Suz-Anne Kinney

Suz-Anne Kinney

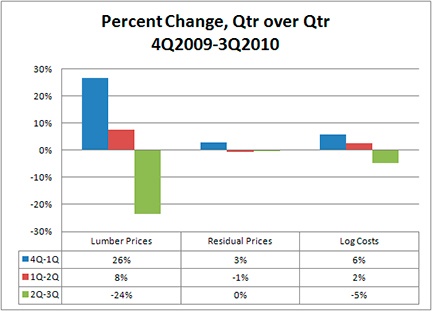

Last winter, total fiber prices escalated due to a significant increase in the haul distance required to move adequate supply to mills in the U.S. South. Local supply in the West-South and Mid-South, constrained by wet weather that prohibited logging, had to be replaced with chip shipments from the East-South, the Lake States, and even as far away as Nova Scotia and Brazil.

Since the end of 1Q2010, however, weather has returned to normal conditions, and as a result, prices have reverted to historical averages (see chart). Hardwood fiber suffered the biggest losses, with prices dropping 13 percent in third quarter, from $49.50/ton to $43.08/ton. Pine fiber prices fell 4 percent, from $36.92/ton to $35.53/ton in the third quarter.

During the winter, we expect to see moderately higher prices due to a normal seasonal increase in rainfall levels and increased demand over the holiday season for containers and paper. Holiday sawmill curtailments will add to these increases, as mills will need to replace a portion of their sawmill residuals with chipped pulpwood.

The most interesting event to watch over the winter will be the RWE pellet facility, Georgia Biomass. The company will reportedly start buying fiber in December as they prepare for a 2011 start-up.

Sawmills Reduce Production and Shed Inventory at the End of 3Q2010

Bracing themselves for a tough 4Q2010 and 1Q2011, sawmills in the South began cutting production and shipping from inventory at the end of 3Q2010....

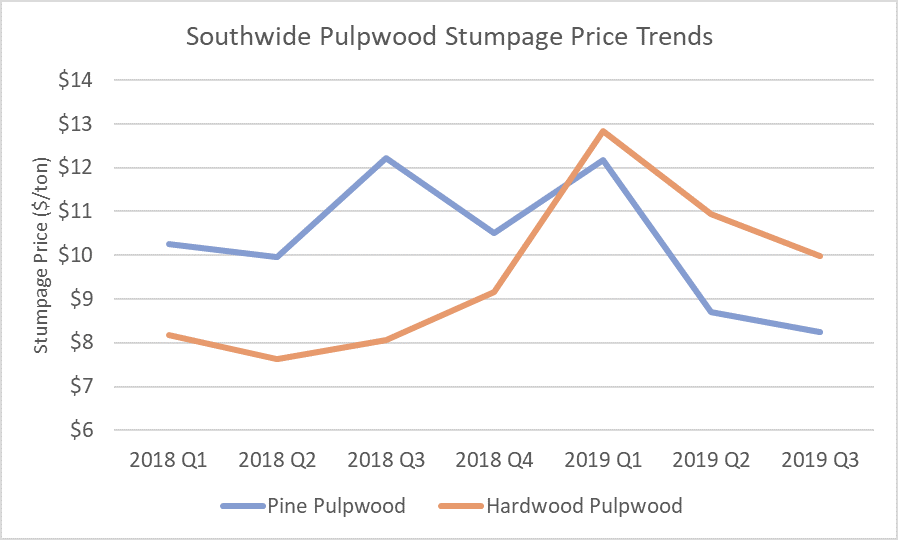

Southern Timber Prices Continued to Slide in 3Q2019

After skyrocketing in 1Q2019 due to prolonged wet-weather challenges, southern timber prices reversed course sharply in 2Q and the trend continued...

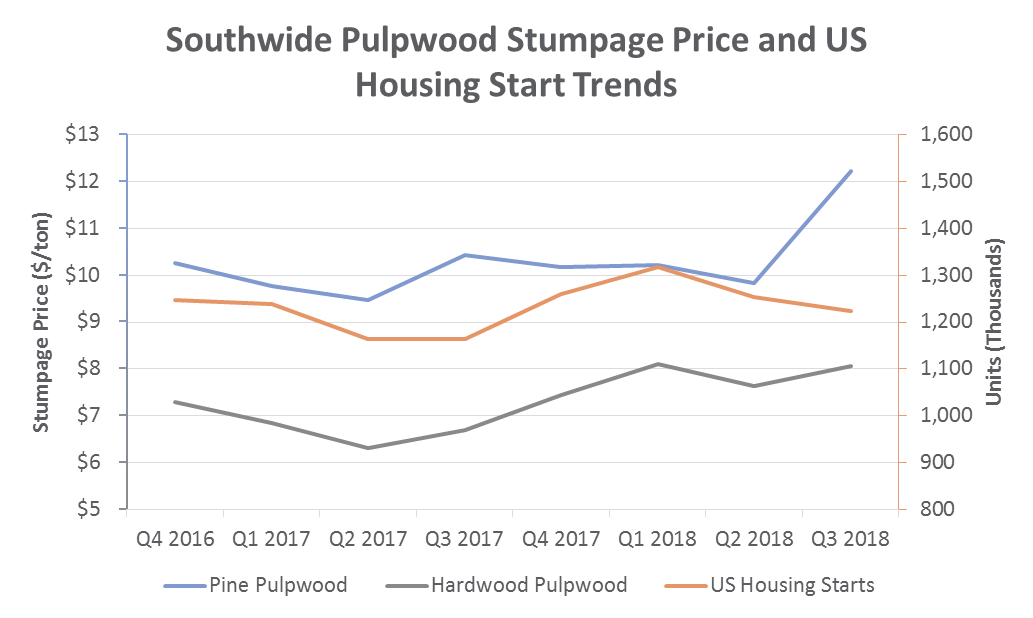

US South Timber Prices: 3Q2018 Performance & Outlook

US South timber prices during 3Q2018 were mixed. Pulpwood products increased significantly and pine log products decreased slightly, but the general...