Already high, volatile and uncertain gas prices – within Europe in particular – were exacerbated by the suspected sabotage of Baltic Sea gas pipes at the hands of Russian agents earlier this week. Just as initial improvements in gas and energy prices began to trigger a hint of positivity in businesses in recent weeks, a further threat to supply sparked shockwaves.

The climb in gas and energy prices has led to mounting cost pressures for both raw materials producers and downstream industries.

Producers throughout the value chain are experiencing squeezed margins, with some reducing rates and even considering temporary shutdowns affecting both supply and demand. Against a backdrop of economic uncertainty, companies will be rethinking their budgets and how they distribute resources.

Overview

(click in the table of contents to go direct to your chosen chemicals or products analysis)

Mixed xylenes

Ammonia, polyurethanes & BDO

Fatty acids & glycerine

Oleochemicals

Butyl acrylate

Methyl methacrylate

PVC

Epoxy resins, bisphenol A & epichlorihydrin

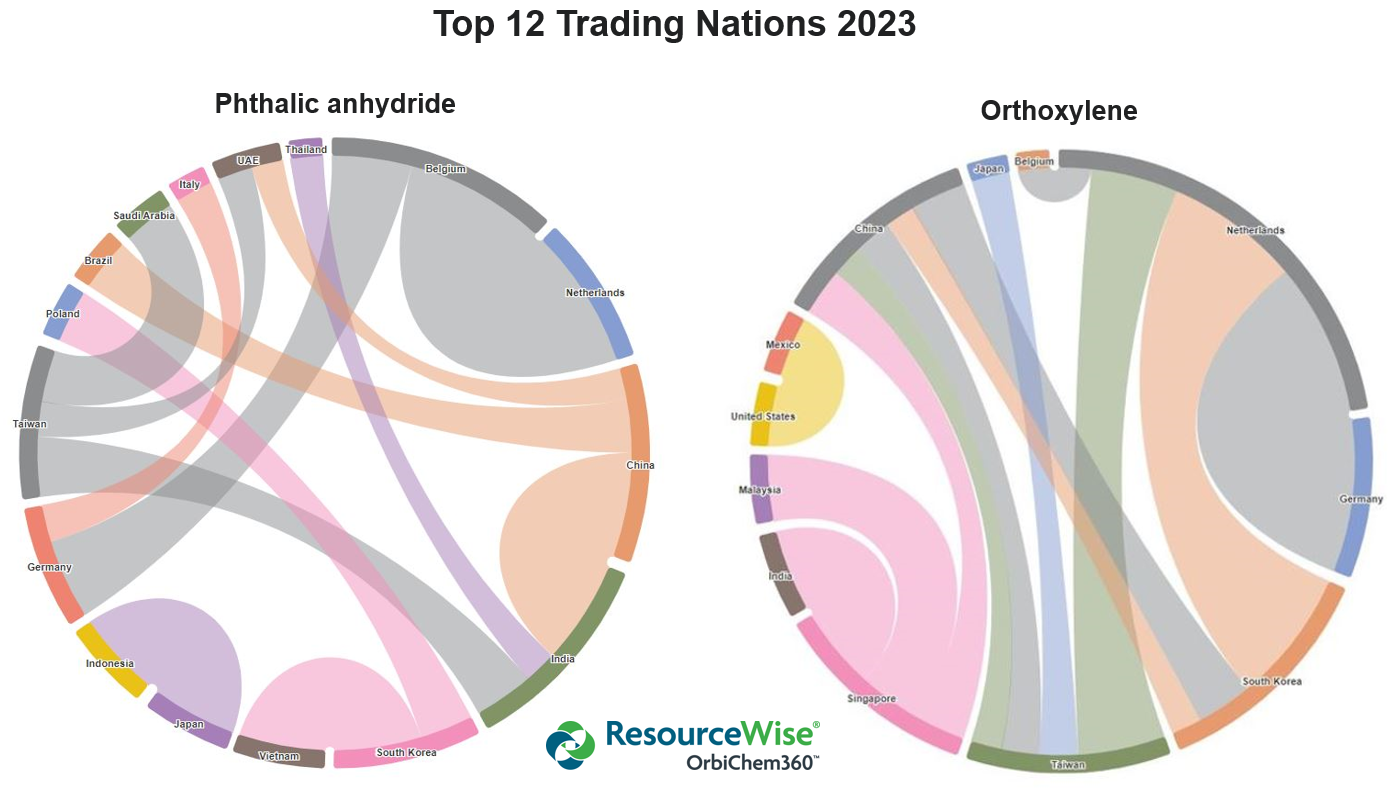

Complex xylenes

The recent rise and fall in the price of mixed xylenes compounded a complex situation. Mixed xylenes are key chemical feedstock in industry sectors including PET, PVC and plasticisers. Expert analysis of the mixed xylenes price irregularity is directly accessible via this link.

As the EU leadership worked towards its emergency intervention package during September, gas and energy prices improved somewhat. If continued, it may have stimulated activity within orthoxylene, phthalic anhydride and downstream industries - a desirable scenario as previously weak Asian markets recovered significantly from August into September. Regains in China and its neighbouring nations could, in turn, reduce imports.

At the same time, damage to Nord Stream 1 & 2 may trigger further price increases, weighing on production costs/prices and market sentiment. Both the results of the prompted investigation into the Baltic Sea pipeline damage, and the full reaction from gas, energy and petrochemical markets remains unknown.

Ammonia, polyurethanes & BDO

The energy crisis equals turmoil for Europe’s ammonia market. Gazprom severed gas deliveries to Europe, forcing shutdowns and production cuts. Five majors reduced output, leaving buyers reliant on imports to meet contracts. Ukraine’s Odessa and Yuzhny ports reopening was news well-received this summer, insurance premiums have made shipping costs so prohibitive traders are spurning the region.

Energy costs have narrowed polyurethane margins, and they may escalate further this winter. Producers are struggling to pass their production costs onto buyers – who themselves see their customer base’s demand weakening. Gas-related price adjustments remain unreported, perhaps due to low demand preventing price escalation. Without consumer appetite for new furniture, cars and mattresses, the sector struggles. Polyols are currently particularly weak, with a long hard winter expected.

With BDO markets weak and expenses escalating, European facilities are vulnerable to cuts and shutdowns. Rising natural gas and raw materials costs, cheap imports plus low demand triggered European market imbalance. Buyers are caught between hard-to-resist low-priced Asian imports and awareness that this supply source quickly disappears when Chinese demand grows. Domestic supply might dwindle if high production costs force European manufacturers to reduce operating rates.

Maleic anhydride

Uncertain about their production levels going forward, maleic anhydride (MA) customers are sticking to the sidelines. Polynt’s late August production unit closures announcement complemented this wait-and-see approach.

Some see potential for Europe’s high energy costs to jeopardise regional producers’ ability to compete with their Asian counterparts. As explored in our blog post Energy dynamics in China’s chemical sector: Balancing resource, although Asian producers’ power costs have risen they remain significantly lower than Europe’s.

And in fact – akin to BDO – MA surpluses arising from weak demand within China’s markets have become cheap MA imports into Europe, dragging down local market prices.

Fatty acids & glycerine

A prime example of how Indonesian producers shifted large volumes to the US when demand in China waned is reflected in recent fatty acids and glycerine trade trends. US prices dropped dramatically these past months as a result.

Oleochemicals

Beyond the summer holidays even, oleochemicals industry demand remained soft.

Butyl acrylate

Dwindling downstream demand in Europe’s butyl acrylate (BA) market and a slew of Asian imports that reduced BA spot prices significantly these past three months, the lack of Russian BA in the European market is not too problematic. However, as Russia continues to supply BA to the Turkish market well below the market average price, this market has seen extremely low prices, and this has been exacerbated by competition for volume from various other exporters such as China and Saudi Arabia.

For European producers however, production costs remain very high – particularly for non-integrated producers exposed to the high cost of oxo-alcohols driven by gas prices hikes. Arkema, for example, has a surcharge on BA and 2-EHA related to the previous month’s gas price and all focus is on managing future pricing issues.

Methyl methacrylate

Major methyl methacrylate (MMA) producer Mitsubishi Chemical Methacrylates kept its UK plant shut following an extended shutdown. Instead, the firm is importing MMA from its other sites worldwide, while other producers have been running at reduced rates for months. The market feels the burden of ongoing slow demand and high production costs, as well as low-cost imports which have contributed to negative price sentiment in Europe.

PVC

Converters in Ukraine and Russia are still running. Russia has been seeing a rise in PVC demand lately, however, this may be short-lived as Putin’s mobilisation order may begin to dampen this growth.

The Turkish market is still importing some Russian PVC – find out more about Turkey's PVC supply here – but some buyers prefer to avoid Russian product as supply may be unstable and have been instead looking to the US market for PVC as supply from Europe is very expensive.

Epoxy resins, bisphenol A & epichlorohydrin

Markets are inundated with material from Asia and China at vastly much cheaper prices amid a softening market. Domestic European producers – crippled by high energy and production costs – are unable to compete and continue to lose market share. They can react in three ways: drop run rates according to demand or completely shut down. Or they could jump on the bandwagon and buy raw materials from China and Asia too, therefore reducing their exposure to European feedstock trends.

Contract negotiations for 2023 are imminent but buyers are stalling because demand next year remains unclear. They do not know what volumes to allocate to contracts with their high-priced domestic suppliers.

It is possible that some volumes will be placed in the spot market to take advantage of low offers, but this could lead to volatile markets next year. Supply could easily disappear if demand in China picks up again. In the meantime, upstream raw materials could also become in short supply; market sources believe phenol/acetone operating rates in Europe have been reduced to 60%.

Without alternative cheaper sources of energy help reduce production costs, Europe’s market fundamentals will remain tough. In the short term, natural gas values will continue rising following the reportedly ‘unprecedented’ damage to the Nord Stream pipelines 1 and 2 in the Baltic Sea.

The other scenario is that demand in China picks up again and this will help to reverse current trade flows; market participants are hoping that consumer confidence will resume following the Lunar New Year holiday next year. And in the unlikely event that the Russian/Ukraine war ends soon, Nord Stream pipelines 1 and 2 now face months of repairs.

Free white paper download:

Will the Russian-Ukraine war trigger more renewable hydrocarbon investments?

(Form at the bottom of the blog post)

Nylon & polyester

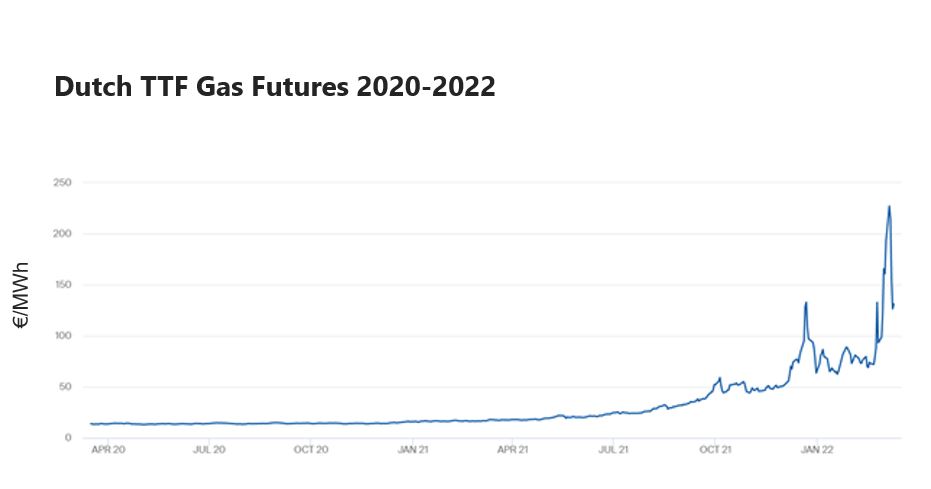

The European polyester industry is not immune to the uncertainty and volaility around gas prices. TTF values – a representative reference for energy prices in the European petrochemical industry – were stabilised below €90/MWh during the first half of June, increased to between €150 and €175/MWh in July and peaked at €346/MWh at the end of August. As of late September, they set slightly below €200/MWh. TTF values in October-November 2021 – when deltas/contracts for 2022 were negotiated – averaged €50/MWh.

High energy values are impacting production cost leading to high disparities on European contract prices for paraxylene (PX) and monoethylene glycol (MEG), as well as impacting adders/deltas for PTA, PET, and PIA prices.

European PET producers find it difficult to match/discourage PET imports due to the impact of high, volatile and uncertain energy values in different feedstocks (PX-PTA, MEG and PIA). Despite the high PTA deltas or MEG contract prices in Europe compared to other regions, these values do not provide profitability to producers. In this situation, they claim poor profitability and they prefer to lower operating rates than sell at these levels.

Volatile & uncertain

Such volatility and uncertainty already changed the way raw materials (PTA deltas) were negotiated in recent years, with a move from yearly to quarterly or even monthly deltas/adders to cope with the high volatility. There have been proposals that include energy clauses with the goal of adjusting the deltas/adders depending on the level of gas/energy values.

Energy clauses could reduce risk to participants along the chain in 2023. High disparity in PX and ECP values means a more competitive price (cost to produce PTA, PET) in Asia and a potential threat for imports of PX and downstream products, including PTA and PET.

Downstream companies using PET are being impacted. It is understood that convertors (film, preform, packaging producers and others) have communicated to customers that contracts need to be renegotiated to deal with increases in energy.

The high cost of freight for containers from Asia to Europe, which allowed higher disparities in raw materials while not having a direct effect on higher imports, has begun to decline, settling import parity for all products in the chain well below European contract values.

The last word to Ukraine

After over half a year defending itself from Russian aggression, Ukrainian demand appears to be picking up again. Yuriy Shafran is the co-founder of Ukraine-headquartered OSV a polyurethane (PU) processing machinery maker and raw materials supplier.

As revealed in a Russia/Ukraine war analysis blog post we published earlier this year, Shafran relocated to the company’s satellite site in Poland with some fellow colleagues. The company's Ukrainian operations reopened in September with a staff base of nine. The facility has moved from its former location to Kyiv due to the Russian occupation.

Shafran told Tecnon OrbiChem that demand was increasing in Ukraine's agricultural and manufacturing markets. 'Business in Ukraine is growing compared to April or May, creating markets for polyurethanes, solvents and pigments. We believe in a few months we will have much more progress too. We remain grateful of our customers' trust in us.'