Joe Clark

Joe Clark

The North American lumber sector has been front-page news for the past several months as exorbitant prices for finished lumber products have driven up new home costs by over $24.000. Prices for southern yellow pine (SYP) lumber have recently set new records by huge margins, and there’s no end in sight based on current demand patterns.

Forest products manufacturers from across the globe have been looking for entry points to the massive North American lumber market - a number of whom have been eyeing the US South as a reliable, low-cost destination. It’s such a popular spot, in fact, that new greenfield facilities combined with existing mill expansions will add roughly 2 billion board feet of production to the region over the next year.

What will this additional capacity mean for existing southern sawmillers, and how can they maintain relevance in a more competitive market when the inevitable downturn comes?

Recent History

In 2012, most SYP sawmills were figuring out how to be more profitable in the post-Great Recession market. Those that survived the US housing crisis and the Great Recession (the South lost 39 lumber/OSB mills from 2007-2017) were making decent profits for the first time in years, most had their pick of the oversupplied timber market, and the future looked bright. In that same year, the average mill was producing about 125 million board feet (MMBF) and they were doing it in only about 60 hours per week, which was more volume than they had produced before, and in fewer hours.

Many of these mills were bumping up against kiln drying constraints and couldn’t produce more lumber even if they were to run the standard 80-hour week. At that time, only a few mills in the US South were capable of producing more than 200 MMBF in a year.

Fast forward just a few years and the southern lumber landscape changed dramatically. By 2018, a number of new sawmills came online across the region—some of them boasting annual capacities of 250 to 300 MMBF. Existing mills have also aggressively expanded by adding drying capacity, running longer hours and upgrading equipment to take advantage of the favorable market conditions.

Looking Ahead

Today, after a 10-year acquisition spree, there are five companies who (combined) own more than 70 mills and control over 60% of regional lumber production capacity. As they continue to expand, these companies have incredible influence and flexibility within the market, and they are poised to be “market makers” for the foreseeable future.

The Beck Group projects that the average SYP sawmill production levels will rise from 125 MMBF in 2012 to over 200 MMBF in 2022. How does this compare to other regions? The following chart illustrates the relative scale of sawmill operations in key production areas of North America.

While large scale mills in the British Columbia (BC) Interior will continue to hold the top ranking for annual production per mill, SYP mills will rival production levels of their western counterparts due to the South’s stable flow of fiber and embedded supply chain.

Most importantly, segment leaders will also continue to innovate, improve conversion rates, gain market share, squeeze “more out of less,” and transform the southern sawmilling industry for the next decade.

What will this change mean for existing producers?

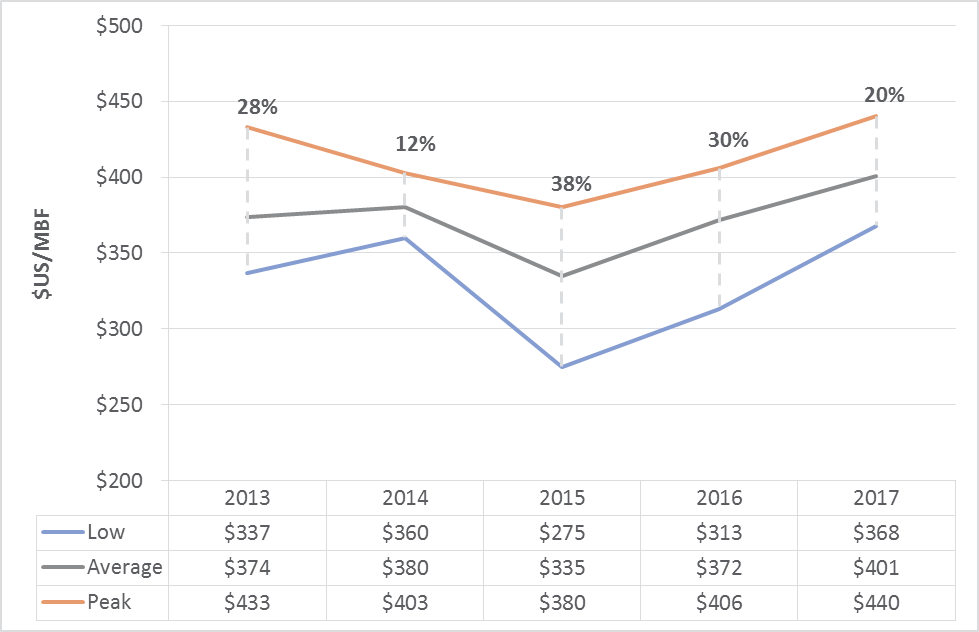

The increase in southern sawmill size and capacity will have significant impacts on productivity and manufacturing costs, delivered log costs, and other operating metrics in the coming years. With the rise of business intelligence, lumber manufacturers are becoming more sophisticated in how they collect and share data. The most sophisticated mills will use the increasing abundance of information to make data-driven decisions to rapidly identify and respond to changing trends, and forward-looking producers are planning ahead and investing now in preparation for the next down cycle.

Improved productivity, lumber recovery, superior grade yields and data-driven decision-making will allow these mills to maximize their productivity in a highly competitive environment. In turn, they will be better prepared to survive the next lumber market valley in order to take advantage of the next peak.

Sawmill TQ

The next step in maximizing sawmill profitability is Sawmill TQ, a partnership between The Beck Group and Forest2Market. Sawmill TQ provides a reliable benchmark for SYP sawmill performance that includes key metrics that drive profitability. The fresh, accurate and representative mill operation data delivered by this tool helps forward-looking SYP mills to improve efficiency in their supply chains—regardless of market turbulence.

Subscribers have access to the industry’s most sophisticated tool to help them better understand their economic health and position in the market while identifying areas of opportunity for improving profitability. Mill-to-mill data can be used to compare performance across a number of important metrics, including:

- Lumber sales realization

- Grade and product mix

- Byproduct price and revenue

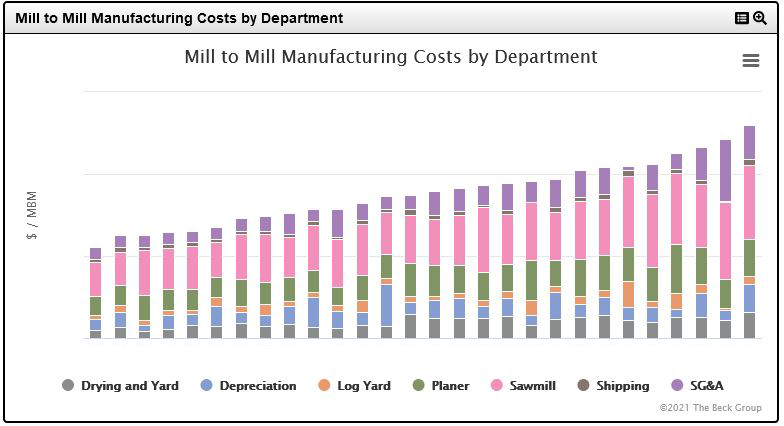

- Manufacturing costs by department and type

- Inventory and productivity

- Log costs

- Yields by product

If we have identified that a sawmill’s sales average is not as good as its competitors and peer group, the next step is to ask “why?”

The Future Needn't be Frightening

Insatiable demand and record lumber prices have really defined the larger market for the last year, and the southern sawmill industry is expanding aggressively to meet this demand. Whether your facility has been in operation for generations or you’re currently expanding and adding capacity in preparation for the future, Sawmill TQ can help you make better operational decisions, optimize your performance and plan for the future.

How Southern Lumber Manufacturers Succeed Despite Volatility

The North American lumber sector has been front-page news for the past several months, as sky-high prices for finished lumber products have markedly...

Sawmill TQ: A More User-Friendly and Timely Sawmill Benchmarking Service

Sawmill benchmarking allows mill management to objectively identify competitive strengths and weaknesses and opportunities for improvement in key...

2017 Southern Yellow Pine Lumber Prices: Quarterly Data and Yearly Comparisons

The North American lumber market experienced a wild ride in 2017.