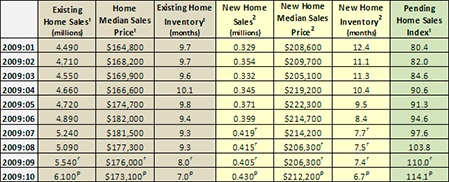

It’s been a long time since we’ve been able to report good news in the housing market. We saw an uptick in sales in December 2008! Sales of existing homes increased by 6.5 percent in December, primarily on the strength of buyers taking advantage of lower prices in distressed markets (Calif., Nev., and Fla.). The number of unsold homes on the market also fell, with inventory now at a 9.3 month supply (November’s inventory was 11.2 months). Median sales prices continued on trend, however, falling just under $5,000 to $175,400 in December.

Current indicators suggest this upward trend is unsustainable due to the flurry of layoff announcements and the number of foreclosures on the horizon. Recent action from the Federal Reserve, however, could prolong the upswing. On January 5, the Fed began the $500 billion program to purchase mortgage-backed securities from Fannie Mae, Freddie Mac, and Ginnie Mae. As of January 28, they had already purchased $70 billion of these securities. The Fed’s intention is to spend the entire amount by the end of June.

According to Bloomberg, the Fed’s program is “intended to lower rates by reducing the supply of outstanding agency mortgage bonds, boosting their prices and thus lowering their yields. Lower yields in turn reduce the interest rates banks need to charge on new mortgages to ensure profitable sales of the securities.” The Fed’s target interest rate is 4.5 percent, a rate that would make mortgage payments more affordable for more people. Rates for 30-year mortgages have been as low as 4.96 percent since the program began. The Federal Reserve also announced last week that it would purchase long-term Treasury bonds. This action would drive down long-term interest rates of all types.

Last week, the Obama administration announced it would spend between $50 and $100 billion of the remaining TARP (Troubled Assets Relief Program) funds to help homeowners avoid foreclosure. An additional plan by the Federal Reserve will allow regulators to revise mortgages it owns, the first round of rewrites will affect mortgages once owned by AIG and Bear Stearns. The Fed took these loans as collateral for bailout money provided to the companies in 2008. If successful, these initiatives could reduce foreclosures, which would stem the growth of housing inventory on the market.

Suz-Anne Kinney

Suz-Anne Kinney