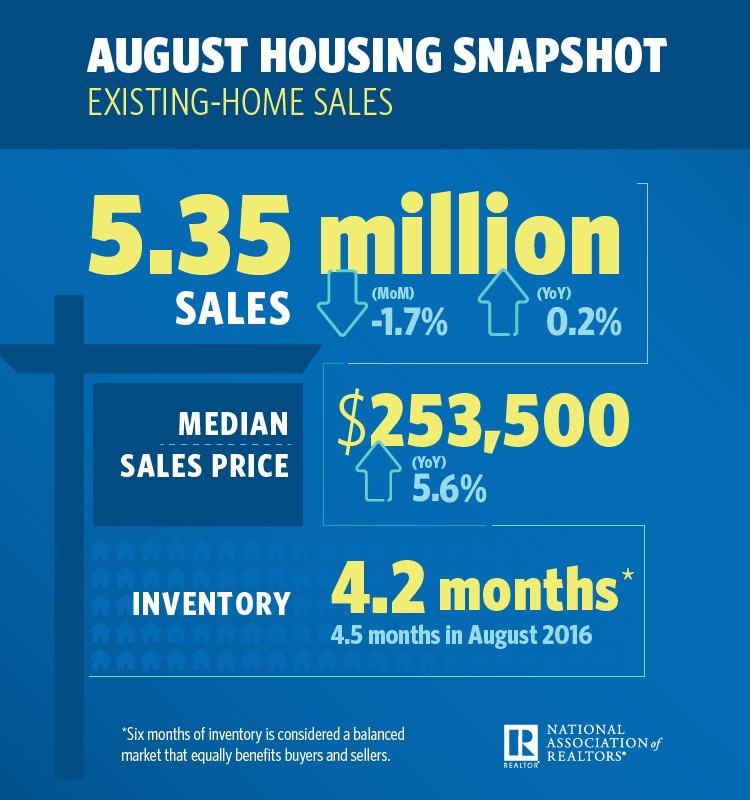

It’s no secret that housing starts have disappointed thus far in 2017 and while an end-of-year bump may be yet to come, it could be too little too late. Existing home sales have also been sluggish: sales slipped 1.7 percent in August to a seasonally adjusted annual rate (SAAR) of 5.35 million. This was the fourth decline in five months for this segment of the market, bringing the annual rate to its lowest level in 12 months. (Existing-home sales account for roughly 90 percent of the total market, while new-home sales make up roughly 10 percent.)

It is also worth noting that housing data may be volatile for several months in the wake of Hurricanes Harvey and Irma and as a result, home sales in 2017 will probably be weaker than they were last year. However, a temporary pause in both sales and construction in Texas and Florida will likely give way to improving demand in 4Q2017 and into 2018.

The US housing market has improved slowly and steadily since bottoming in the wake of the 2008 Great Recession, but it is now showing signs of weakening. What’s going on with one of America’s most reliable market segments? More specifically, what forces are combining to affect the market at the same time?

Reformed Buying Habits

Analysts continue to look for real-life explanations for why the housing market is behaving in such volatile fashion despite apparent evidence of pent-up demand. “The primary reason [for the lack of activity] seems to be widespread consumer caution,” wrote Jeffrey Snider, head of global investment at Alhambra Investments. “American homeowners do not appear willing to put up their homes for sale despite rising prices. It is practically the antithesis of the housing mania period from just over a decade ago. That may be in part due to a paradigm shift in expectations and behavior (a lot of people learned something from the bust).”

Household formation is also beginning much later in life for Millennials, many of whom witnessed their parents get blindsided in 2008. This trend is not necessarily something Millennials favor as a group; the data suggest that they are eager to pursue homeownership. However, the effective unemployment rate for this generation is roughly 14 percent and even for those fortunate enough to have found jobs, they are usually low-paying. Millennials are graduating from college with an average student loan debt of $33,000 and more of them have debt exceeding $40,000 than at any other time in US history. The result is a generation that is forced to delay some of life’s major milestones including marriage, parenthood, and home buying. Consider the statistics:

- Almost 50 percent of Millennials have less than $5,000 in savings

- In 2010, almost 30 percent of those aged 18-34 were living with their parents

- The median marriage age in 2010 was 30 compared to 23 in the 1970s

- In 2012, 23 percent of those aged 18-31 were married and living in their own household compared to 56 percent in 1968

Household formations have been decelerating on trend since mid-2016. One can debate whether this is a symptom of or contributor to the housing slowdown, but “it is complementary data that suggests growing reluctance on the part of consumers to take a major risk with a major life change,” Snider continued. “That’s not indicative of a healthy economy, or even the right marginal direction towards one.”

Inventory

Even before the storms made landfall, home price growth was exceeding wage gains due to lean inventory, which hurt affordability for some and left others with fewer properties to choose from. Starter and trade-up homebuyers need to spend 3 percent and 2 percent, respectively, more of their income to buy a home now than they did in 2016. Ironically, a steady job market and low borrowing costs are keeping the housing recovery alive… but for how much longer?

“The American housing market is stuck in its own kind of stagflation: Existing home sales have been flat since last fall, while home values are up more than 4% over the same period,” said Zillow Senior Economist Aaron Terrazas. “For more than two years now, inventory has been has been contracting, pushing the housing market into an inventory crisis.”

At least part of the reason for contracting existing-home inventory is that not enough affordable new homes are being built to meet demand. Only about 14 percent of new homes sold so far this year were priced at or below $200,000 compared to a January 2002-to-June 2009 average of roughly 43 percent.

“The economics of building, with fixed costs associated with permitting and environmental requirements rising steeply, favored the high end of the market for much of this expansion (it is easier to get those fixed costs back on a $500,000 home than a $300,000 home),” noted Stephen Stanley, chief economist for Amherst Pierpont Securities. “Anecdotal reports point to a widening chasm between the entry-level market, which is red-hot with inadequate supply, and the luxury market, where there are huge gluts of overpriced homes in many areas. Builders will have to figure out how to make money building starter homes to balance that equation,” Stanley added.

Home buyers could face an additional hurdle of higher mortgage interest rates if/when the Fed begins to shrink its balance sheet. The Federal Reserve was one of the biggest buyers of mortgage-backed securities (MBS) during and after the housing crash of 2008. As the Fed begins to unwind those purchases, new buyers will have to step up to the plate.

Other Considerations

Of the roughly 1 million mortgaged homes in Harvey’s disaster area, Black Knight Financial Services, a data and analytics services provider to the mortgage and real estate industries, estimates more than 75,000 will become delinquent within two months, and 45,000 are at risk of becoming seriously delinquent or even face foreclosure inside a four-month period. “It is clear investors are banking on the rebuilding effort becoming its own macroeconomic engine of growth,” wrote Danielle DiMartino Booth. However, “with housing clearly peaking, the nearer-term risk is that Harvey’s devastation solidifies broader market woes.”

Though the extent of damage from Hurricane Irma is yet to be determined, estimates are that 25 percent of homes in the Florida Keys were totally destroyed. It is clear that the rebuilding efforts will require massive amounts of lumber and other wood products but as we noted earlier in the month, much of this will involve a temporary reallocation of resources and labor away from the existing housing market.

The good news is that the housing market is still poised for modest growth, and homebuilding will begin again after the rebuilding from these two storms. If history is to be a guide, stumpage prices may drop in the near term and rebound within a few quarters. SYP lumber prices have begun rising sharply in the wake of Harvey after exhibiting a slow decline since April. Demand for wood fiber and lumber seems healthy as we head into 4Q2017 and the new year, despite a wavering housing market.

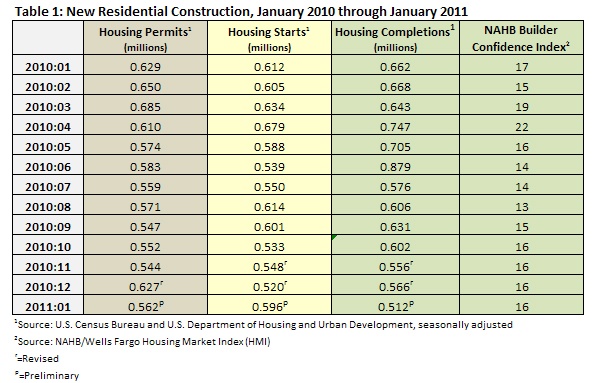

Housing Update - March 2011

Once again, signals from the housing market were mixed in January. As Lawrence Yun, the chief economist at the National Association of Realtors...

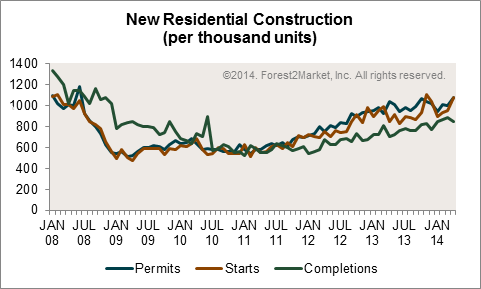

Housing Market Trends: 2008 to Present

Nearly seven years after the housing market experienced its largest downturn since the Great Depression, and five years into the recovery from the...

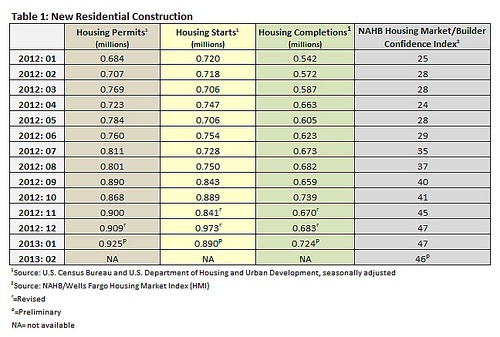

Housing Market Update - January 2013

Even though the economy grew at its slowest pace since 2011 in the fourth quarter of 2012, the housing market over-performed in comparison. David...