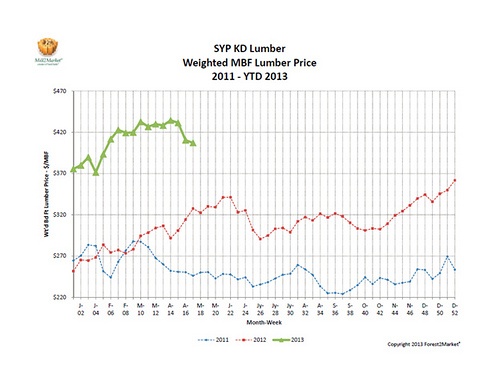

At the start of April, Forest2Market’s composite lumber prices reached the highest point of the year thus far at $434/MBF (Week 14). Prices steadily decreased in subsequent weeks, ending the month six percent lower at $407/MBF. Still, prices remain well above their levels of just one year ago.

Is 2013 shaping up as predicted? When we last wrote about southern pine lumber prices in A Perfect Storm?, we predicted the seasonal price drop seen in recent weeks. Increased mill capacity has met demand - allowing shipments to catch up with orders - and lumber buyers have reached satisfactory inventory levels for the first time since the sharp upturn in housing construction surprised the market during 4Q2012. As a result, lumber prices have fallen over recent weeks.

The cold, wet spring experienced throughout much of the Northeast and Upper Midwest exacerbated the current weakness seen in the market. As the days become warmer and drier in late spring and summer and construction activity picks back up, lumber prices are expected to level off.

Over the past several weeks, a 38 percent decline in multifamily starts has alleviated price pressure on 2x4s and 2x6s. Though single-family home starts also fell (by 2 percent) last month, building permit activity for these homes remains strong. Upward price pressure on the wides could follow if single family starts gain momentum. The long-term picture is still developing; it looks like prices are on a path to return to the historic trend line, though they will still remain above seasonal historical values.

The above figure summarizes pricing data gathered for Forest2Market’s weekly lumber market report, Mill2Market. For this report, Forest2Market aggregates sales order data submitted directly by report subscribers. This figure charts weekly sales order prices from January 2011 through year to date 2013 and compares sales order data, FOB Mill on a volume weighted $/MBF basis. The prices in the figure are composite prices; they include dimension lumber, timbers and boards.

Is Southern Yellow Pine Good for the Economy?

This post is republished courtesy of our friends at the Southeastern Lumber Manufacturers Association and “Wood. It’s Real,” which raises awareness...

Southern Yellow Pine Lumber Prices Steady in September

Southern yellow pine (SYP) lumber prices appear to have leveled out over the course of the last few weeks. Forest2Market’s composite southern yellow...

3 min read

9 Predictions for Global Wood Consuming Industries (& the NBA) in 2017

My predictions for global wood consuming industries (and the NBA) in 2017: US pulp and paper producers will experience some uplift as the economy...