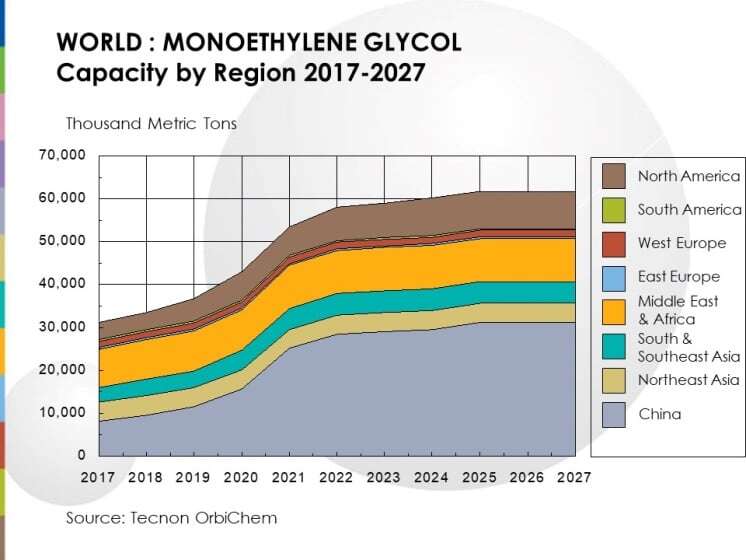

MEG: Global Overcapacity, Regional Tightness - For How Long?

Everything that happened in 2020 was impossible to imagine, as is the current situation in the petrochemical industry, and glycols are no exception....

1 min read

Engineering Thermoplastics: Calming Markets or More Chaos Ahead?

After the tumultuous start to 2021, engineering thermoplastics market participants were expecting a return to more representative activity starting...