3 min read

Beginning in 1Q2017, prices for domestic and export Douglas Fir and Hem-Fir logs in the Pacific Northwest (PNW) rose steadily before spiking to record levels in 2Q2018. As I wrote in 4Q2018, log and lumber prices in the PNW began to drop precipitously by September of last year as lumber market speculation subsequently waned. We’re now halfway through 2019 and, while prices have meandered up and down minimally since the beginning of the year, the overall decreasing trend is nevertheless stark.

Log Price Roller Coaster

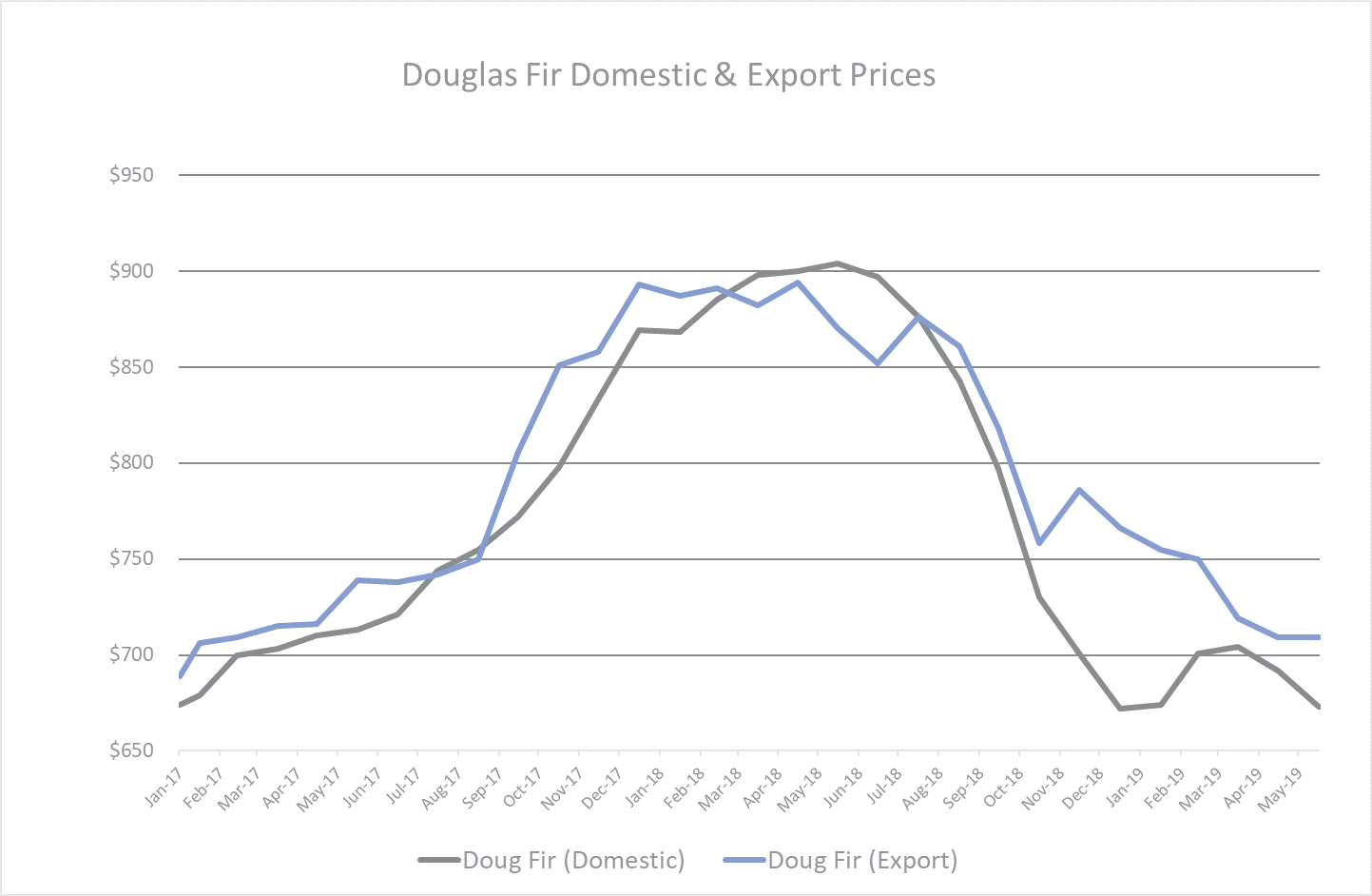

Just one year ago (June 2018), the weighted average price for delivered domestic Doug fir logs was $904/MBF, which was 27% higher than the year prior. However, the meteoric rise was short-lived as prices recently plunged to $673/MBF (-25%) in June 2019.

Export prices have followed a similar path to domestic prices over the last few years, however, notice the trend reversal in November 2018 in the chart below. In that month, export prices diverged significantly from the downward slide of domestic prices and jumped nearly $30/MBF, or roughly 4%. While export prices have trended down since then, they have remained above domestic prices and the current spread between the two is roughly 5%.

Douglas Fir Log Prices

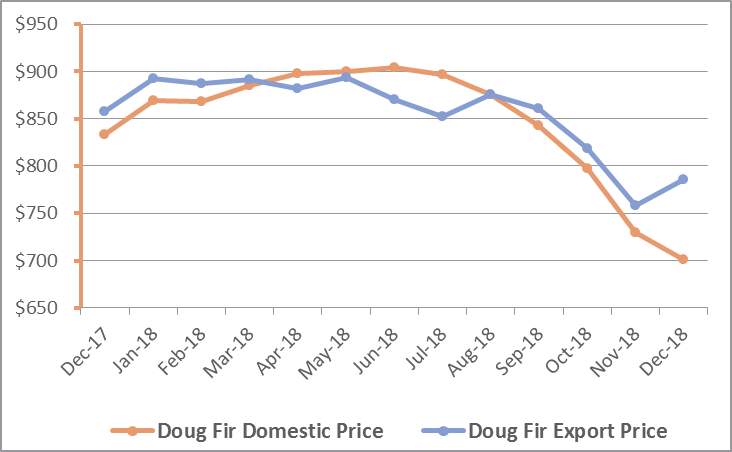

In June 2018, the weighted average price for delivered domestic Hem/Fir logs was $693/MBF, which was 21% higher than a year earlier. Like Doug fir prices, the meteoric rise was temporary, and prices crashed to $540/MBF (-22%) a year later in June 2019. Compared to Doug fir performance, export prices of Hem/Fir have tracked much closer to domestic prices since 2018. While export prices have also remained above domestic prices, the current spread between the two is roughly 1%.

Hem/Fir Log Prices

Near-Term Outlook

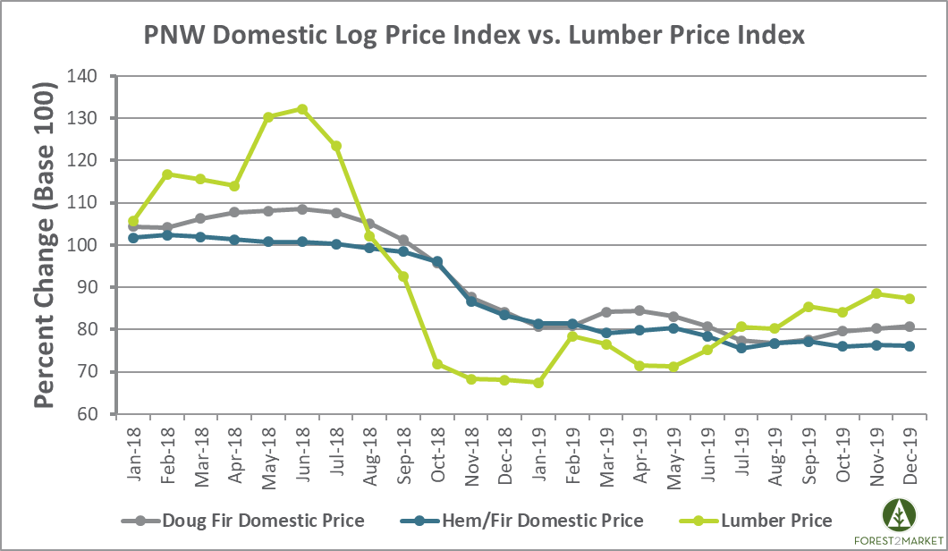

The combination of domestic and export competition for logs in the PNW drove prices to sustained highs for most of 2018, but a rebalancing of the market has largely taken place. There are a couple of dynamics to watch as we progress through the remainder of home-building season and into 2H2019.

- Domestic log price decreases are a delayed reaction to the extreme volatility of lumber market in 2018. Lumber prices have dropped significantly since posting record highs last year, which reflects a significant lack of demand in the current construction environment. As a result, a number of regional mills in the PNW, and many more in British Columbia, have either temporarily curtailed production or shuttered operations. This delayed reaction will continue to affect log prices in the near term.

- As Keta Kosman recently noted, the government of British Columbia (BC) has implemented a new policy that will increase the taxes collected on log exports from the coastal area of the province. Timber companies are required to prove that logs slated for export are “excess” to lumber manufacturing needs before the province will grant them export permits. While the policy is expected to discourage exports of higher-value timber, making more of the supply available to domestic mills that have a more difficult time competing, the restrictions on log exports from private lands could also mean that timber resources are undervalued, creating complications with key trading partners and adding unnecessary levels of complexity for the entire supply chain.

It’s too early to tell how this will affect timber supplies and producers on the US side of the border, but I expect there will be impacts. Coastal and southern BC pulp mills, which have been fiber short in recent years, may see some benefit in fiber availability from this and other policy changes, perhaps reducing their need to purchase fiber from the US PNW.

The continued decrease in domestic log prices is welcomed news for members of the PNW sawmilling industry that have maintained regular production through the slow homebuilding period of 1H2019. Despite multi-family housing starts tanking in June, single-family starts were up over 3 percent, and there is reason to believe the segment will maintain steady growth.

As Ian Shepherdson, chief economist for Pantheon Macro noted, “Single-family permits usually track new home sales but are lagging behind, either because homebuilders doubt the recent revival in sales will last - we think it will - and/or because they have too much inventory still after the disastrous drop in sales in Q4 last year. If we’re right, and new home sales rise in the second half of the year, new construction will follow.”

Constant analysis of current log prices paired with micro- and macro-economic market intelligence will be imperative to minimizing costs and maintaining profitability in this highly fluid and volatile market. Forest2Market offers transaction-based delivered price benchmarks and a suite of historical, data-based tools to help members of the PNW forest supply chain succeed in periods of uncertainty.

Pacific Northwest Log Markets: Domestic and Export Prices Diverge

Beginning in 4Q2017, prices for domestic and export Douglas fir logs in the Pacific Northwest (PNW) rose steadily before they spiked in 2Q2018 to...

Log & Lumber Parity: Are PNW Producers Back in the Game?

It’s been a crazy two years for the Pacific Northwest (PNW) log market. Beginning in 4Q2017, prices for domestic and export Douglas fir logs in the...

PNW Log & Lumber Prices: 1Q2020 Update

As Forest2Market data has confirmed over the last several years, log and lumber prices in the Pacific Northwest (PNW) can often result in a...