For many years, the pulp and paper industry focused mainly on scale—building capacity, optimizing utilization, and competing based on cost per ton. However, this approach is quickly becoming outdated.

At the Forest Biofacts Spring Conference 2026, ResourceWise's Marko Summanen outlined how the global packaging industry is entering a fundamentally different era—one shaped by regulation, traceability, sustainability requirements, and structural overcapacity. While fiber-based packaging continues to gain share from plastic in many applications, the industry's future winners may not be the lowest-cost paper producers. Instead, they will be the companies that can manage fiber as an integrated system.

The next competitive advantage is not simply manufacturing paper. It is orchestrating the entire fiber value chain.

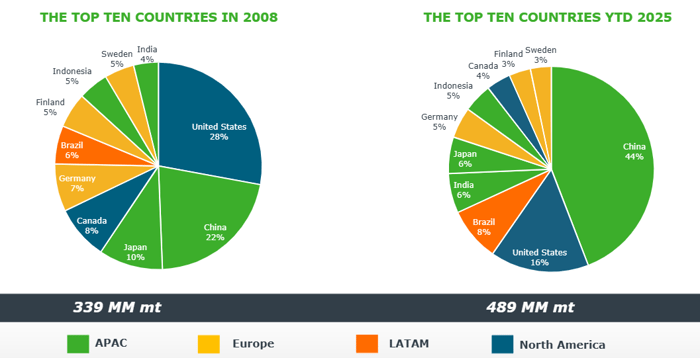

China's Rise Continues to Reshape Global Markets

Over the last two decades, state-supported investment has enabled China to become the world's largest pulp and paper producer. Today, China continues to add significant virgin pulp and paper capacity while expanding containerboard, cartonboard, tissue, and specialty paper production.

Source: FisherSolve

However, this growth has created a new challenge: structural overcapacity.

Chinese paper capacity is growing faster than domestic demand, forcing producers to seek export markets. Cartonboard exports have nearly tripled since 2021, acting as a pressure-release valve for excess production.

This dynamic is increasingly influencing global pricing, trade flows, and competitive positioning, particularly in Europe.

So, what does this mean for global producers?

- Global competition intensifies

- Price pressure increases across commodity grades

- European producers face greater import exposure

- Regional supply-demand balances become less relevant than global capacity balances

In many markets, the challenge is no longer generating demand. It is managing excess supply.

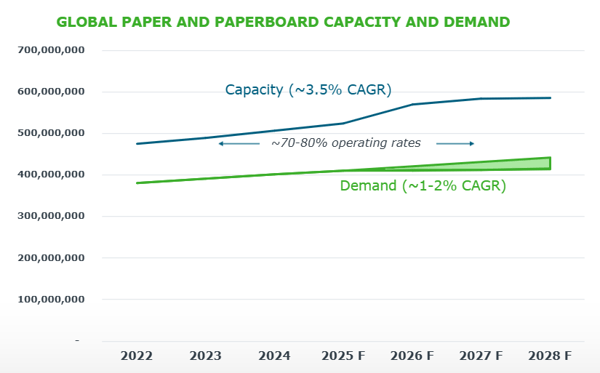

Packaging Demand Is Growing—Just Not Fast Enough

The long-term outlook for paper-based packaging remains positive, driven by several strong trends: rising e-commerce, efforts to replace plastics, sustainability commitments from leading brands, regulation favoring recyclable materials, and consumer preference for renewable options.

Growth is expected in areas such as corrugated transport packaging, folding cartons, paper bags, e-commerce mailers, molded-fiber protective packaging, and dry-food packaging solutions.

However, a key issue persists – global demand for packaging increases by about 1–2% annually, while capacity grows at roughly 3.5% each year. This creates a supply-demand imbalance that may continue into the next decade. The industry's challenge is shifting from simply producing more packaging to delivering more value.

Source: FisherSolve

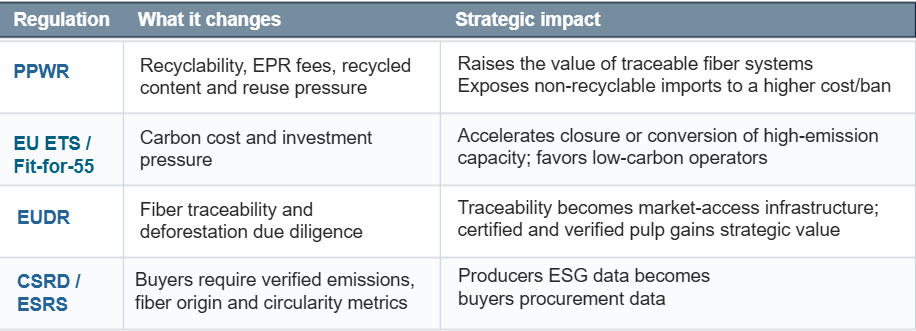

Regulation Is Becoming a Cost Curve

Perhaps the most significant theme emerging from the conference was the growing influence of regulation. Historically, mill competitiveness was determined primarily by fiber, energy, and labor costs.

Today, a fourth factor is becoming equally important – compliance costs. European regulations are fundamentally reshaping market conditions.

These regulations increase the value of traceable fiber supply chains, verified sustainability credentials, circular operating models, and low-carbon production assets.

In other words, compliance is no longer a reporting exercise. It is becoming a source of competitive advantage.

Traceability Is Becoming Market Access

One of the clearest examples of this shift is EUDR compliance.

The regulation requires companies to demonstrate that fiber inputs are not linked to deforestation and can be traced back to verified origins.

This creates a new reality: Traceability is becoming infrastructure.

Companies unable to provide verified fiber sourcing may face increasing barriers to market access, while those with transparent supply chains gain strategic advantages.

Technology platforms such as ResourceWise Forest Trackt® are emerging to help companies manage increasingly complex traceability requirements across global supply chains.

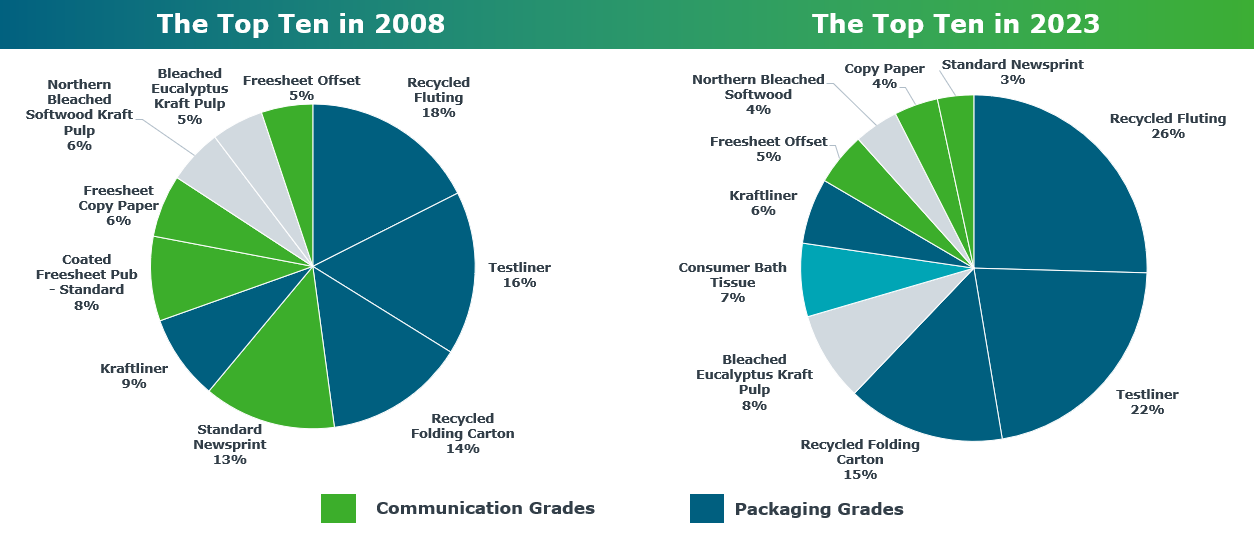

Molded Fiber Is Emerging as a Major Growth Category

One area showing particularly strong momentum is molded fiber.

Traditionally used in protective packaging applications, molded fiber is increasingly replacing expanded polystyrene and certain plastic formats in:

- Food packaging

- Consumer goods

- Industrial components

- Protective packaging systems

Global molded fiber production is projected to continue growing at approximately 6.5% annually through the end of the decade.

As brands seek sustainable alternatives and regulators push for recyclable packaging, molded fiber is positioned to become one of the most important innovation segments within the packaging industry.

Why Closed-Loop Fiber Systems Matter

Perhaps the most important strategic insight from the presentation was the industry's transition from a volume mindset to a systems mindset.

Historically, companies focused on tons produced, capacity utilization, and commodity pricing.

However, future leaders will focus on:

- EBITDA per packaging unit

- Closed-loop fiber systems

- Customer integration

- Regulatory readiness

- Fiber traceability

- Circular supply chains

The concept is simple:

Make a box → recover the fiber → make another box.

Closed-loop models reduce fiber cost volatility, improve sustainability performance, strengthen regulatory compliance, and create stronger customer relationships.

Companies such as Saica and Prinzhorn were highlighted as examples of organizations building competitive advantage through integrated fiber systems rather than simply expanding production capacity.

The New Competitive Formula

The future of fiber-based packaging remains promising. Demand growth, sustainability pressures, and regulatory support will continue creating opportunities for paper-based solutions.

But growth alone will not solve the industry’s challenges.

Global capacity expansion is outpacing demand growth. Regulation is becoming a structural cost factor. Traceability is becoming market access. And overcapacity—particularly in China—will continue influencing global markets.

The companies that thrive in this environment will not simply manufacture more paper. They will design, control, and optimize the flow of fiber itself.

To do that well, companies need a clearer view of the forces shaping their markets—from mill-level cost positions and capacity changes to recycled fiber pricing, carbon exposure, trade flows, and regulatory risk.

With deep data, market intelligence, and strategic consulting across the pulp and paper value chain, ResourceWise helps companies understand these shifts and make more confident decisions in an increasingly complex packaging market.

What the UCO Market Reveals About Crude Tall Oil Demand

What's Next for Asia's Largest Wood Pellet Supplier?

Fiber Forward: Sustainability Highlights from the Paper Packaging Industry

Sustainable packaging continues to present a significant opportunity for pulp and paper professionals as brands, regulators, and consumers push for...

Navigating the Future of the Pulp, Paper, and Packaging Industry

As the global landscape evolves, the pulp, paper, and packaging industry stands at a pivotal crossroads. Rapid advancements in technology, changing...

Pulp, Paper, and Packaging Conferences You Should Look Out for in 2024

As we enter a new year, there is an exciting lineup of conferences waiting to be explored. Conferences provide the perfect opportunity to join forces...