Week: 2/13/2014 through 2/19/2014

Relative softness in the market continued this week as the Upper Mid Atlantic and Northeast continued to thaw from the last two weeks of weather. News on the housing starts front and declining builder confidence numbers added to the weak sentiment. Average sales order and shipment volumes were down slightly but there was some spread between Commodity products and Specialties. 2x6, 2x10, and 2x12 dimensions took the majority of the hits in both East and West markets. 2x4 MSR trades reflected the weak housing start numbers.

Housing starts, completions and inventory are not only key indicators for our industry; they are also key overall economic indicators and deserve attention. While some geographic areas are picking up steam, we’ll need to see 1.5 million starts (annualized) nationwide before the market is deemed fully recovered.

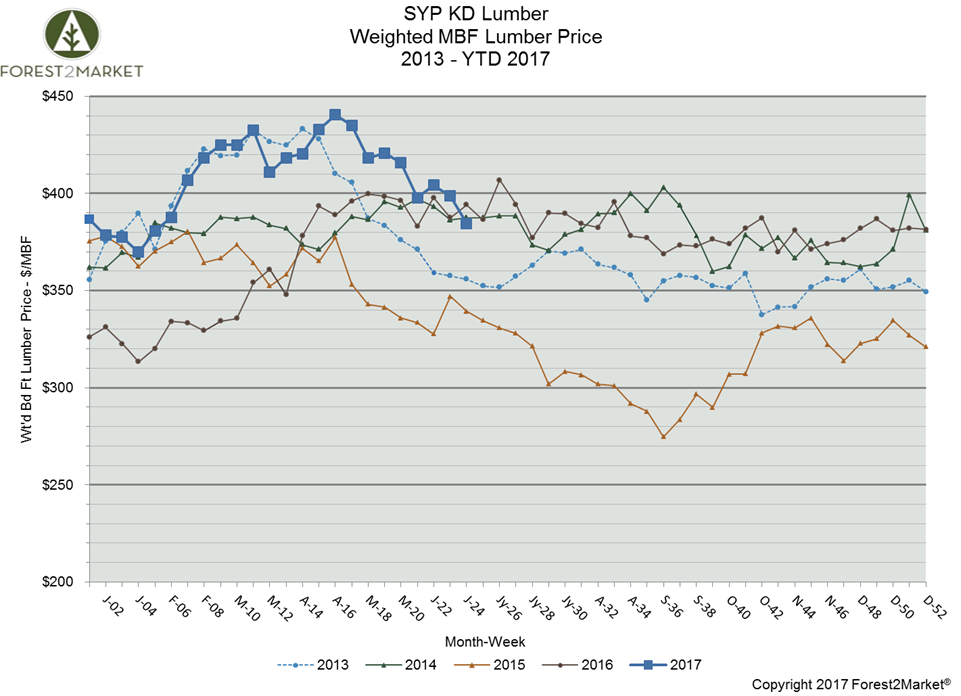

Lumber Prices Stabilize; Is More Volatility Around the Corner?

By mid-July, the price for finished southern yellow pine (SYP) lumber had tumbled over 65% from a new record high achieved just nine weeks prior....

Strong Demand for Lumber Driving Sawmill Expansions in the US South

Over the last few decades, the US South has become the most active region in the country for the forest products industry. While a number of factors...

The Coming Lumber Gap: Part II

In the final installment of this two-part series, we examine the cumulative effects of a number of dynamics likely impacting the current lumber...