2 min read

Recovery in the housing sector slowed throughout the first quarter of 2014. Housing starts remained below the one million mark needed to meet demographic growth, and both new and existing home sales sputtered. Despite continued gains, home prices have recovered only to mid-2004 levels. Mortgage interest rates, which have risen over the past year but remain low by historical standards, might also be contributing to weakness in the market.

An article recently published by the New York Times asserts a weak housing market is to blame for the stalled economy, noting, “In today’s economy, housing activity accounts for a smaller share of GDP than in the recessions that followed World War II. That activity would close nearly 40 percent of the gap between America’s current weak economic state and full economic health.” (GDP growth in 1Q2014 is currently estimated at 0.1 percent.)

The article goes on to suggest that if building activity reached its expected average proportion of the economy, it would add nearly 1.5 million jobs and reduce the 6.7 percent unemployment rate by a percentage point.

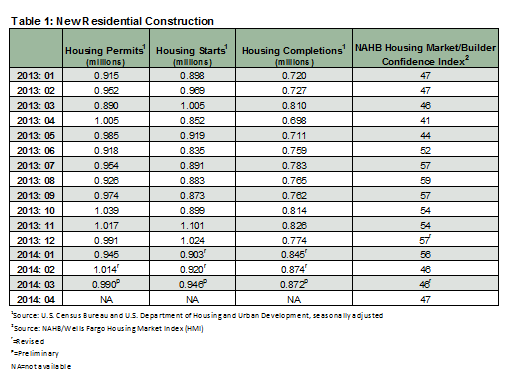

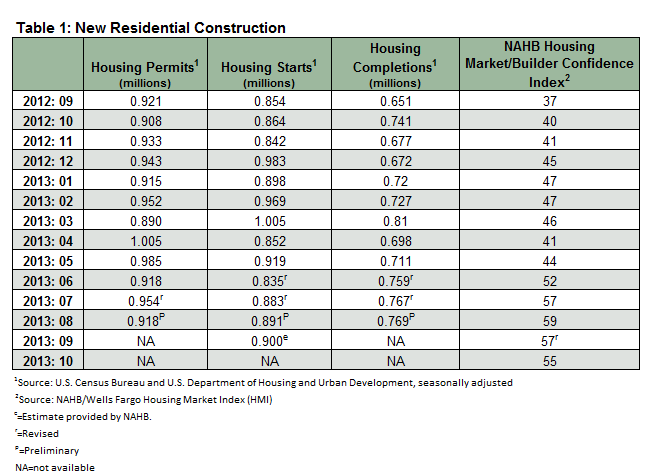

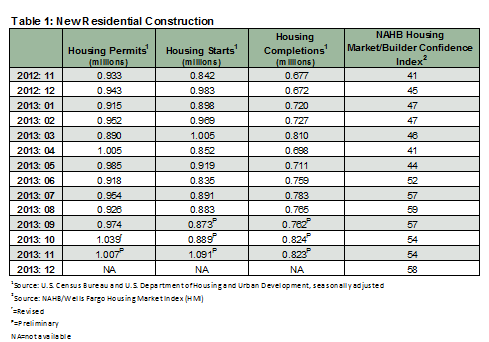

Housing Starts, Permits & Completions

Since rising above one million in November and holding on through December, housing starts have failed to remain strong through the first quarter of 2014. Despite inching up for the first three months of the year, March numbers show nationwide housing starts are down 5.9 percent from where they were a year ago. Most analysts believe starts were negatively impacted by the usually cold winter season.

One bright spot amidst the gloom is the strong housing permit statistic. Although permits fell 2.4 percent from over one million in February to 990,000 in March, the numbers indicate a strong building season in the coming months.

Completions have also been relatively strong, ranging from 845,000 to 874,000 throughout the first quarter and reaching numbers higher than those recorded during any month in 2013.

Builder Confidence

Positive expectations among builders at the start of the year have tapered off, tumbling 10 points from January to February. Confidence remained fairly low in March, and improved by one just one point to 47 in April. Builders cite ongoing issues such as limited lots and labor, increasing costs of building materials, and tight credit markets keeping buyers away for low expectations. It will be interesting to see if builder confidence improves next month as the spring buying season ramps up.

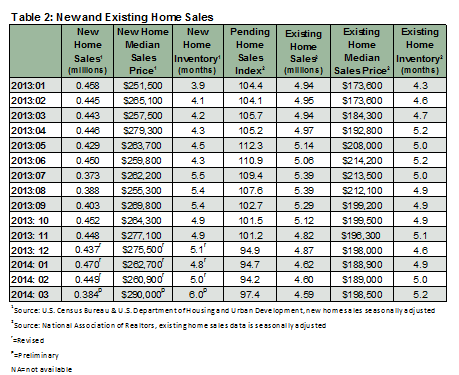

Home Sales & Inventory

New home sales reached their lowest levels in eight months in March, falling 14.5% from February and 13.3% from where they were one year prior in March 2013. The median sales price for new homes improved considerably to $290,000.

Existing home sales essential remained unchanged, down only 0.2% from February. Compared to one year ago, however, existing home sales are down 7.5%. Pending home sales spiked in March, although numbers have not risen above one million — where they spent the majority of 2013 — since December.

At more than 5 months of supply, existing home inventory is the highest it has been since June 2013, but consistently remains below the six-month supply indicative of a balanced market.

Home Prices

Year-over-year home prices rose 12.9 percent through February 2014, as reported by The Standard & Poor’s Case-Shiller index. Despite the increase, annual rates of gain slowed, and prices are forecasted to grow only by single-digits in the coming year.

Commenting on this trend, Chairman of the Index Committee David M. Blitzer noted, “The annual rates cooled the most we've seen in some time. On a month-to-month basis, there is clear weakness.” If rising home prices are indeed stalling home sales, prices may level off and fall in coming months.

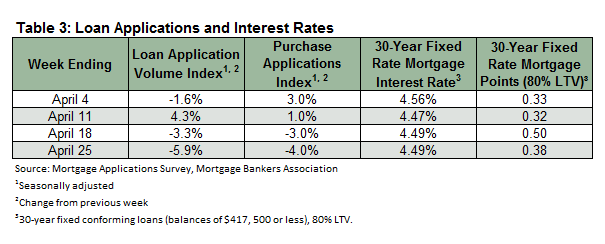

Mortgage Rates

As home prices were steadily on the rise, the volume of mortgage loan applications was more of a roller coaster, falling, rising, and then falling again to close out the month.

Hovering around 4.5% for a 30-year conforming loan, mortgage interest rates remain favorable although they are now a full point above the 3.44% low recorded in December 2012. The Federal Reserve’s decision to cut back on bond purchases will likely lead to higher interest rates going forward.

Although uncertainties around the availability of credit and irregular job growth hold down the market, most analysts forecast the housing market will slowly gain strength throughout the year.

Housing Market Update – September 2013

A limited supply of homes and a rise in interest rates over much of the summer discouraged many potential buyers during the historically busy summer...

Housing Market Update – November 2013

Housing Starts, Permits & Completions In its latest release, the Census Bureau provided three months’ worth of housing starts, permits and...

Housing Market Update - April 2010

Sales of both existing and new homes fell in February, with existing home sales slipping 0.6 percent to 5.02 million units and new home sales...