William Bann

William Bann

DOE’s Updated 45Z GREET Model Brings Clarity to US Biofuels Markets

EUDR Compliance in 2026: Why Traceability Has Become a Competitive Advantage

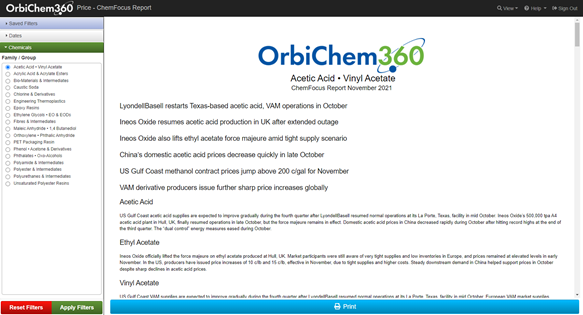

New Quick Access ChemFocus Report Tool: Step-by-Step User Guide

Tecnon OrbiChem has added a new feature to the OrbiChem360 business information platform aimed at improving access to information our subscribers...

10 Essential Steps for Navigating the Methanol Market

The methanol market has been evolving at an unprecedented pace, with stakeholders encountering various opportunities and challenges from regulatory,...

Caustic Soda Market Reverses in the Wake of US Winter Storm

The demand for caustic soda has gradually been recovering following a low point seen in Spring 2020. Currently, across much of the world, demand is...