Jane Denny

Jane Denny

As Ukraine continues to defend its sovereignty against the Russian invasion, a plethora of trade dynamics will emerge and trickle through global markets.

From the advantages of cheap oil grabs from a sanctioned Russia to the diversion of goods from central to west – as opposed to Eastern – Europe, our consultants share their insight.

Will other petrochemical companies follow Shell's buy big then abandon strategy? Which other industries will suffer most? And where might opportunity present itself?

Orthoxylene Boost to Western Europe

Russia’s invasion of Ukraine has affected the orthoxylene (OX) and phthalic anhydride (PA) value chain on multiple levels. Tecnon OrbiChem junior consultant Ben Edmunds said, "As a downstream petroleum product, orthoxylene is closely tied to crude oil and energy prices/supply."

"Therefore, the unstoppable rise in both crude oil and energy values means prices in the market will undoubtedly follow suit," Edmunds added.

Orthoxylene producers intend to divert material to the tightened West European market to meet downstream consumers' demand.

Ben Edmunds, Tecnon OrbiChem Consultant, Orthoxylene, Phthalic Anhydride and Synthetic Fibres

Some Eastern European producers refer to a nearly entire drop off in local demand, including Ukraine, since the Russian invasion began 14 days ago. "It was interesting to hear one Hungary-based producer say that that decline will not impact its production schedules," Edmunds said.

"Utilization rates are not changing because producers intend to divert material to the tightened West European market' to meet the demand of downstream consumers that are currently scrambling for available spot material,' said Edmunds.

The OX producer will continue spot business in West European markets not only to avoid reducing production rates but also due to direct enquires for trade.

Edmunds' (pictured left) focus includes markets for synthetic fibres along with orthoxylene and phthalic anhydride. He added: 'It’s unclear at this stage, but I suspect that this will only somewhat mitigate, but not entirely hold off, the tightening West European market under the current circumstances.

'The situation differs depending on whether the downstream producers have a contract for their OX supply or whether they depend on the spot market. Larger contracted customers reported manageable OX supply while other contacts indicated the spot market is scrambling to acquire material.

With multiple planned PA maintenance stoppages due in March, April and May, producers planned high run rates to build inventory ahead of outages.

"That simultaneously results in higher OX requirements as well as further reducing the excess PA available to the spot market going forward, before factoring the invasion’s effect on OX and upstream markets."

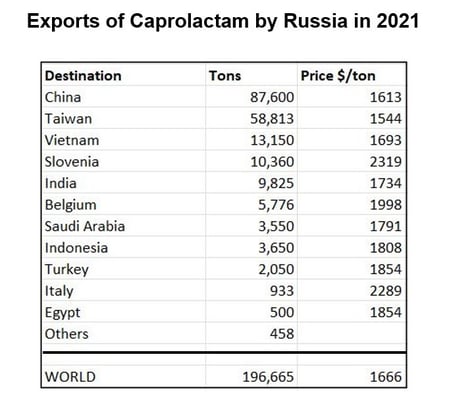

Disruption to Trade in Caprolactam

World trade in caprolactam amounts to around 550 ktpa (excluding exchanges within the European Union). Russia has accounted for about 40% of the world’s exports in recent years, though in 2021 this fell to 35%. The table details Russia’s exports in 2021.

Source: Tecnon OrbiChem

"This trade is likely to be sharply curtailed in 2022," says Tecnon OrbiChem founder Charles Fryer, "following the exclusion of many Russian banks from the SWIFT international banking exchange system."

Caprolactam buyers in Taiwan in particular are wondering whether they will be able to get any supplies from Russia in the months to come. "Also, buyers in the other countries listed as destinations in the table above will be reassessing their purchasing strategy. One of the caprolactam producers in Russia is highly dependent on exports and is likely to be finding survival very difficult," Fryer adds.

Buyers in Slovenia and Italy will not be too concerned, since alternative supplies can be sourced from West European producers, with markets currently coming out of last year’s tightness, though price escalation from rising natural gas costs will be a big worry.

But buyers in Asia will be much more concerned, Fryer says. 'Russian producers can offer very competitive prices, as is clear from the table above, by low energy costs. They will be in an even more cost-competitive position this year, following the devaluation of the Rouble. But the difficulty for Asian buyers will be the exclusion of dollar trading facilities, which will be an even greater problem for the Russian sellers.'

Circumventing SWIFT

Russian suppliers have established positions as suppliers in China, which consumers will want to foster, with the traditions of reliable and low-cost supplies. To facilitate that, Russia's logistics firm FESCO announced its acceptance of the Chinese yuan due to sanctions on payments in euros and US dollars. The announcement adds that the company continues to provide logistics services on all existing routes in full.

Already there are reports that Chinese refiners are increasingly paying for Russian crude using cash transfers paid upfront, mitigating the banking risks after most Western banks shied away from issuing letters of credit. China's state-owned trader Unipec has reportedly bought as much as eight ESPO cargoes in the Far East.

The Chinese government is trying to establish the Renminbi as a reserve currency, and some commerce between Russia and China will undoubtedly take place by circumventing the need for dollar-denominated transactions. China has established facilities for international commerce to take place using the Renminbi as the exchange currency and has set up credit facilities mirrored on Amex, Visa, and Mastercard, but they are still in their infancy.

However, it is possible that caprolactam trade from Russia to China could continue, though at volumes much reduced from those of 2021. China has a surplus of caprolactam capacity and does not need to import on volume grounds, though the Russian imports can be offered at lower prices than those from domestic suppliers.

Other Asian countries will probably have to look elsewhere for caprolactam supplies. This will be an opportunity for caprolactam producers in Japan and South Korea to expand their export business, but their spare capacity is limited, nor is much extra product available from West Europe or the USA. Maybe the Mexican producer will find renewed opportunities for sales in Asia.

Deepening Ammonia Woes

Already tight this past six months due to various European producers cutting production because of the high cost of natural gas, ammonia markets are once again under significant pressure following Russia’s invasion of Ukraine.

Russian Togliattiazot was reported to have suspended ammonia deliveries as the pipeline from Russia via Ukraine to Yuzhny closed.

Regina Sousa, Tecnon OrbiChem Consultant, Polyurethane & Intermediates, 1,4 butanediol & Derivatives

Prices began to stabilize in February 2022 following months of significant increases but this changed again in the wake of the invasion of Ukraine.

Prices began to stabilize in February 2022 following months of significant increases but this changed again in the wake of the invasion of Ukraine.

Russia is the second biggest ammonia producer and accounts for roughly 20% of the world’s ammonia exports. Significant levels of ammonia go through the Ukrainian port Yuzhny, which closed due to security reasons after Russia invaded Ukraine. Russian Togliattiazot was reported to have suspended ammonia deliveries as the pipeline from Russia via Ukraine to Yuzhny closed.

Regina Sousa is Tecnon OrbiChem’s consultant for polyurethane & intermediates, 1,4 butanediol and its derivatives.

Sousa said, "It is a bit early to predict what will happen with ammonia and other markets but sanctions on Russia, port closures, and lower supply are expected to tighten ammonia markets once again."

"Furthermore, energy gas costs are going up and will add extra stress on an already shaken market," she added.

Automotive Market Hopes Dashed

Antimony finds use deep in many supply chains. Antimony metal is used in alloys with lead and tin, for example in battery plates, solder, pewter, and ammunition. Antimony trioxide is a widely used fire retardant for plastics and pigment for paints. Antimony trisulphide is used in safety matches and fireworks.

Titanium – an aerospace industry vital but also a key chemical industrial plant component – has traditionally been supplied by Russia. With sanctions preventing Russia’s goods from reaching global markets, a diverse range of supply chains – such as paint manufacture which widely uses titanium dioxide as a pigment – will be impacted.

Used as vehicle exhaust catalysts, the availability of the metals palladium and platinum are key to a smooth-running automotive industry. Traditionally, Russia has supplied these materials to eager global markets. With sanctions, supply is likely to dry up. Aluminum – used in vehicle frames – and palladium prices both hit record highs on Monday, 7 March, according to Reuters.

Ukraine is a major iron and steel supplier and the largest supplier of noble gases used in chip making, especially neon. With the automotive industry already restricted by the global semiconductor shortage, the conflict is likely to bring it more disruption.

Speaking to BBC Radio 4 on Saturday, 5 March, principal supply chain economist Chris Rogers from freight forwarding and customs brokerage company Flexport unraveled some of the complexities of the invasion’s knock-on effects.

No-Fly Zone Impact on Freight Times

He said: 'The geographics and centrality of Russia and Ukraine means that access to their airspace is very important for rapid shipments. What we've seen is that the initial closure of the airspace over Ukraine and western Russia added about 3% to the transit times for air freight from Asia to Europe.'

With the subsequent block of Russian planes from their airspace by over 30 countries – and Russia’s reciprocal block of those same countries from their airspace – we are seeing a great restriction in the amount of transportation capacity. In this climate, rising freight costs are inevitable.

"That's now led to an increase in those air freight times to around 6% compared to where they were before the conflict began." And about the sea element to this conflict, the closure of the major ports such as Mariupol and Odessa Sea ports is restricting shipping for commodities, he said.

'It has also led to some of the biggest container lines in the world to no longer ship to Russia. And I think related to that, we're also beginning to see some customs authorities including the Netherlands restricting the export of goods directly into Russia,' Rogers added.

Maersk, one of the world’s largest shipping companies, has suspended deliveries to and from Russia, except for food, medical and humanitarian supplies.

Sign up for our blog to get the latest insights and updates delivered directly to your inbox.

Join ResourceWise at AFPM's International Petrochemical Conference 2025

Ukraine-Russia: Trade Impact Analysis

Heavy sanctions continue to cripple trade between Russia and the Western world as a growing number of companies cease operations in Russia. But...

Ukraine-Russia: Trade Impact Analysis Autumn 2022

Already high, volatile and uncertain gas prices – within Europe in particular – were exacerbated by the suspected sabotage of Baltic Sea gas pipes at...

Can China’s Engineering Thermoplastics Markets Maintain Steady Recovery from Worst of Covid-19 Downturn?

Overview of China's Economic Landscape Amid COVID-19 China, like the rest of the world, has witnessed unprecedented upheaval due to the COVID-19...