Jane Denny

Jane Denny

When carmaker Porsche launched its iconic “ducktail” rear spoiler to boost the 911 Carrera RS 2.7’s aerodynamics, the entire vehicle weighed under 1000kg. The year was 1972, and many other cars on the market weighed twice as much.

Firmly in innovation mode, Stuttgart-based Porsche used feedstock from US-based chemicals company DuPont—developer of the ‘stronger than steel’ polyamide material branded “Nylon” in 1939—to take its flagship vehicle to the next level.

Knowing Nylon stockings’ durability came via polyamide 66, Porsche engineers focused on a composite of the material—namely glass-reinforced (GRF) polyamide. They realized that it matched the heat and abrasion resistance of irons, metals, and alloys, a game-changing recognition. Today, over 10 percent of the plastic composition of every vehicle produced globally is polyamide (PA).

Intake Manifold Innovation

Like a lung in a living being, intake manifolds—also known as inlet manifolds—are vital to automotive engine functionality. They ensure cooling air (and sometimes fuel) circulate the engine.

Intake manifolds are built to withstand pressures including pulsation, high burst, and prolonged vibration, as well as thermal cycling and shocks. Traditionally made of cast iron or alumina, PA 66 and glass-reinforced (GRF) polyamide composites have become the go-to materials for manufacturers today.

Porsche’s 1972 release of its iconic 911 model marked the first commercialized use of a PA-based intake manifold. Nowadays, PA-based feature in a range of Ford, Chrysler, and General Motors vehicles.

Replacing just one vital under-the-hood component previously made from cast iron reduces its weight from over 20kg to just a few kilograms. GFR polyamides have almost completely replaced metals in various under-the-hood automotive applications, including intake manifolds.

Sustainable Mobility

This year, however, Italian Tier 1 automotive supplier Marelli took PA-based intake manifolds to new heights. The firm developed an award-winning model using a fully recycled PA version.

Using Renycle from fellow Italian firm RadiciGroup, Marelli’s design reduces CO2 emissions by 70 percent compared to fossil fuel feedstock-based versions. RadiciGroup—a supplier of PA 6 and PA 66 to automotive OEMs worldwide for many years—uses post-industrial material diverted from manufacturing process waste streams and post-consumer materials to produce Renycle.

Key to the issue is the question: What material adequately meets the required specifications at the lowest cost? For an increasing number of applications, the answer will be PA. Moreover, petrochemical-based PA will continue (by and large) to price metals and recycled plastic products out of the market for some time.

That said, sourcing fair-priced products with suitable delivery timelines becomes complicated in a globalized world. In the absence of smooth-running supply chains with stable pricing structures, transparent markets become key.

Automotive Raw Materials and Market Disruption

Volatility characterized the PA intermediates market even before COVID-19 and the 2020s. Demand from the automotive sector and plant stoppages disrupted value chains across the chemicals, along with other supply chains. Factors such as these have underpinned an interplay of oversupply and acute shortage since 2017.

Product allocation measures—which limit the amount of a product that individual customers can buy—have disrupted automotive sector procurement process. Tight markets were seen for additives and compounding materials including glass fibers for reinforced PA used to make radiator shrouds, air ducts, structural components, and reservoirs.

Regional Insights

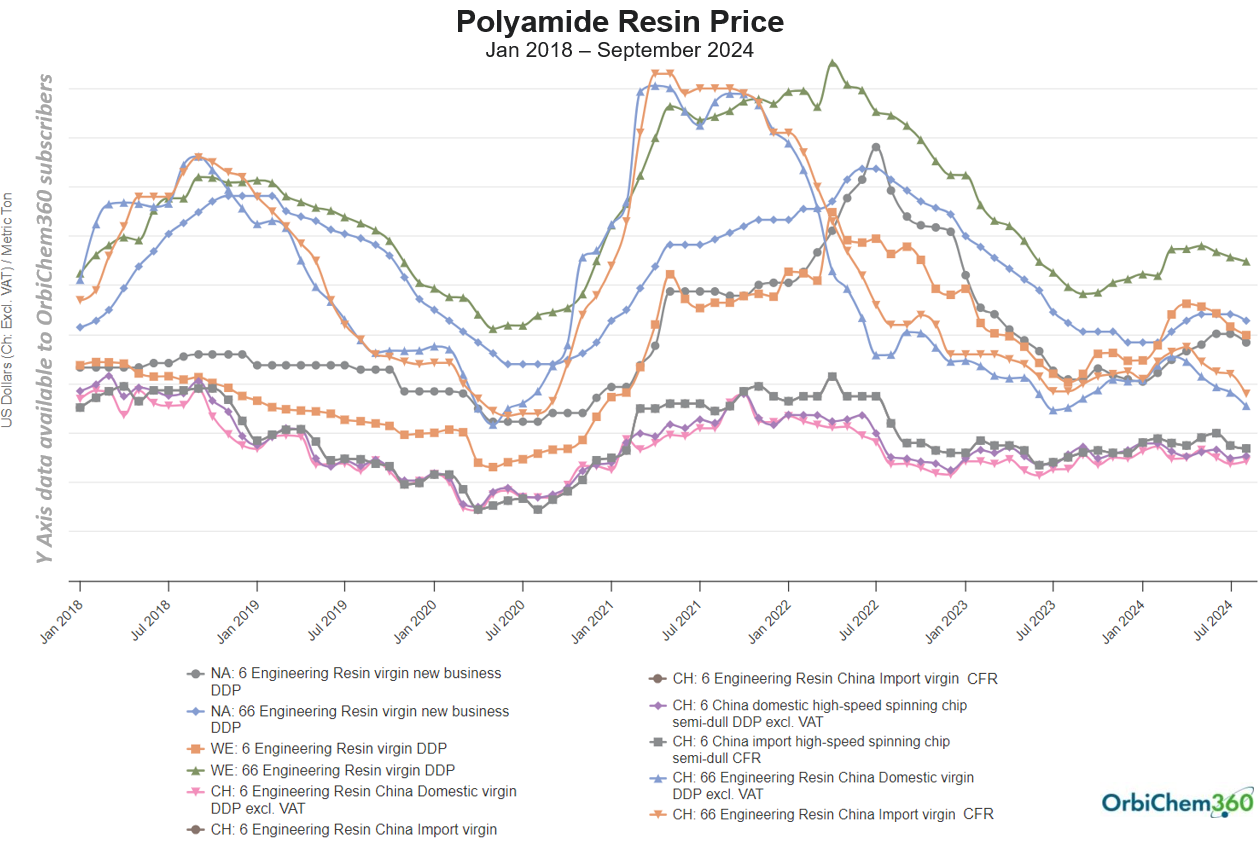

As the price graph above shows, the price of PA resins has been volatile in many regions for many years. In western Europe, it appears that prices for both PA 6 and PA 66 dropped to their lowest in the months after the COVID-19 pandemic began. The price of both products then peaked, like many chemicals, when Russia invaded Ukraine, although they had been rising for some time before the war. In the past year, or thereabouts, the region's prices for both steadily rose before steadily falling again in Q2 2024. North American price swings and trends are largely mirroring those in western Europe.

The graph shows North American and western European-produced PA demonstrate price structures above or roughly in line with those recorded in January 2018. In the case of virgin engineering resin, China's current prices are significantly lower than recorded in 2018. They are also today almost as low as they have been at any time in since the start of 2018.

Feedstock Price Fluctuation

Ammonia is a key precursor for both PA 6 and PA 66 intermediates. At the start of the production process for PA 66, nitric acid is obtained via ammonia oxidation to deliver adipic acid.

Ammonia is also used in the production of caprolactam, a precursor for PA 6. Though a steady uptrend in the feedstock's price characterizes the current market, ammonia values have been volatile in the 2020s.

Back in Q4 2021, higher natural gas costs tightened the supply of ammonia globally and triggered a three-fold increase in international prices. Our chemicals business intelligence platform OrbiChem360, shows that the ammonia price increase pushed Europe’s PA 66 economics to ‘critical’ levels.

Following Russia's invasion of Ukraine in February 2022, ammonia prices—which had averaged around $400/ton—escalated to $1,500/ton. In time, a number of major automobile manufacturers in western, and central Europe announced temporary closures due to the disruption in supplies from parts makers in Ukraine.

Forecasting Future Volatility

In 2024, a new set of disruptive influences are in play. The EU’s Carbon Border Adjustment Mechanism (CBAM) is also expected to result in higher ammonia prices. Designed to account for the carbon cost of producing imported goods, the policy aims to reduce greenhouse gas emissions and support a net zero future globally. It amounts to tax on the embedded carbon content of certain imports. As such, the ripple effect of its imposition on ammonia will be felt in the feedstock's downstream markets.

Our eBook, Understanding Automotive Sector Supply Chain Dynamics, explores the dynamics impacting engineered plastics value chains from an automotive angle.

It includes price forecast graphics that indicate whether the cost of raw materials— including acrylonitrile, butadiene, and styrene—will rise, fall, or remain flat from now to 2026.

Join ResourceWise at AFPM's International Petrochemical Conference 2025

Ammonia Shortage Triggers Supply Chain Ripple Effect

South Korea’s urea supply crunch is a stark reminder of the value in supply chain diversification. With very little means of meeting its own urea...

Ammonia: What Future for Fuels, Feedstocks and Fertilizers?

As the second-most produced chemical worldwide and the single biggest carbon-emitting chemical, ammonia is a supply chain product ripe for...

Tecnon OrbiChem: Big Brands Pivot to Engineering Thermoplastics Potential

The petrochemical and polymer industries are amidst a major realignment as companies position themselves for growth with the low carbon/circular...