3 min read

In January 2019, Resources for the Future (RFF), along with the US Endowment for Forestry & Communities, Inc. and the National Wooden Pallet & Container Association (NWPCA), commissioned the forest industry analysts at Forest2Market to perform a comprehensive analysis of the wood fiber residuals market. The resulting paper, Changes in the Residual Wood Fiber Market, 2004 to 2017, delivers important findings for the forest landowners, mill owners, and marketers of wood products in the United States and abroad.

But while the analysis was principally directed at the forest products sector, there are important implications for state and local policymakers in forestry-oriented regions of the United States as well.

The Forest2Market paper identified major trends that have shaped the wood fiber market over the past fourteen years, principally focusing on the American South and the Pacific Northwest, the two leading production centers for wood fiber.

As we described in a press release accompanying the report, the trends for the global markets for secondary wood fibers have created economic winners as well as losers: There is surging demand for softwood fiber (i.e., pine) driven by strong markets for cardboard boxes, disposable diapers, and the like, as well as bioenergy in the form of pellets. Exports of wood pellets from the United States have increased from essentially zero in 2007 to over 5 million tons in 2017, creating an economic boom for softwood producers and mills in the South. Softwood demand has also shown sustained growth in containerboard for cardboard boxes (annual increases of 2–4 percent) and fluff pulp (annual increases of 4 percent). But while softwood is booming, hardwood producers are suffering, driven by a continued slump in markets for printing and writing papers and other end products made from hardwood fiber.

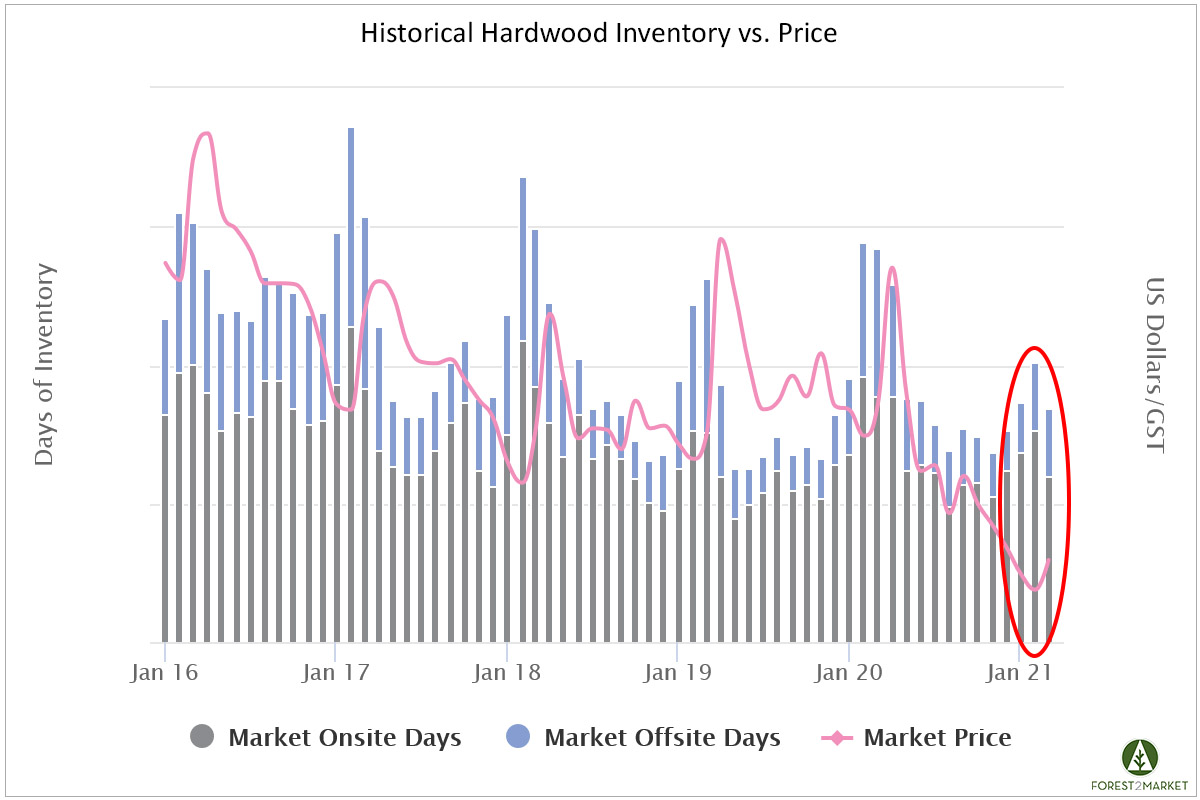

One of the most important challenges identified in the report is the long-term, structural decline for hardwood fibers. This poses particular challenges and opportunities in the South. RFF Vice President for Land, Water, and Nature, Dr. Ann M. Bartuska, noted, “A sustainable material like hardwood fiber still faces great challenges on several important fronts in the US South. For example, there has been a 25 percent decrease in the demand for hardwood fiber in the past 10 years, and the report bluntly cautions that the industry will have to address such areas to survive.”

The pulp and paper industry in the South has responded to these long-term trends by, for instance, shifting mill production from hardwoods (writing and printing papers) to softwood (pulp, containerboard, boxes, etc.). Existing mills are being redesigned and retrofitted to respond to the buoyant demand for softwood fiber driven by strong pulp and wood pellet markets. (Sixteen new pellet mills were constructed in the South between 2007 and 2017.) Manufacturers can respond relatively quickly to market demands, but forest landowners are squeezed economically when lands dedicated to hardwoods decline in value.

How can policymakers in the South respond? One important consideration is whether there is a role for state governments in developing transition plans to support foresters as struggling hardwood forests decline—i.e., can state policies assist them in identifying new markets or revenue plans to make up for the continued declining demands? There are also important ecological reasons why policymakers should consider supporting hardwood forest landowners during this decline. Hardwood forests and plantations in the South provide biodiversity and water climate benefits, including serving as habitat for important wildlife species and protecting source watersheds for residents. In the northern hardwood forests of the South, conversions to plantation pine is not an option. In the southern forests of the South, these conversions have already been made. But there are ecological and ecosystem services functions that are still at risk if landowners were forced by economic trends to convert these lands to non-forest uses, such as subdivisions or industry. If so, the conversion would likely result in diminished ecological and carbon storage value.

There are important policy questions for states in the Pacific Northwest as well. In Oregon, Washington, Idaho, Montana, and northern California, the markets for secondary wood fiber products have been stable and profitable, but shortages of hardwood and softwood fiber have hindered pulp and solid wood sector growth, resulting in stagnant production. But there are underserved future markets for expanding the Pacific Northwest production of ecologically sustainable secondary wood fibers.

In Oregon, Washington, and British Columbia, building codes are being changed to allow the use of cross-laminated timber (solid timber glued together in a pattern) and mass timber (pressed wood fiber with composite glues) in mid-rise and high-rise buildings. These locally-sourced building materials are poised to become major elements in the forestry economy, and Oregon is aspiring to become the center of the US mass timber production economy. State policymakers could consider further opportunities to expand this sector, which is both an ecologically sound resource (mass timber is lighter and takes less energy to produce than concrete and steel, while sequestering carbon) as well as economically promising. But for mass timber to really take off as a building material in the Pacific Northwest, the available supply of logs and residuals needs to meet the demand, which is unlikely given the shortage of wood fiber. As the Forest2Market report documents, the Pacific Northwest industry is resource-constrained due to four factors.

- A lumber industry where growth is constrained by the finite supply of logs

- Restricted harvest on federal lands

- Restricted log supply from Canada

- Export log and lumber demand from China

This creates important questions for policymakers in Oregon and Washington wishing to support the expanding mass timber and composite industries, while responding to popular and regulatory pressures that restrict timber harvest on federal and state lands.

RFF, working in collaboration with scholars, forest sector partners, and related experts, intends to continue developing our research and convening agenda on forest resources and markets. In coming weeks, we will hold a webinar with Forest2Market on trends in the primary and secondary forest products sectors, explore policy opportunities and challenges, and reflect on the prospects in both the South and the Pacific Northwest in expanding markets for forest products and preserving forest lands.

Michael Zwirn is Program Director for Land, Water, and Nature at Resources for the Future.

Evolving Forest Industry Creates Challenges for Lakes States Timberland Owners

The forest products industry has migrated away from the vertical integration model it used until the early 2000’s. While this trend has freed up...

The West’s Ravaged Woodlands—A Problem with a Proven Solution

The Economist’s recent article, “Ravaged Woodlands” paints a bleak picture of forests in the American West and the rate at which they are succumbing...

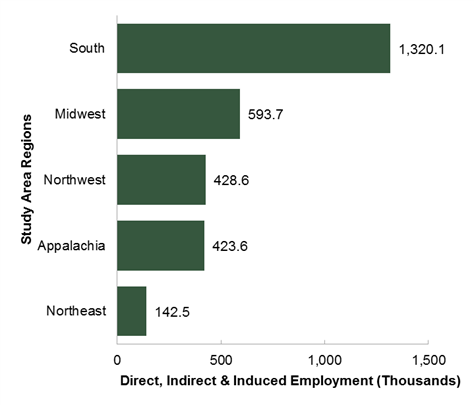

New Report Details the Economic Impact of US Forest Products Industry

Forest2Market recently completed an economic impact study for the National Alliance of Forest Owners (NAFO), which quantifies the contribution that...