3 min read

Finland’s forest products industry stands at a pivotal moment. Global market shifts, tightening EU regulations, and domestic restructuring are driving companies to reassess operations, optimize capacity, and innovate for long-term competitiveness.

While near-term challenges persist, such as soft demand in pulp and paper as well as cost pressures in sawmilling, the sector continues to demonstrate strategic adaptability and strong fundamentals.

Strategic Adjustments Across the Value Chain

Leading producers are reshaping their portfolios in response to the structural decline in graphic paper and weak global demand.

UPM plans to close its Kaukas paper mill in Lappeenranta by the end of 2025, affecting 220 employees and reducing coated magazine paper capacity by 300,000 tons. The move aligns with the company’s focus on cost efficiency and high-value segments. UPM has also started a strategic assessment of its plywood industries. The company recently sold its Korkeakoski sawmill to Versowood Oy.

Similarly, Sappi Europe has begun consultations to potentially close one paper machine at its Kirkniemi mill in Lohja, a step aimed at strengthening operational sustainability and long-term competitiveness.

Metsä Board is closing its Tako cartonboard mill in Tampere. Metsä Group is to initiate statutory negotiations concerning all of its business areas and Group operations. According to preliminary assessments, the planned measures may lead to a permanent reduction of 800 permanent jobs if implemented and € 300 million annual savings.

Meanwhile, Stora Enso reported improved Q2 results, supported by stronger wood-product demand and the integration of its Junnikkala sawmill. The company continues to streamline operations and invest in growth areas such as packaging materials and construction solutions. The company is also planning a sawmill investment in the vicinity of its facilities in Imatra.

Sawn Timber: Growth Meets Margin Pressure

Finland’s sawmill industry has expanded output despite a difficult cost environment.

Sawn-timber production rose roughly 15 % year-on-year in early 2025, with exports up more than 20 % to over 70 countries. Growth was particularly strong in Egypt, Estonia, and the UK.

However, profitability remains squeezed: log prices have surged nearly 80 % over the past decade and a half, while lumber prices rose less than 40 %. Weak pulp and residue markets, along with soft global construction demand, continue to challenge margins.

Investments in modern, automated facilities—such as Pfeifer Group’s new Kajaani mill— (also Koskisen Oy, Kuhmo Oy, Versowood Oy, Isojoen Saha Oy etc.) illustrate the sector’s long-term commitment to efficiency and sustainability despite short-term volatility.

Policy and Regulation: Navigating Complexity

The EU’s regulatory agenda continues to shape the operating landscape.

The EU Deforestation Regulation (EUDR) has been delayed by one year due to IT-system readiness issues, giving companies more time to prepare compliance systems. While the European Commission insists that the regulation’s objectives remain unchanged, many stakeholders see the postponement as a critical window to simplify overly complex reporting requirements.

At the same time, the EU Forest Monitoring Regulation was rejected in committee after opposition from Finnish forest owners concerned about data control and administrative burden.

Finland and Sweden have also jointly urged the Commission to make the LULUCF Regulation more realistic, warning that current carbon-sink targets risk constraining sustainable harvests and undermining the forest industry’s role in the green transition. Also Central European countries are questioning LULUCF.

Economic Policy and Competitiveness

The Finnish government’s 2025 budget session reaffirmed fiscal discipline but highlighted the need to safeguard industrial competitiveness and forest-growth investments.

The phase-out of electrification support for energy-intensive industries has raised concerns about Finland’s cost position relative to other EU countries that maintain such incentives.

Ensuring a reliable raw-material base, strengthening carbon-sink accounting, and supporting young-forest management remain critical to both economic and climate goals.

Outlook: Opportunities Through Transition

The Finnish forest products industry faces a demanding short-term environment—marked by subdued pulp markets, oversupplied packaging, and cost inflation—but continues to advance in areas that support sustainable growth.

Nature-credit markets, bio-based materials, and improved carbon-sink accounting represent emerging opportunities.

A modest recovery in the European construction sector is expected to begin in 2026, aided by EU-funded infrastructure and easing financing conditions.

Finland’s industry enters this next phase with its traditional strengths intact: resource efficiency, world-class forest management, and a deep commitment to sustainability. However, it can be expected that consumption of roundwood will decrease somewhat from the record years. Domestic harvestings increased maybe too much after imports of Russian wood ended, the energy sector increased consumption and, the forest industries enjoyed tailwind from the markets.

Stay informed on the evolving trends, key regulatory developments, and market movements shaping the global forest products sector—subscribe to our newsletter for expert analysis, actionable insights, and timely updates tailored to support strategic decision-making in today’s dynamic industry landscape.

The Pulp Mill as a Biorefinery: Unlocking New Revenue Streams

Bio-Bunker Premiums Rebound as Oil Market Disruption Eases

Keeping Pace with the Forest Products Market: A Close Look at Finland's Forestry Update

The forest products market worldwide is anything but stagnant. With various factors such as weather conditions, policy changes, and global demand...

Finland’s Forestry Industry in 2026: Powering a Bioeconomy Under Pressure

Finland’s economy has long been rooted in its forests—but in 2026, the sector sits at the intersection of energy transition, environmental...

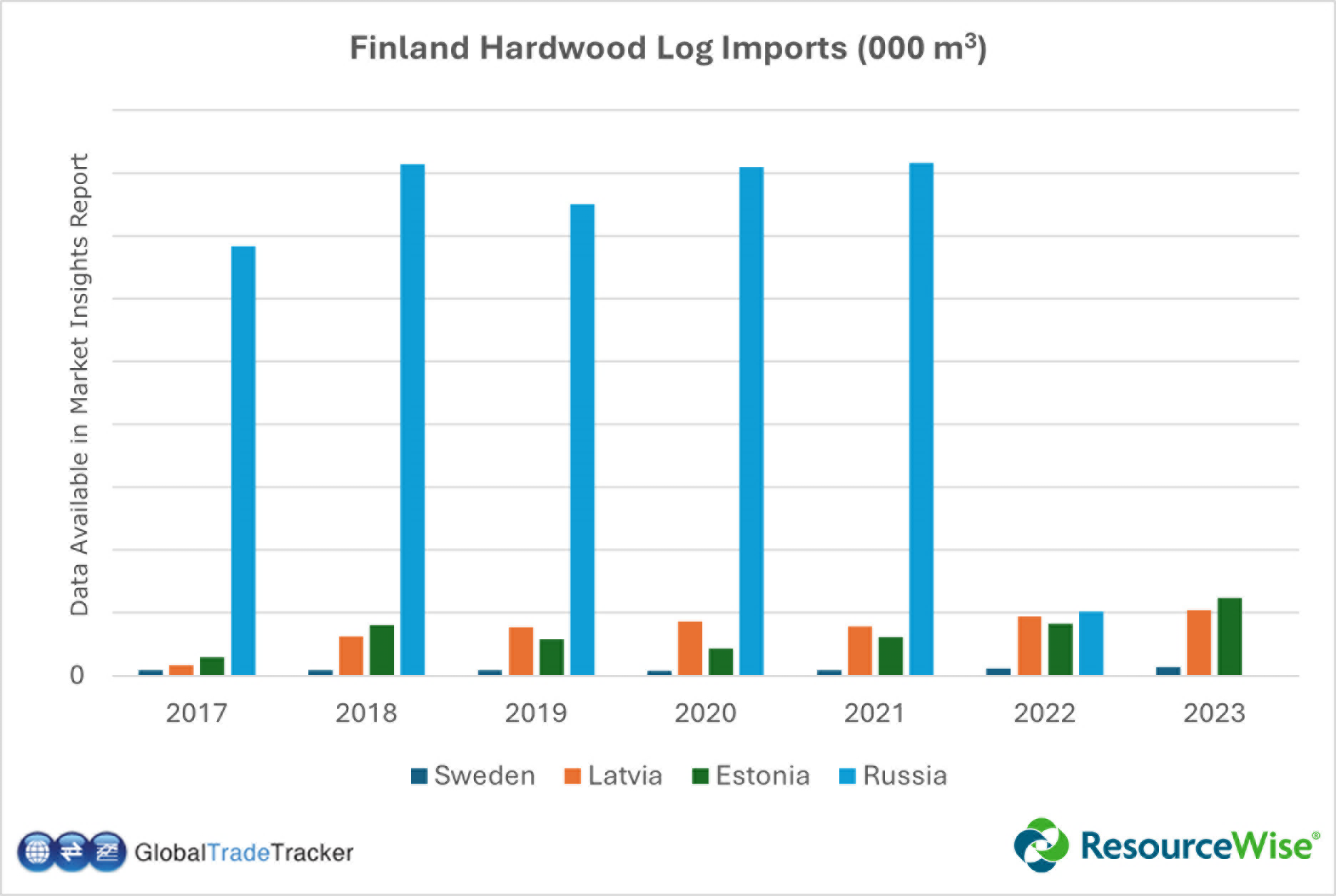

An Overview of Finland's Hardwood Log Imports

Recent geopolitical events have impacted a range of industries, including Finland's hardwood log import market. Recent shifts in the international...