Pete Coutu

Pete Coutu

Wood fiber prices have trended downward in the Great Lakes region over the last two years despite an economy that is sustaining growth—slight as it may be. What is affecting this price drop and are there any indications that it may reverse course anytime soon?

The Great Lakes region has some unique characteristics when compared to other timber-producing regions across the US. The area boasts an abundance of high-quality wood raw materials and has a long history in pulp and paper production, but a series of mergers, acquisitions and facility closures in recent years has changed the regional industry.

Unlike the US South, the seasonality of timber harvesting is a significant driver of price in the Great Lakes region. While there is oftentimes discussion about “limited logging capacity” due to this seasonality, proper planning will usually mitigate the risks associated with any unforeseen impact on supply. While all species groups are affected by seasonal fluctuations in weather, hardwood production seems to be a main driver of the industry in the Great Lakes.

Due to these seasonal weather extremes, hardwood inventory management is key to market pricing for all fiber. Hardwood inventories grow significantly in the winter to include as much as 80 days’ worth of system-wide inventory to last through the spring months. It is equally important for the system to maintain a minimum of 30 days’ worth of hardwood inventory during the rest of the year so that winter surge capacity is not stressed beyond its capabilities.

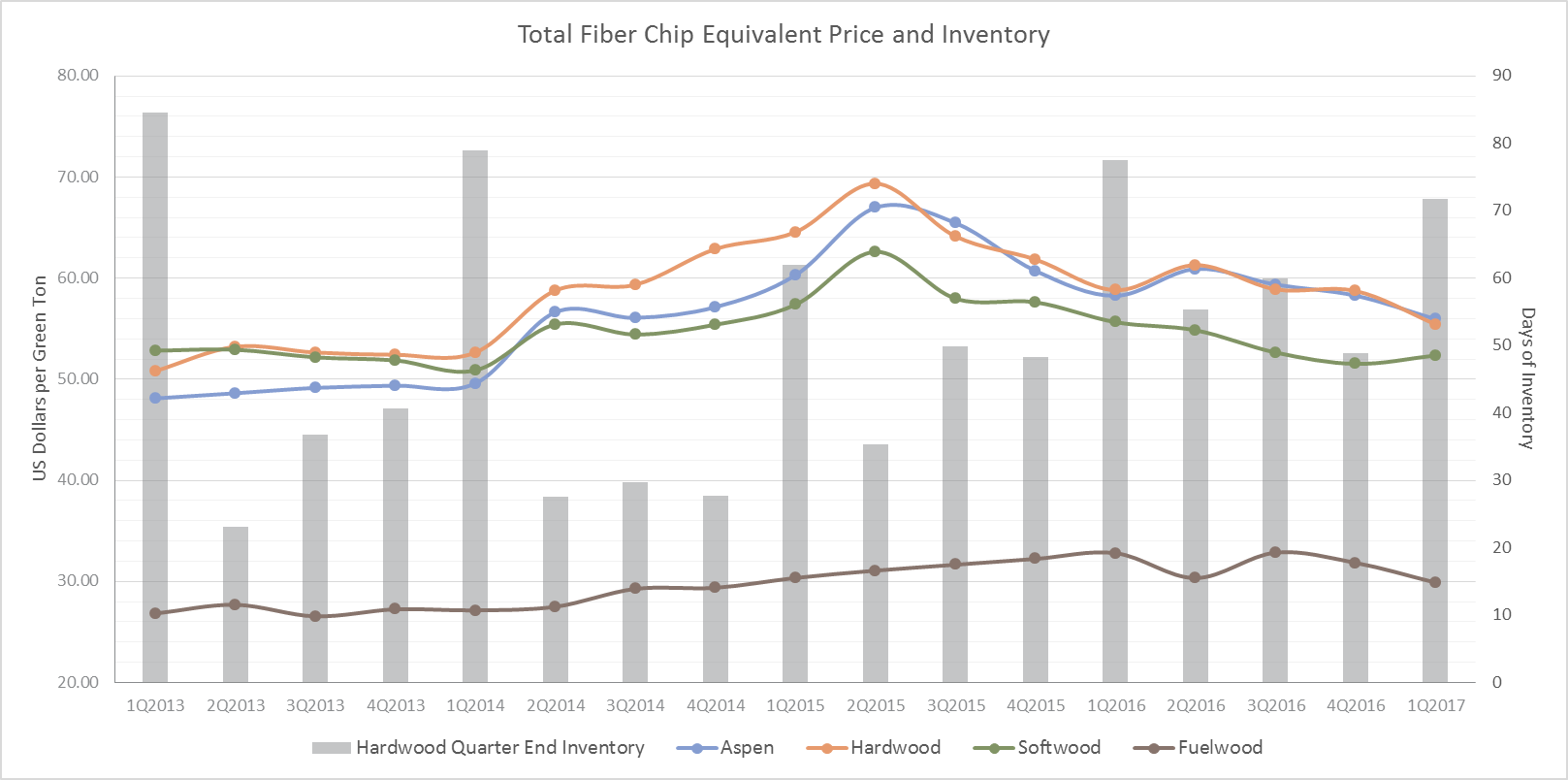

Notice in the chart below that price for each of the three species groups (hardwood, softwood, and aspen) follow the same trend of increase and decrease. But an interesting dynamic emerged in the last few years, which illustrates the importance of hardwood inventory management in a seasonal market. The chart below confirms the seasonality of inventory building in the Great Lakes; notice the Q1 end-of-quarter inventories by year since 2013 and you will see 70-80+ days of inventory in 2013, 2014, 2016 and 2017. Also notice the Q2-Q4 inventories in 2013, 2015 and 2016.

Now, look at Q2-Q4 hardwood inventories in 2014 and notice the price correlation; inventories remained markedly lower in this period—averaging less than 30 days—while prices increased steadily. But when it came time to begin building the standard large hardwood inventories in winter, the sudden surge in demand caused prices to spike and inventories to suffer; regional mills averaged just 60 days’ worth of hardwood inventory in 1Q2015—25 percent below the ideal 80 days—that came at a much higher price.

Prices peaked in 2Q2015 due to lagged effects from Q1 demand, and all products tracked downward similarly through the remainder of 2015 (with the exception of wood fuel). Notice the robust hardwood inventories that have been held over the last eight quarters and you will also notice the corresponding decrease in price, which suggests that the market is adjusting and getting back to a stable, less volatile level.

However, seasonality has a huge impact on prices in the Great Lakes. Should the region experience an unusually wet summer that might impede harvest activity, prices could begin climbing again. Regional rainfall for June was more than double the average in some areas. 1Q2018 inventory building will begin in just three months, so any hitch in supply in the near term could have lasting effects on price well into 2018.

Chip & Pulpwood Price Trends in the US South & PNW

Over the past six years, chip and pulpwood prices in the Pacific Northwest (PNW) have demonstrated significant levels of volatility when compared to...

Timber Prices & Inventories in the Lake States Continue to Fall

As we reported in late 1Q2021, delivered wood fiber prices in the Lake States hit their lowest point since Forest2Market began collecting...

PNW Log Costs Remain Near Record Highs

Delivered log prices in the Pacific Northwest (PNW) have maintained near record highs through winter, and the sustained high price run since 4Q2017...