Regina Sousa

Regina Sousa

Isocyanate markets improved in Q1 2020 but as the COVID-19 outbreak reached worldwide markets the picture changed once again. In previous years, spring usually brings an improvement in demand in most sectors, but this year so far is a different picture.

In Q1, the US MDI market changed direction after months of price cuts on the back of long supply and weak demand. In March, several producers announced price increases to improve margins. There was relief in the market as most players had been struggling since mid-2019. Towards the end of March, the situation changed drastically due to the COVID-19 outbreak. Demand is declining due to quarantine measures and supply is lengthy once again.

The European MDI market has seen the same picture as the US. Following months of softness, prices improved in March. One major European producer had a planned turnaround in February and March, and this helped the upward movement. However, everything changed towards the end of March as Europe was severely hit by the epidemic. Several countries are now on lockdown and only essential markets are running. The construction and automotive sectors are heavily impacted by closures and April is likely to be very weak for most players.

In China, the ongoing COVID-19 outbreak led to markets trending downwards as transport was disrupted and the Chinese New Year holiday was extended for much of February. Downstream factories were not able to operate at full capacity and demand for MDI declined. Given limited demand, producers either paused or reduced production for most of February. In March, the domestic MDI market remained weak. Downstream sectors resumed production, but demand was limited, and production rates were low due to large stocks in warehouses. Most sectors are expected to resume operations in April and demand may now begin to recover.

The North American TDI market has been under pressure from producers to increase prices as margins have been low for over a year and the market has been expecting a price correction for some time. February saw some suppliers sending letters to buyers with price increase announcements. The market firmed in March in what appeared to be a change in direction following months of low prices. The change was short-lived, however, as the COVID-19 outbreak hit the US and markets started softening again. Automotive has been particularly hit by the outbreak due to its markets being weak to begin with.

The European market is not dissimilar to the US. In March, producers attempted to improve margins by raising prices. One operator had a turnaround which helped to push price increase initiatives. Demand began to see some improvement and the market expected to start seeing recovery. Towards the end of March, the situation changed as countries started to quarantine operations and lockdowns were implemented. Demand from automotive struggles the most as the sector has been weak for a long time and is now almost fully closed in Europe. April is likely to see further closures as the transportation of goods becomes harder due to border limitations, lower labor numbers, and further quarantines. The comfort industry is also severely impacted. Most plants are running at reduced rates and, even though some may be allowed to be open again, lack of demand and difficulty sourcing raw materials is likely to lead to further closures. April is increasingly looking weak as more plant shutdowns are expected to take place.

In China, under orders from the government, most Chinese downstream factories delayed the reopening of their plants, resulting in limited demand for raw materials. TDI prices decreased significantly with few transactions taking place in the market. In March, as the COVID-19 outbreak is showing signs of being contained, downstream factories had mostly resumed operations. However, as suppliers have high levels of stocks and end-user purchasing is limited, the price of TDI kept moving downward.

The North American domestic polyether polyol market has changed significantly over the last few weeks as the country battles the COVID-19 outbreak. Prices were firming on the back of improving demand and expected growth in March but now most sectors are slowing due to the epidemic.

The polyether polyols market has seen a significant change from last month as the COVID-19 outbreak continues in Europe. Supply disruptions during March meant prices firmed but this month market fundamentals changed dramatically. Due to the COVID-19 outbreak, most foam plants are now either closed or running at reduced rates. March was a good month because most plants were running normally but as governments impose lockdowns, April is likely to be a difficult month for polyols.

The Chinese flexible foam polyol market faced limited demand from downstream industries leading to high levels of supply and difficulties clearing stock during March. The flexible foam market is expected to remain low as end-use demand was not showing signs of a strong recovery in the short term. Supply will remain more than demand for a certain period.

The market is difficult to predict for the short term due to the uncertainties surrounding the COVID-19 outbreak but most isocyanates markets are expected to remain weak. Further closures due to quarantine measures are expected and softening is the most likely scenario in Europe and the US. In China, plants are slowly restarting operations and demand is improving but not back to normal levels yet.

Sign up for our blog to stay up to date on issues impacting the global chemicals industry.

The Industries of Chemicals: How Key Markets Shape Global Demand

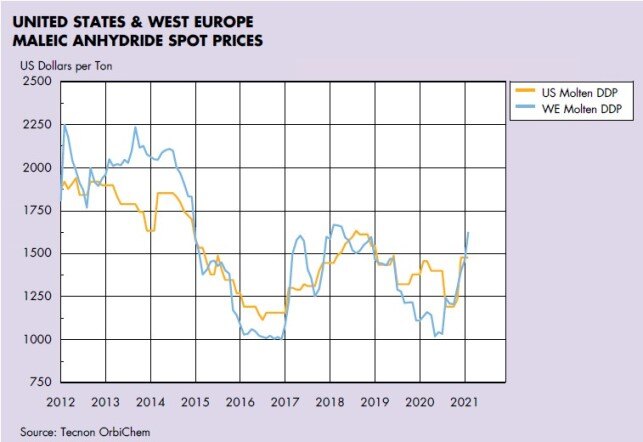

Maleic Markets Stumble Towards Recovery

Maleic anhydride markets around the world continue to reel in the face of the global COVID-19 pandemic, which has knocked out thousands of tonnes of...

Global Markets Are Slowly Returning to Normal but Concerns Remain for the Rest of the Year

Like most petrochemical markets, the global UPR markets took a big hit following the global outbreak of COVID-19 in early 2020. European and US...

Coronavirus Drives Wide Swings in Global Maleic Anhydride Market

Global maleic anhydride markets were booming in the last quarter of 2020 and the early part of the New Year. China was a little ahead of the curve...