Structural changes in markets are often caused by profound changes to the economy. Over the course of the last 20 years, the US economy has undergone some stark adjustment periods that resulted in such structural changes. The “dot-com bubble” of 2002 resulted in a stock market downturn and loss of $5 trillion in market capitalization from its peak, and the Great Recession that began in 2007 is still a dire reminder for many of just how quickly things can change.

We are still in the early stages of a pandemic-fueled shutdown of the global economy, but there will also be some stark adjustments once we emerge on the other side of the COVID-19 challenge. The “new normal” is poised to decimate the automobile, airline, cruise line, and larger hospitality industries in the near term. And the complex supply chains that service these industries – the thousands of manufacturers, distribution networks, etc. – will also feel the pain.

While the major stock indices are designed to be forward-looking, they are (interestingly) largely ignoring the abysmal economic data. A recent piece from Bloomberg notes that “The S&P 500 is now up 26% from its March trough as slowing infection rates fuel hopes the global economy can begin to open up, while record monetary stimulus fuels a hunt for yield. The U.S. benchmark is now trading at 20 times the coming year’s forecast earnings, near the highest since 2002.”

This also feels like a moment that could accelerate the decline of already struggling sectors of the forest products industry: Printing and writing papers, as well as newsprint.

What is driving the accelerated pace of market adjustment?

On-Demand Information

Widespread access to the internet in the mid-1990s ushered in a new digital age—a profound shift in accessibility, information gathering and knowledge sharing that is still developing at an ever-quickening pace. Demand for printing and writing papers continues to decline rapidly as the digital age matures; over the last decade, production of printing and writing papers has been collapsing for some time.

As Fisher International’s Matt Elhardt wrote last month, “While the rates of change by country are different, since 2012, global capacity has been declining from -1 percent for uncoated freesheet (used in copy paper, envelopes, etc.) to -4 percent the coated groundwood grades (used in magazines, weekly circulars), to -6 percent for newsprint.”

Writing on the Wall

A recent piece via the Wharton School of Business portends a dynamic that is likely to accelerate in the future as the workplace evolves: “Enabled by advances in technology, remote work has been gaining traction in the last decade. Research released last year from International Workplace Group, a flexible workspace provider, found that 83% of businesses offer, or are planning to offer, remote work. The number of employees currently working from home under the social distancing guidelines demanded by the pandemic haven’t been counted officially. But anecdotally, it’s likely in the millions.”

And with school and university systems across the country now employing “distance learning” for the foreseeable future, tens of millions of K-12 and college students are doing their work online. All of this adds up to a situation where printing and writing papers are simply not needed to accomplish tasks and take tests.

Elhardt continues, “In the more bearish case, we assume not only a significant impact to printing and copying – due to work from home, quarantines, and institutional alternatives (like my kids now submitting homework online versus on paper worksheets), but also, that companies see some of those options are preferred, which results in permanent demand destruction before reverting to the longer term trend.”

The COVID-19 pandemic is indeed driving an accelerated demand destruction of this segment of the paper market – a market already in the early stages of structural decline.

Implications for Forest Markets

As a 2019 Forest2Market study demonstrated, the North American residuals market has been in a state of flux based on a combination of sufficient access to fiber and end product demand, which carries implications for many pulp and paper markets.

For example, demand for sawlogs in Western North America has remained strong in recent years but, dissimilar from the US South, timber supply is constrained. Unlike markets where the timber supply is expanding and prices can adjust downward as supply outpaces demand, the PNW timber supply is tightly matched to lumber and panel production requirements. This limits sawmill expansions and caps residual production to a finite volume and as a result, the PNW lost seven major pulp and paper operations in the wake of the Great Recession.

The PNW is not alone in bearing the brunt of this trend; southern hardwood markets have also been in a state of structural decline for years as consumer preferences ran countercurrent to products made by hardwood saw and pulp mills, and new market entrants are not choosing hardwood as the feedstock of preference. The regional hardwood lumber industry has not adapted to new market realities and adequate hardwood residual volumes are simply unavailable. Instead of fighting the inevitable decline, many hardwood pulp mill operators have switched to pine pulp or taken mills out of production.

Additionally, low cost pulp production in Brazil and Indonesia has stymied any new capital inputs in the US South hardwood market. At least three pulp mills have been converted away from hardwood production in the US South over the last several years.

In recent weeks, we have also seen announcements from major pulp and paper producers in the Northeast and Lake States regions detailing closures, curtailments and consolidations. Currently, there are simply no demand trends that indicate future growth for the hardwood pulp market, and this structural market change is accelerating under the weight of the COVID-19 pandemic.

What’s Next?

How are some of the segments under the greatest pressure going to navigate the impending changes to the markets?

At Forest2Market and Fisher International, we think about this a lot – it’s the foundation of our business. In a capital-intensive industry, the cost of good data is invaluable because better data leads to better decisions and, ultimately, better results.

How will COVID-19 and the resulting economic scenarios impact your business? What are the likely range of outcomes? For each scenario, do you have a playbook in place?

As a mill owner or supplier, your strategy to navigate the next year could vary dramatically based on what unfolds in the next day, week or month. And while the uncertainty is perhaps unprecedented, this shouldn’t stop business owners from being prepared.

In order to develop strategies, these are some of the fundamental questions management teams could be asking themselves:

- If demand does fall dramatically, where do your assets fall on the cost curve and will they survive?

- For exporters, are your facilities more at risk than those in other countries?

- How will future prices react in each scenario, and what’s your likely cash flow in each?

- Does your customer mix put you at risk?

- If company valuations fall, are you in a position to expand via an acquisition?

- What new products can you develop to serve changing markets?

Forest2Market and Fisher International are here to help you answer these questions, and better prepare for the structural market changes taking place across the globe.

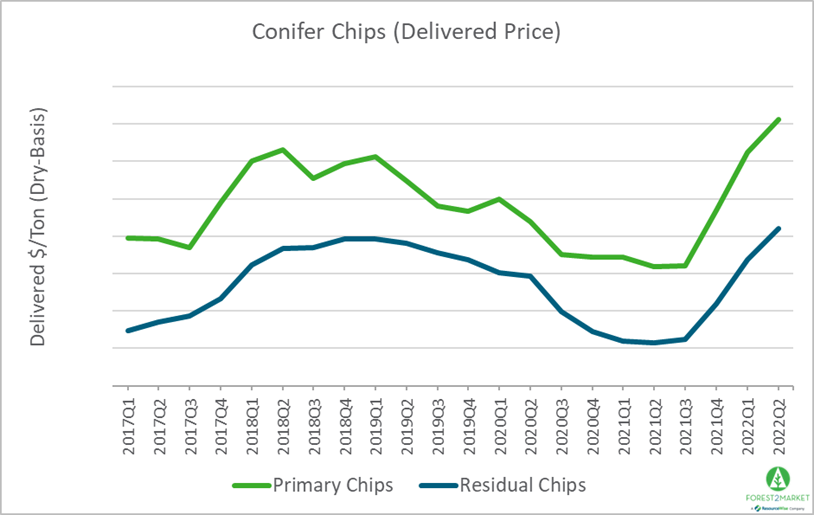

Wood Chip Supplies Diminish and Prices Soar in the Pacific Northwest

Labor union strikes and industry developments that have pinched the supply of conifer wood chips in the Pacific Northwest (PNW) now have a number of...

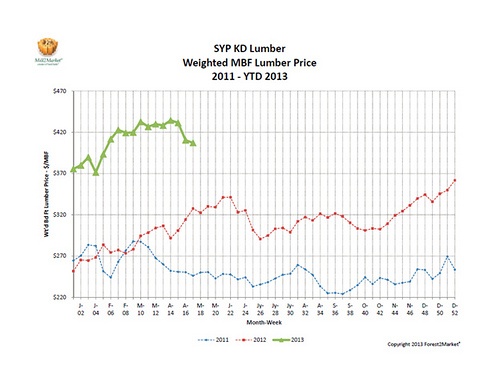

Southern Pine Market Takes a Breather

At the start of April, Forest2Market’s composite lumber prices reached the highest point of the year thus far at $434/MBF (Week 14). Prices steadily...

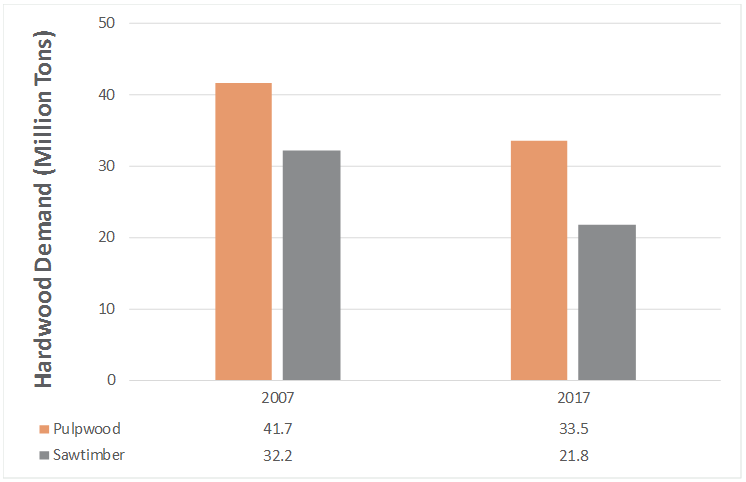

Loss of Hardwood Markets Represents a Structural Shift Affecting Residuals

This is the first in a series of posts covering the recently-published report compiled by Forest2Market titled “Changes in the Residual Wood Fiber...