Suz-Anne Kinney

Suz-Anne Kinney

This post on forestry related industry performance is excerpted from Forest2Market's monthly Economic Outlook, a 24-month forecast of macroeconomic indicators. For a comparison of last month's numbers, see Forestry Related Industry Performance - August 2014.

Industrial Production

Although industrial production (IP) continues to be a bright spot in the U.S. economy, its luster dimmed slightly in August when total output ticked down by 0.1%. Other details from the report showed:

- Manufacturing output fell 0.4% in August after jumping by 1.0% (the largest increase since February) in July.

- Wood Products and Paper output rose by 0.2 and 0.3%, respectively—on the heels of +1.0 and –0.6% respective performances in July.

- Construction slowed to a 0.1% increase after July’s +1.3%.

- Consumer Goods tumbled to –0.8% in August, more than erasing July’s +0.7%.

The capacity utilization rate for manufacturing fell by 0.6% in August (to 78.0%). Wood Products capacity utilization edged down by 0.3%, while Paper rose by 0.5%.

Manufacturing capacity expanded by 0.2% again in August. Wood Products capacity extended its upward trend with another 0.4% rise. Paper, on the other hand, contracted by 0.2% yet again—to its lowest point since January 1986.

Manufacturing and Non-manufacturing

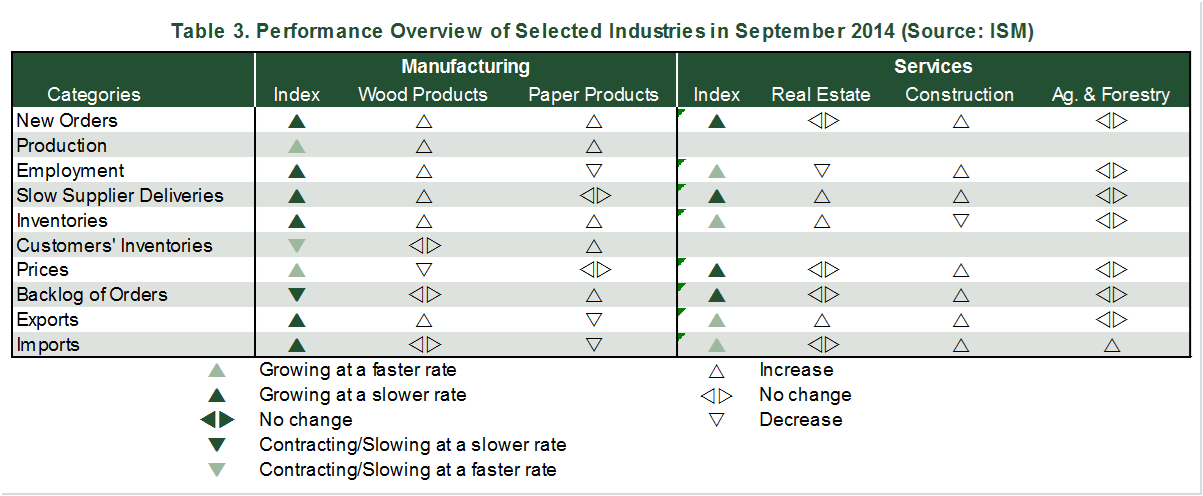

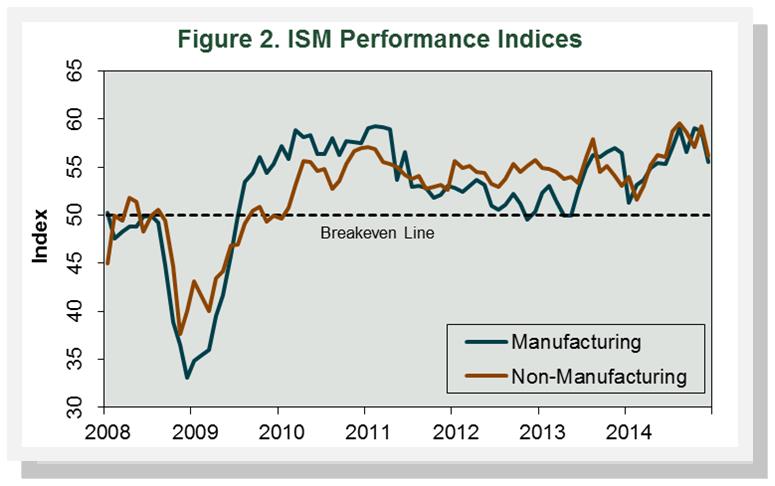

The Institute for Supply Management’s (ISM) monthly opinion survey showed that expansion of economic activity in the U.S. manufacturing sector stumbled in September. The PMI fell back to 56.6% (Figure 2), a decrease of 2.4 percentage points (50% is the breakpoint between contraction and expansion). All of the sub-indices weakened except for Production and Input Prices (Table 3).

Contrary to overall manufacturing, there was fairly widespread support among the sub-indices for the expansion in both Wood and Paper Products during September. One Paper Products respondent observed, “Outlook is very good; demand seems to be growing.”

The pace of growth in the non-manufacturing sector—which accounts for 80% of the economy and 90% of employment—also retreated in September. The NMI declined by 1.0 percentage point, to 58.6%; the drop appears to have been primarily concentrated in the New Orders and Orders Backlog sub-indices.

Two of the three service industries we track reported expansion in September, although only Construction had meaningful support among the sub-indices. “In the building industry there continues to be a lot of remodeling and smaller additions with replacement facilities and new buildings lagging,” wrote one Construction respondent. “Many companies would like to build new, but are still concerned about making the large investment at this time.”

Forestry Related Industry Performance - August 2014

This post on forestry related industry performance is excerpted from Forest2Market's monthly Economic Outlook, a 24-month forecast of macroeconomic...

Forestry-Related Industry Performance: March 2015

Forestry-related industry performance was mixed in February/March—not unlike the January data—in both the manufacturing and non-manufacturing sectors.

Forestry-Related Industry Performance: November/December 2014

Forestry-related industry performance at the end of 2014 was mixed. (Read Forestry-Related Industry Performance: November 2014.) Industrial production