William Bann

William Bann

What the UCO Market Reveals About Crude Tall Oil Demand

What's Next for Asia's Largest Wood Pellet Supplier?

Novel Coronavirus and Chinese Petrochemical Markets – How to Anticipate the Unexpected?

What has happened so far? The novel coronavirus, a variant of the virus that caused SARS and MERS, was first identified in Wuhan in Hubei province,...

How China’s Pulp Overcapacity Is Impacting the Australian Wood Chips Market

For more than a decade, Australia has been a significant supplier of hardwood and softwood chips to North Asia’s pulp and paper producers. Strong...

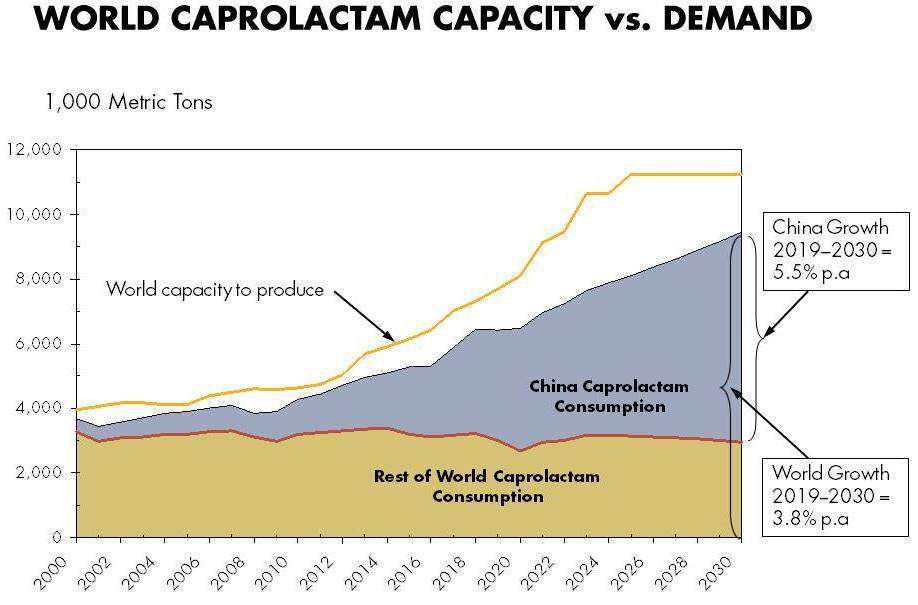

China’s Caprolactam, Adiponitrile Markets Face Opposing Forces

The outlook for polyamide market demand, the stop-and-start nature of economic recovery during the COVID pandemic, and key feedstock materials – both...