What do the following have in common?

- F16 fighter pilots and mechanics

- Lenders and buyers

- Minnesota taxpayers and drivers

Give up? The answer is this: the lives (personal, professional, or both) of these people are made safer and less expensive by the use of “predictive” mathematical models that forecast probable future outcomes of a variety of everyday events.

The United States Air Force uses mathematical models to predict part failures and establish replacement schedules. Based on historical failure rates, jet age, flight hours, and a multitude of other data, these forecast models determine the probability of part failures at a specific point in time. By predicting part failure rates with a high degree of accuracy, the Air Force increases pilot safety and saves both mechanics time and taxpayers money by replacing parts only when their failure is likely.

Financial institutions use mathematical models to calculate competitive interest rates while minimizing overall risk. These models evaluate hundreds of pieces of historical data about consumer behavior to determine a rate that is competitive enough to earn consumer business and high enough to minimize lender risk. The banking model forecasts the probability a customer will sign loan documents and pay back the loan. Insurance companies calculate insurance rates in a similar fashion.

Planning new highway construction is one of the more unique applications of data for forecasting purposes. The Minnesota State Department of Transportation uses a statistical model to predict the presence of undiscovered archaeological sites along planned highway routes. Using data associated with known sites, the model identifies locations along planned routes and assigns them a high to low probability of having undiscovered historical sites. By researching these sites in advance, the state avoids costly re-routing and work stoppages, all while complying with the National Historic Preservation Act. As a result Minnesota drivers get new roads at less expensive construction costs faster.

Even though their objectives are considerably different, the models used by decision makers in each of these cases have a lot in common.

They require a lot of data.

Developing mathematical models is an expensive undertaking. The cost of collecting, aggregating, and analyzing the amount of data required to develop and maintain a model is out of reach for most businesses.

They focus on achieving financial objectives.

Models are driven by financial objectives. Pilot safety is a top priority, but the Air Force cannot afford to replace every part in an F16 each time it flies. Instead, they use a model to maximize mission safety while extracting as much life as is possible out of each part.

If a bank’s only concern was risk, it would not lend money. However, zero risk means zero return, and this is not a sustainable revenue model. Banks use sophisticated models to maximize returns and maintain an acceptable degree of risk.

We have all heard the adage “practice makes perfect”, but in reality, it is perfect practice that makes perfect. Practice and perfect practice start the same; performing an act again and again until an objective is reached. Perfect practice is practice that introduces subtle changes over time, so the objective is still reached, but the act itself may change.

A classic example is Tiger Woods’ golf swing. While legendary, the drive that helped him win the Junior World Championship at the age of eight is not the same as the one that helped him win the US Open 22 years later. Conditions changed; he grew taller and gained muscle. To practice perfectly, he adjusted his golf swing to his changing conditions to achieve the same objective.

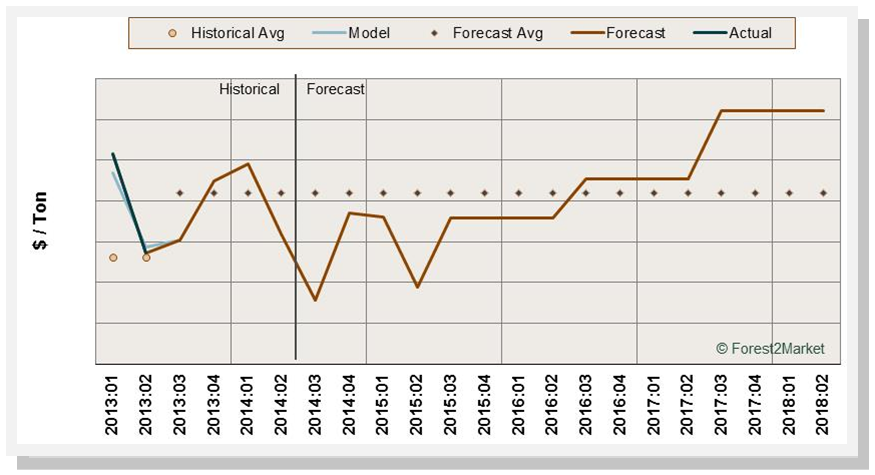

The creation of mathematical models is the same. As illustrated in the blog post A Lesson in Forecasting: Oil Prices, past performance along with the analysis of new data is an integral part of every quality model. Over time, the models get better at forecasting very specific outcomes with a high degree of accuracy, helping businesses improve their operational efficiency every day.

Using Models to Forecast

The modern business environment is one where events across the world can impact events at home:

- How much does the changing price of crude oil affect raw material cost?

- If China dumps its cache of US dollars, devaluing the dollar against the Euro in the process, does that mean anything to the future business environment?

- What affect will the Federal Reserve’s actions on interest rates have on business?

Readers of this blog are likely interested in how those events relate to wood procurement and how local markets are affected by factors like mill expansions or closures and price seasonality. How can we fit these global and local factors together to determine how and when prices will respond to changing factors?

The answer is to use a mathematical model that relates global factors to the local market, highlighting them according to how much an impact they had on past outcomes. Applying the discipline of mathematical modeling to the rapidly changing factors affecting prices is the only way to anticipate future timber prices. If you know with a high degree of confidence what you will pay for timber each month for the next 24 months, you can:

- Better optimize wood procurement – both volume and price

- Manage inventory (standing or in the yard) more effectively

- Align mill feedstock and output with raw material price trends

If you are in business, you forecast, even if you may not call it that. A forecast is simply a judgment about future events. If you think markets will slow down next month, you will make one set of decisions. If you believe markets will pick up next month, you will make a different set of decisions. The closer your judgment about the future to how things actually turn out, the better chance you have of making higher profits in the process.

Using a forecast model to maximize return and minimize risk is good business. Mathematical models are the power tools you need to gain strategic advantage, operate efficiently, and increase profits.

Suz-Anne Kinney

Suz-Anne Kinney