William Bann

William Bann

The Pulp Mill as a Biorefinery: Unlocking New Revenue Streams

Bio-Bunker Premiums Rebound as Oil Market Disruption Eases

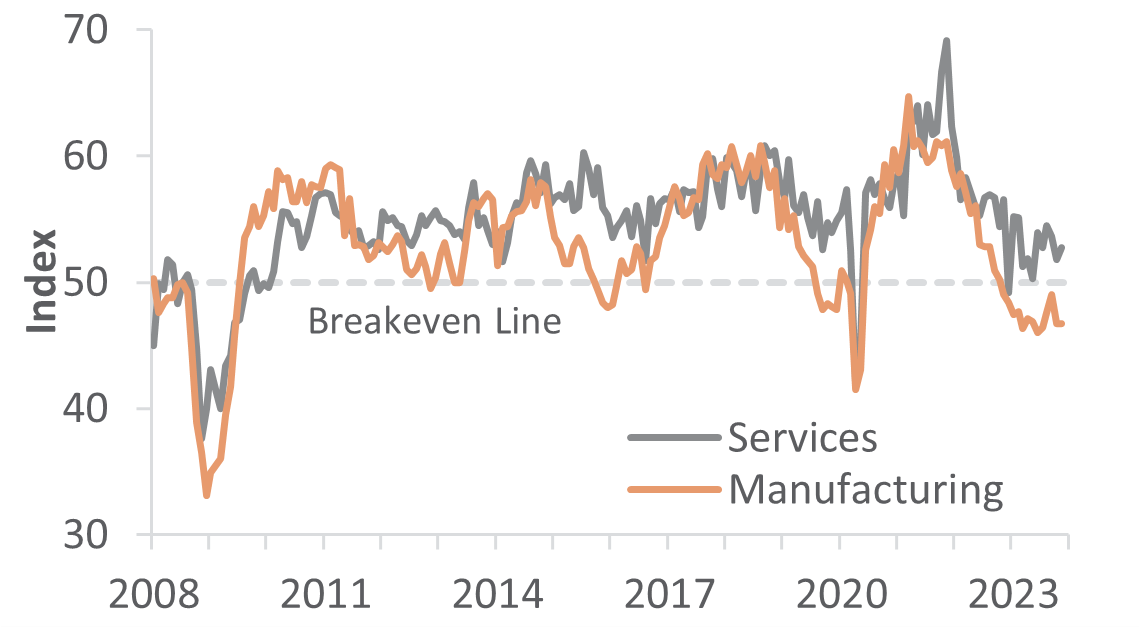

Economic Conditions Remain Unchanged, How Does This Impact the Forest Products Industry?

With economic conditions showing little variation, the forest products industry finds itself at a crucial juncture due to global conflicts and...

As the Chinese UPR Market Starts to Put Out Green Shoots: the US and Europe Face Frosty Demand

The Chinese UP resin market started to show some recovery in March after coming to a standstill in late January and remaining virtually shut down...

Orthoxylene Markets Hang in the Balance as COVID-19 Reaches New Peak

In Europe and the US, the outbreak of COVID-19 was delayed compared with Asia as the regions did not enter lockdown until March. Demand was steady,...