Javier Rivera

Javier Rivera

DOE’s Updated 45Z GREET Model Brings Clarity to US Biofuels Markets

EUDR Compliance in 2026: Why Traceability Has Become a Competitive Advantage

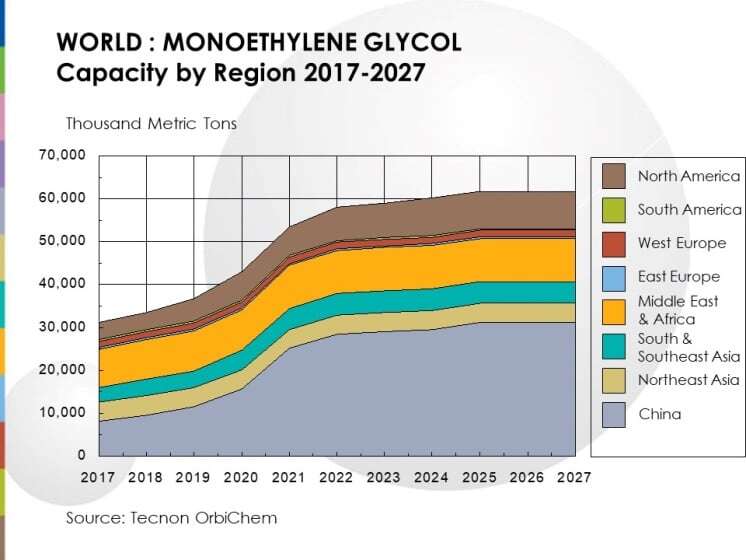

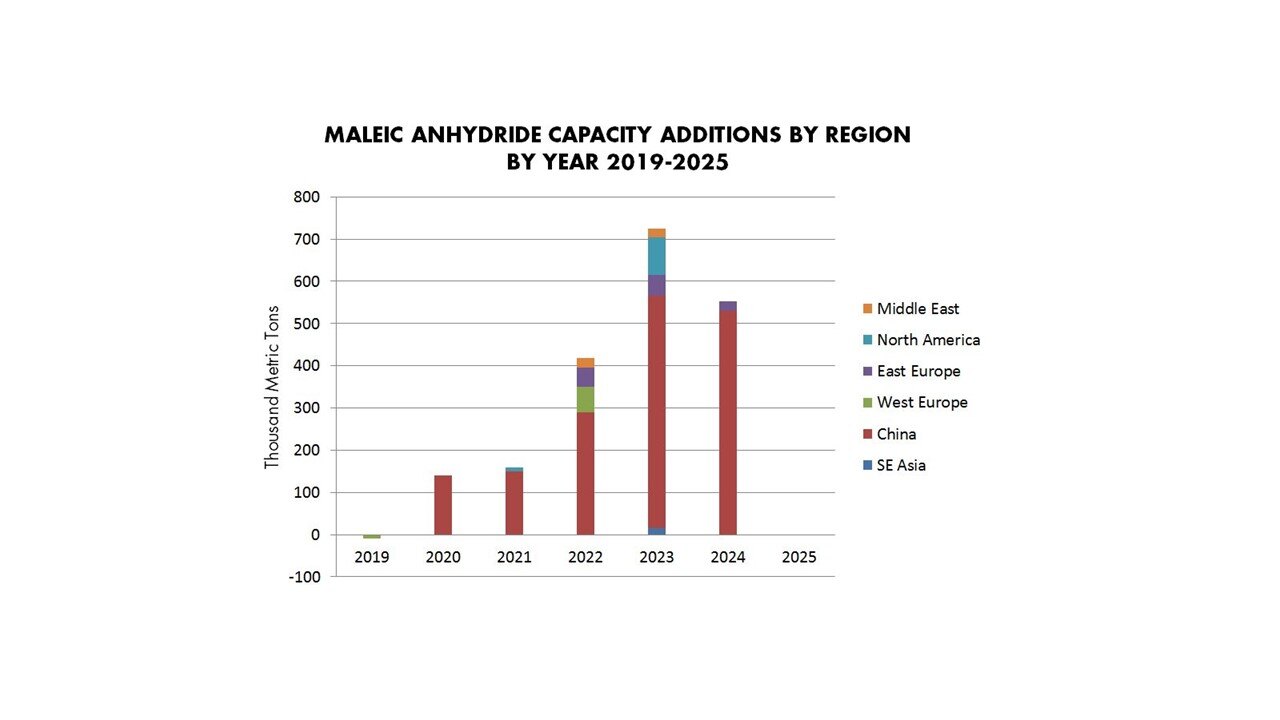

Maleic Anhydride - New entrants to market set to cause disruption

Global maleic anhydride markets have experienced a sharp upturn in late 2020 and 2021 following the negative growth seen in 2020 as markets continued...

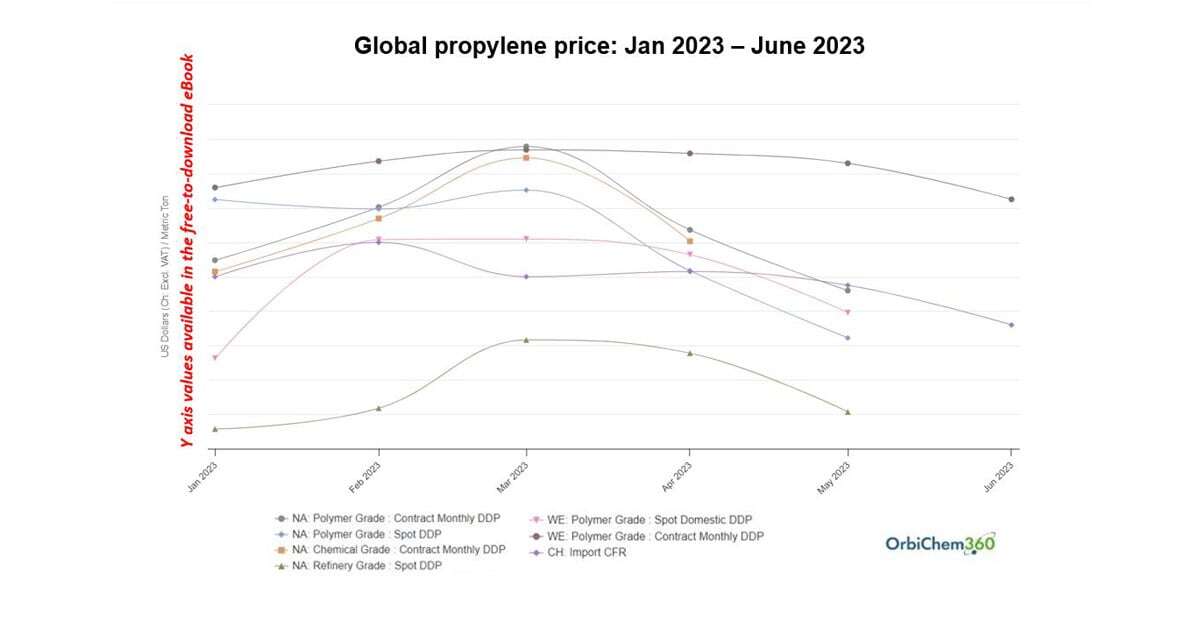

Plasticizers and Their Raw Materials: eBook of Mid-year Analysis

Plasticizer market participants and producers within the sector's supply chain – plus raw materials producers – began the year with breath baited....

Is the US Automotive Sector Strike Impacting Chemicals Supply Chains?

The automotive sector is operating in a contradictory landscape at present. This year alone, it has been subject to pent-up demand driven by Covid,...