As Q1 2015 came to a close, Europe’s near-term commitment to utilizing low-carbon energy solutions continues to reflect a growing global awareness of pioneering energy alternatives. International interest in wood pellets — an increasingly popular and sustainable biomass feedstock— remains high, particularly by Western European utilities. In fact, wood pellet demand continues to rise year-over-year and growth in the sector has led to a number of recent pellet mill expansions in the Southeastern US, which is an ideal region to manufacture this product due to its thriving forestry and timber industry. In recent years, US-based pellet producers have fulfilled the increased demand abroad and with continued growth in the sector— as well as continued EU subsidies for renewable energy—there are real opportunities for American producers.

What’s driving demand abroad?

An international interest in cost-effective, renewable energy and the ability to generate heat and power from low-carbon sources have been driving an increase in US wood pellet production. Globally, the 2014 demand for wood pellets exceeded 23 million metric tons. Due to a limited ability to supply its own biomass, Europe’s demand alone was over 19 million metric tons. With continued interest in the biomass model and investment from some of Europe’s leading utility providers, consider the recent news out of the region:

low-carbon sources have been driving an increase in US wood pellet production. Globally, the 2014 demand for wood pellets exceeded 23 million metric tons. Due to a limited ability to supply its own biomass, Europe’s demand alone was over 19 million metric tons. With continued interest in the biomass model and investment from some of Europe’s leading utility providers, consider the recent news out of the region:

-

Drax Power Limited, supplier of 8% of the UK’s electricity and operator of England’s largest power station located in North Yorkshire, continues to devote substantial resources towards biomass technology. Drax is investing in its future by replacing coal-burning units with low-carbon, wood-burning units. Two of the six units at its North Yorkshire flagship complex have been converted to burn biomass, and the company has plans to add a third unit in late 2015/early 2016.

-

Drax is also actively engaged in maintaining a sustainable source of supply for wood pellets, and the company operates manufacturing facilities located in the Southeastern US.

-

DONG Energy, Denmark’s largest energy provider has converted the final coal-fired unit at its Avedøre Power Station to burn wood pellets— a move that will provide low-carbon energy for over 215,000 residents in the Copenhagen area. Additionally, DONG’s largest power station will generate clean energy solely from biomass by the fall of 2016.

Europe’s 2014 demand for 81 percent of the global wood pellet supply is so exceptional that one might be tempted to categorize it as a momentary trend. But consider the power station conversions mentioned above as well as the rise in thermal generation and this growth suggests a transition towards permanent and sustainable low-carbon sources of energy. As governments continue to demand adherence to sets of laws designed to curtail environmental impact (Renewable Fuel Standard; Biomass Sustainability Guidelines), the public is becoming increasingly aware of—and eager for— energy alternatives. The Economist Intelligence Unit predicts a renewable energy increase of 13% in 2015 as cleaner sources of power become more popular.

In the case of the European Union (EU), substantial subsidies exist for the creation of renewable energy via the European Commission’s Renewable Energy Directive, which “establishes an overall policy for the production and promotion of energy from renewable sources in the EU. It requires the EU to fulfil at least 20% of its total energy needs with renewables by 2020 – to be achieved through the attainment of individual national targets.”

A Steady Supply of Southeastern Biomass

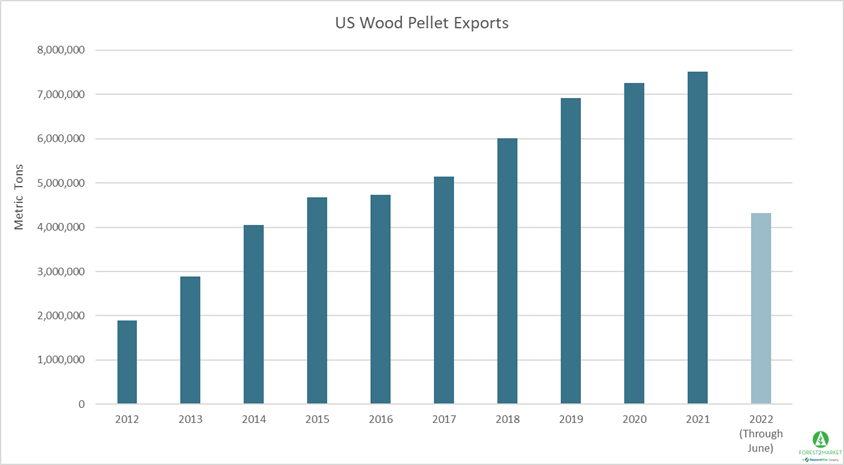

As mentioned above, the Southeast is a natural hub for the production of wood pellets. Biomass is plentiful, and the dense canopies that provide (relatively) fast growing cycles make it an ideal region in which to plant and harvest timber. And with convenient regional access to major shipping ports, it’s no wonder the Southeast is home to over 80 individual pellet mills. Note the graph below, which illustrates the regional pellet production growth over the last seven years as well as the projected explosion in growth over the next five years.

In Q1 2015, new facility construction announcements and forecasts have confirmed the surge in Europe’s commitment to wood pellet energy production going forward:

-

Enviva Partners, LP, a market leader in wood pellet production with large-scale operations throughout the Southeast, announced plans to open two new manufacturing facilities in North Carolina’s Sampson and Richmond counties. Both sites will have annual production capacities of over 500,000 tons. The combined $214 million projects are scheduled to be completed in 2016, and will bring the company’s individual NC facility count to four. Enviva also operates pellet manufacturing facilities in Virginia, Alabama, Mississippi and Florida, as well as port operations in Virginia and Alabama.

-

Zilkha Biomass finalized the purchase of a land parcel in Monticello, Arkansas that will become the site of its newest wood pellet mill in late 2015. The company is making a $90 million investment in the facility that will produce roughly 450,000 tons of its proprietary Zilkha Black® wood pellets once it becomes operational in 2016.

-

Cornerstone Biomass Corp., a joint venture between PHI Group Inc. and AG Materials LLC, announced plans to construct a new pellet mill in Suwanee County, Florida. The facility is expected to be operational in early 2016 and will produce an estimated 200,000 tons of wood pellets per year.

-

Portucel Sporcel Group, a Portugal-based forest, paper and energy corporation, has announced plans to construct a $110 million wood pellet production facility in Greenwood County, South Carolina. Slated to open in late 2016, the plant will be Portucel’s first pellet mill in the US and will have an annual production capacity of roughly 400,000 tons.

Near-Term Projections and Market Outlook

Though impressive, these developments do not tell the whole story of the larger wood pellet sector. As with any emergent industry serving a complex, global market, there will be challenges both home and abroad to overcome in the near and long terms. As Seth Ginther, Executive Director of the U.S. Industrial Pellet Association recently noted, US pellet producers dealt with a substantial surplus of product during Q1. He added, “Additionally, there are some regulatory constraints, such as a recent doubling of value-added tax on pellet imports in Italy that has increased the price of pellets by 30-35 euros per tonne.”

It is also worth noting that the EU’s renewable energy directive was conceived prior to the 2008 financial crisis and, while commendable, reflects the optimism of a 1990’s economic climate. With tangible budgetary constraints and concerns over the last seven years—as well as disparate expectations and capabilities by EU member—one must question whether the 20% goal is attainable and if subsidy qualifications will be restructured within the next five years.

While the larger EU directive for renewable energy goals is based on the 2020 target date, the UK government, for its part, has stated that it will end biomass subsidies in 2027. How will this move affect the market for wood pellets and the demand for American timber resources going forward? There is no energy market crystal ball—especially when government subsidies are involved— but consider the investments being made on both sides of the pond:

-

Utility providers such as Drax and DONG continue to make substantial infrastructural investment to burn biomass for heat and such a commitment is unlikely to be abandoned or reversed in 2027, especially as the projected US South wood pellet production (and European demand) continues to rapidly rise.

-

The US has already established an effective supply chain to deliver wood pellets to Western Europe, which offers streamlined advantages for parties on both continents. As investment in US timberlands, wood pellet mills, and process improvements continues to develop, there would be no reason to suspend a stable source of supply.

As Q2 ushers in the continued construction of new wood pellet facilities throughout the Southeast, there is reason for regional producers to remain optimistic. Again, consider the projected growth detailed in the above graph and the ongoing investment being made abroad. Through the combined efforts of organizations in both the US and Europe, these symbiotic relationships are meeting current clean-energy requirements while laying the groundwork for a cleaner—and greener—future. This is the objective, after all, that will remain top of mind for individuals and legislators for decades to come.

EU General Court Tosses Anti-Biomass Case

In a win for wood biomass and the continued growth of renewable energy across Europe, the European General Court recently dismissed a case brought by...

Wood Pellets Can Help Alleviate Energy Pressures Amid War, Uncertainty

As the Wall Street Journal recently reported, the ongoing war in Ukraine has pinched trade flows of the increasingly valuable supply of industrial...

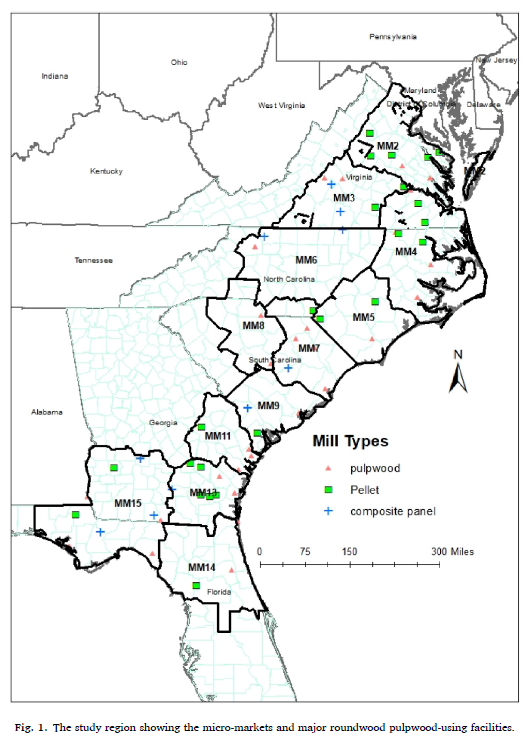

Quantifying the Impacts of Wood Pellets on Pulpwood Stumpage Markets in the US South

This is an abbreviated version of Dr. Rajan Parajuli’s article published in Volume 317 of the Journal of Cleaner Production on October 1, 2021. The...