Javier Rivera

Javier Rivera

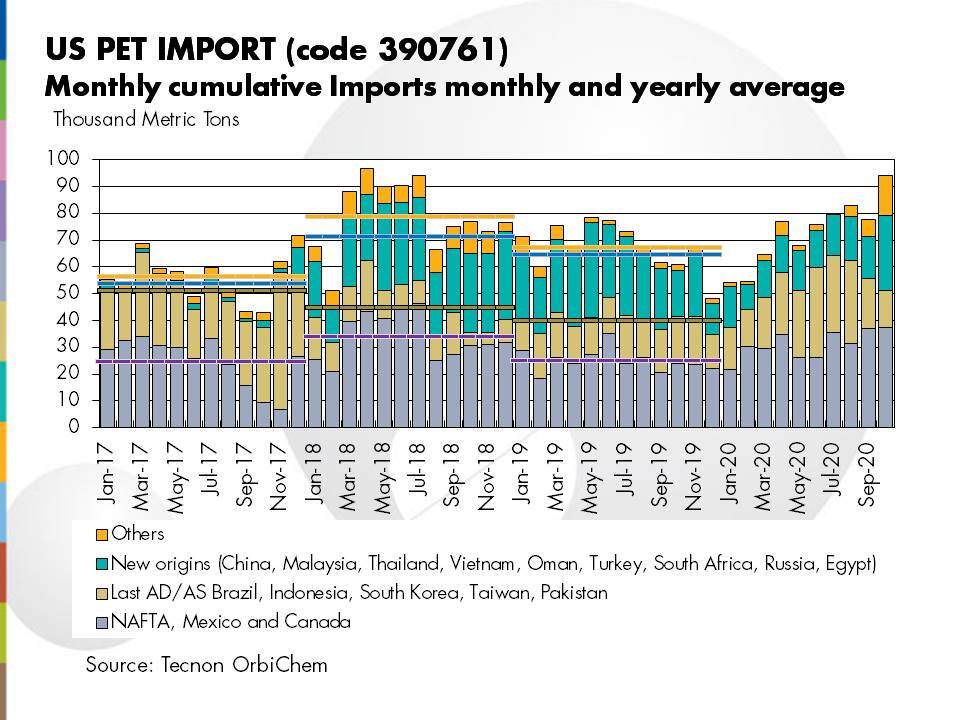

PET Supplies Range from Tight to Short to Balanced to Long. Where Are You?

Supply limitations, logistic constraints and varying demand patterns have created different scenarios for PET in each region. The South American...

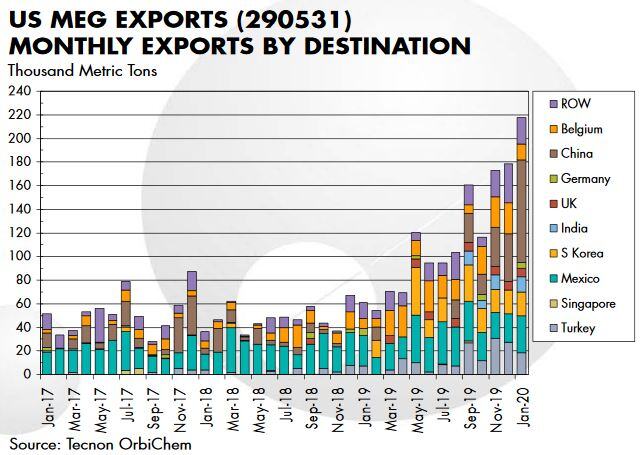

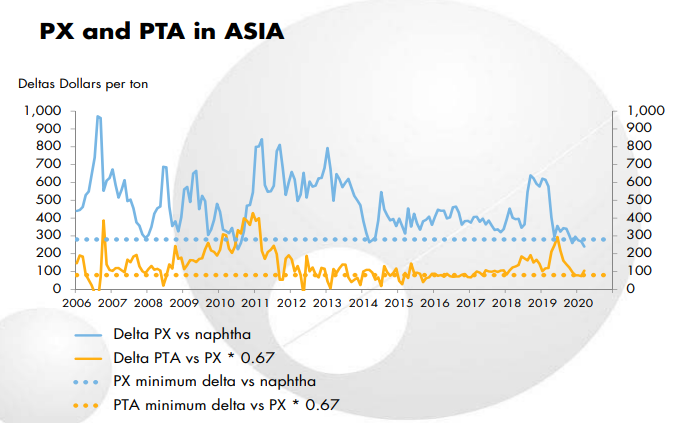

Where Should PET Resin and Polyester Intermediates be with Brent Crude Oil?

Everything is uncertain and challenges abound for individuals, industries and society at large in the context of today’s COVID-19 pandemic....

Chlor-Alkali in 2026: Why Market Insight Matters More Than Ever

The chlor-alkali market entered 2026 with a more complex set of pressures than in previous years. New capacity additions, shifting trade flows,...