Hira Saeed

Hira Saeed

Historically, the chlor-alkali process is one with numerous environmental and health concerns since the diaphragm cell process and mercury cell process were first commercialized in the late 1800s.

These processes, which have been used for the production of chlor-alkali products for over 100 years, include the use of mercury, asbestos in the diaphragm cell process and the production of toxic chlorine-containing chemicals.

Since the 1890s, there has been much innovation in the industry including the development of the membrane cell process in 1970. This has allowed the phasing out of mercury cell plants in accordance with the Minamata Convention on mercury in the last decade. Currently in Europe, the overwhelming majority of producers have converted to the membrane cell process. This is in line with European Union regulations.

The 27th Tecnon OrbiChem and I•C•I•S World Chlor-Alkali Conference takes place in Singapore from 27-28 June 2024.

How can green caustic soda drive carbon neutrality? What can we expect from hydrogen and clean energy? And how is the chlor-alkali industry contributing to the global drive for sustainability? These questions will explored in this panel discussion on day two of the conference.

Read more on the event agenda in our earlier blog post A World Chlor-Alkali Conference in Energy Turbulent Times, or register to attend below.

Now, as the world moves towards Net Zero goals, the focus has shifted to green chlor-alkali products. The chlor-alkali process converts sodium chloride and water to chlorine, caustic soda, and hydrogen as a byproduct. For many years, the hydrogen produced in this process would be vented.

As the technology to harness hydrogen as a greener, low-carbon energy source emerges, it will be key to achieving net-zero goals.

However, as modern technology to harness hydrogen as a greener, low-carbon energy source emerges, it is becoming clear, particularly in Europe, that this will be key to achieving net-zero goals.

Green Hydrogen: A Promising Prospect

Most green hydrogen is produced by the electrolysis of water using a renewable energy source, in contrast with grey hydrogen which is produced from natural gas or methane without carbon capture.

Industry body Euro Chlor says the European chlor-alkali sector produces 0.27 million tons of hydrogen annually. This hydrogen is increasingly recovered and considered “green” when renewable energy is used for the chlor-alkali process. The hydrogen produced may be eligible for "green hydrogen" certification depending on the carbon footprint.

One company that has achieved green hydrogen certification in Europe is INEOS Inovyn. It was certified under the ISCC (International Sustainability & Carbon Certification) PLUS scheme at its Antwerp site in 2023.

Dutch firm Nobian is another company focused on green hydrogen. Nobian is taking steps to reduce scope 3 emissions using green hydrogen produced by the company as transport fuel to move emissions-free salt to its southern Netherlands Botlek plant.

Source: International Energy Agency

Source: International Energy Agency

Green Caustic Soda is Drawing Investment

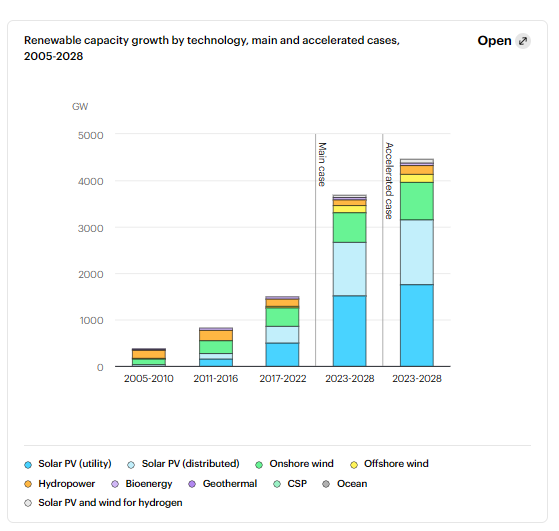

As renewable energy has become more available, the possibility of producing green chlor-alkali products has resulted in much investment throughout Europe with EU Climate goal deadlines approaching fast. While the economic downturn has temporarily drawn attention away from environmental goals, most accept that the Green Transition will soon become unavoidable.

Since 2021, Germany-based Vinnolit has offered "green caustic soda" which is produced at its Knapsack and Gendorf sites under the brand name GreenVin. The carbon footprint of the green caustic soda is 30% lower than Vinnolit’s conventional caustic soda.

In February, INEOS Inovyn announced a new ultra-low carbon range of chlor-alkali products, including caustic soda, caustic potash and chlorine. Carbon emissions of up to 70% can be reduced using the products, according to INEOS' announcement.

Many other sites across Europe are taking steps to source more renewable energy and reduce their carbon footprint while not officially producing green caustic soda.

Who Will Purchase Green Caustic Soda?

A major roadblock to the widespread use of green caustic soda is the economic factor. These products come with price premiums due to the higher cost of renewable energy.

In Portugal and Spain, the percentage of energy from renewable sources in 2023 was 61% and 53%, respectively.

Some regions have a higher advantage than others in terms of renewable energy, for example in Portugal and Spain, the percentage of energy that came from renewable sources in 2023 was 61% and 53%, respectively.

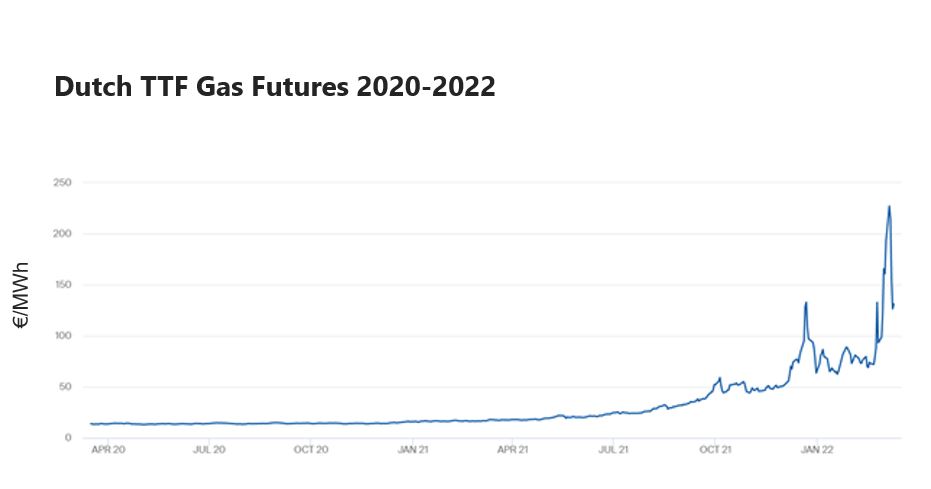

This is from hydropower, wind and solar for the most part. In addition, the spikes in energy costs caused by the Russia-Ukraine conflict have renewed European countries’ interests in renewable energy which will play a large part in the transition to net-zero by 2050. This includes REPowerEU, which set out in May 2022 to help to diversify the EU’s energy supplies and decrease reliance on Russian gas.

This is being achieved by speeding up the green transition by promoting investment in renewable energy. In the short-term, the increased investment will support companies in producing lower carbon footprint chlor-alkali products.

Source: International Energy Agency

Source: International Energy Agency

While many chlor-alkali producers are taking steps to reduce their carbon footprint, many buyers remain reluctant to pay premiums for such products. This is not industry specific and more specific to buyers and their company’s missions, though for certain industries, green caustic soda is lower on the list of priorities.

Alumina: An Energy Intensive Industry

One such case is the alumina sector, which is very energy intensive. There has been little focus on green initiatives in this sector due to the nature of the industry, though, the initial route to decarbonization would be through investing in renewable energy.

The majority of emissions from this sector are scope 1 and 2 emissions from the high energy intensive process. The purchase of caustic soda would be a smaller scope 3 emission, which to some alumina producers would not justify the price premium that purchasing green caustic soda involves.

In any case, the alumina industry has more complex environmental issues than the emissions from caustic soda.

Pulp and Paper Sustainability

The pulp and paper sector is another high energy-intensive sector more likely to invest in renewable energy than green caustic soda in the short-term. Some individual companies however—that are more focused on net-zero goals—may transition to green caustic soda sooner.

Green caustic soda's high prices discourage buyers but inquiries about cost and carbon footprint calculations are increasing.

While there are some environmentally-conscious buyers, they are the minority.

While the high price for green caustic soda is discouraging for buyers, there have been some inquiries about cost and carbon footprint for calculation. Perhaps they will begin to pave the way to a more sustainable chlor-alkali future. While chlor-alkali markets feature some environmentally-conscious buyers, these remain the minority for the time being.

Driving Sustainability: The European Green Deal

Though cost pressures remain critical in the transition to green caustic soda, regulations, particularly the European Green Deal, will likely be the main driver. The European Green Deal sets out to ‘make the EU’s climate, energy, transport, and taxation policies fit for reducing net greenhouse gas emissions by at least 55% by 2030’ and then have zero net emissions of greenhouse gases by 2050. This will eventually push buyers towards purchasing green caustic soda to meet sustainability deadlines.

Join ResourceWise at AFPM's International Petrochemical Conference 2025

%20in%20price%20per%20ton%20twice.jpg)

Chlor-alkali 2022: Key Factors Driving China's Markets

China’s Dual Control Policy sharply reduced caustic soda production in the country in Q4 2021. The policy's impact on particular chemical value...

1 min read

How is COVID-19 Impacting the Caustic Soda Market Around the World?

Since the COVID-19 virus hit Europe in January, infection cases have been rising and while initially there was no immediate impact on the market,...

Ukraine-Russia: Trade Impact Analysis

Heavy sanctions continue to cripple trade between Russia and the Western world as a growing number of companies cease operations in Russia. But...