While pulpwood prices across North America are driven by competition for fiber, we tend to see higher price volatility in pulpwood prices in the Northeast and Lake States due to availability factors that are unique to these markets. These factors include :

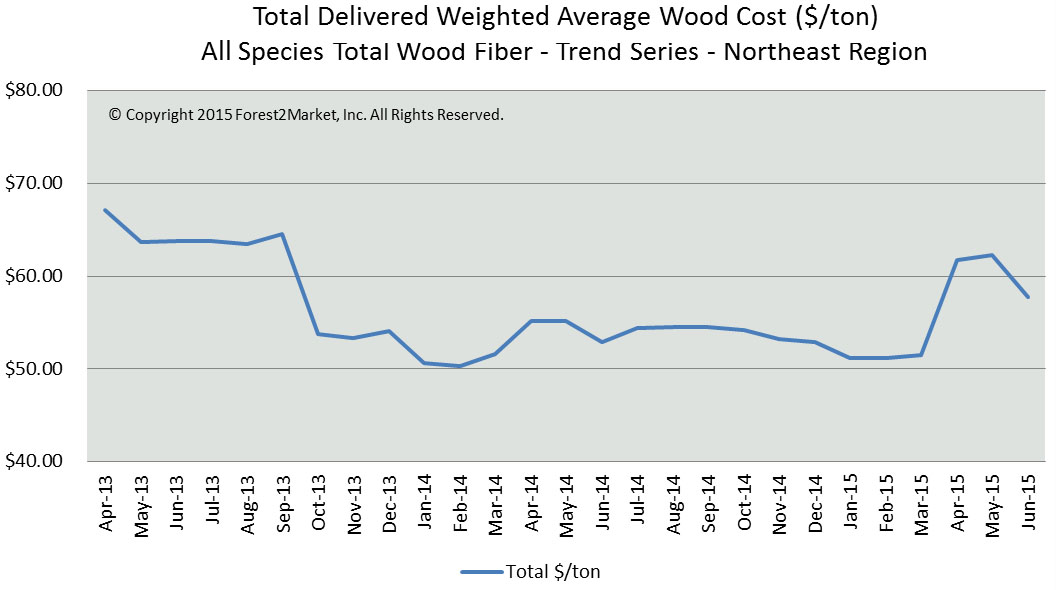

Seasonality – Wood production tends to be volatile in these regions from one quarter to the next. This is especially true when comparing a high production first quarter to a low production second quarter. In 2013, pulpwood prices were highest in April, with a volume weighted average wood cost of $55.62. Until the first quarter of 2014 when delivered prices dropped, prices had been fairly stable at $51 per ton. The lower price was partially due to an increase in available supply in the winter months. Higher delivered prices are fairly common in April and/or May as wood production is limited by weather. This 2014 winter harvest season was also longer than average with March hardwood pulpwood deliveries remaining extremely strong.

Distance Hauled – As the overall supply of hardwood increases during these months, mills are able to purchase wood originating in forests closer to the mill. Forest2Market’s Benchmark shows the average number of miles hauled (haul distance) in the Northeast during 4Q2013 as 93 miles; the average haul distance in 1Q2014 dropped to 80 miles. Lower haul distances coincide with lower delivered prices, such as those observed over the first quarter of this year despite the competitive fiber markets over the course of the winter.

Competition for Other Species and Other Types of Fiber – Logging capacity, particularly as it relates to the “surge capacity” needed to fill inventories during the winter or when unexpected events drive inventory shortfalls, has been a pervasive topic of conversation in the Northeast and Lake States. Capacity issues such as these often affect hardwood production. The overall supply of hardwood pulpwood, for instance, is affected by aspen and softwood demand and the availability of pulp quality chips. If softwood sawmills are running more hours, this will increase the supply of softwood chips, thereby freeing up constrained logging capacity for hardwood production. This interaction affected hardwood production this winter, and the additional supply lowered prices.

Supply Agreements – Supply agreements are frequently used in the pulp and paper industry with strict requirements for deliveries that affect the price of fiber on the open market. The nature of dynamic wood markets means supply agreements are often established at a time when market conditions were different than they are when the fiber is harvested and delivered. Depending on the calculation mechanism, this can create a delayed effect on market pricing.

While these factors come into play in all regions in the North American timber industry, they are typically more pronounced in the Northeast and Lake States regions. Price volatility is therefore higher in these regions as seasonality, haul distances, competition for other species and types of fiber and supply agreements put pressure on prices from opposite directions.

Pete Coutu

Pete Coutu