Jennifer Hawkins

Jennifer Hawkins

The Industries of Chemicals: How Key Markets Shape Global Demand

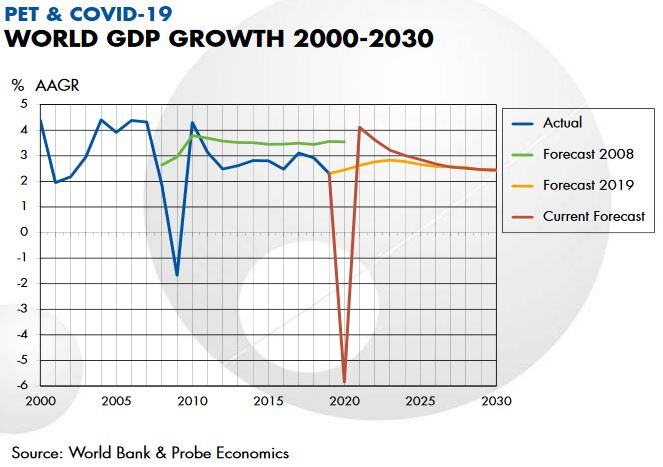

Covid-19 Related Factors Mitigate GDP Collapse for PET Resin Demand - But for How Long?

Like many consumer products, PET Packaging Resin demand is strongly linked to the health of the global economy. Based on long-term correlations with...

How Plunging PVC Demand is Behind the Recovery in the Caustic Soda Market

As the world battles to control the Covid-19 outbreak, demand in many chemical sectors is tumbling. With automotive and construction industries...

As Covid-19 Shows No Sign of Abating, What’s in Store for the Acrylic Acid Market?

Nearly nine months after the first COVID-19 cases were reported in Wuhan, China, the pandemic has had a striking but varied impact on key downstream...