This post is excerpted from Forest2Market's monthly Economic Outlook, a 24-month forecast of macroeconomic indicators.

Industrial Production

Industrial production (IP) rose 0.2% in June; total IP was 4.3% above its level of June 2013. For 2Q as a whole, IP was 5.5% higher than 2Q2013. Other details from the report showed:

- Manufacturing output increased by 0.1%, its fifth consecutive monthly gain.

- Wood Products output rose by 0.3%, slowing from May’s +1.4%.

- Paper also rose by 0.3%, partially reversing May’s -1.9%.

- Construction notched a 0.5% increase, a bit lower than the 1.4% gain in May.

- Consumer Goods were unchanged in June, after -0.3% in May.

The capacity utilization rate for manufacturing edged down by 0.1% in June (to 77.8%). Wood Products capacity utilization also nudged 0.1% lower, while Paper jumped by 0.6%.

Manufacturing capacity expanded by 0.2% again in May. Wood Products capacity extended its upward trend with another 0.4% rise. Paper, on the other hand, contracted by 0.2% to its lowest point since January 1986.

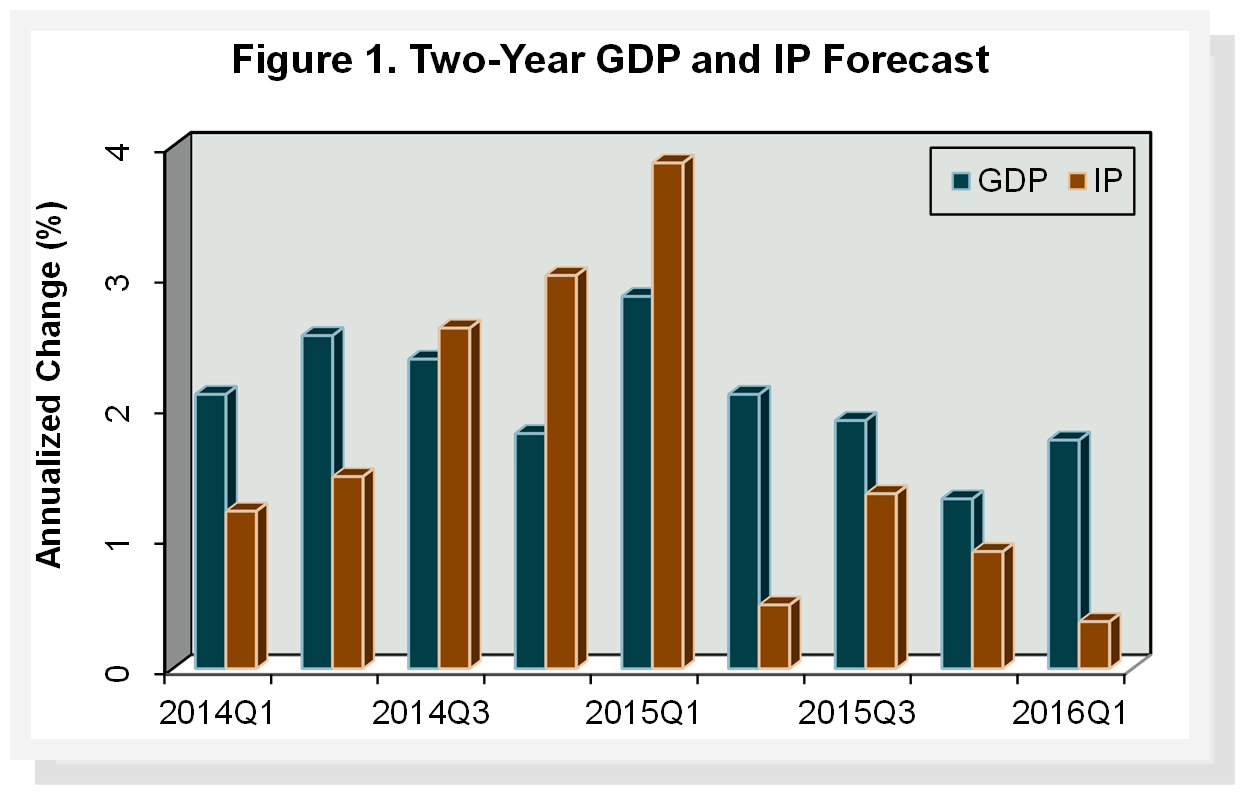

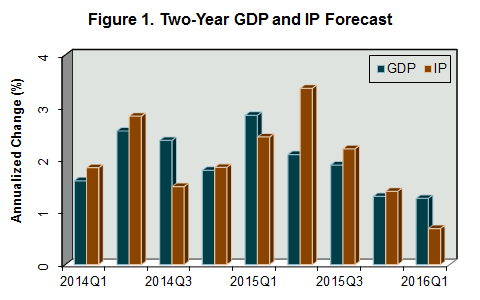

F2M forecasts that 3Q2014 IP will increase relative to 2Q2014 by an annualized rate of 2.7% (Figure 1). IP growth will subsequently fluctuate between -1.5% and 3.7% through the remainder of the forecast, averaging 1.4% overall.

Manufacturing and Non-manufacturing

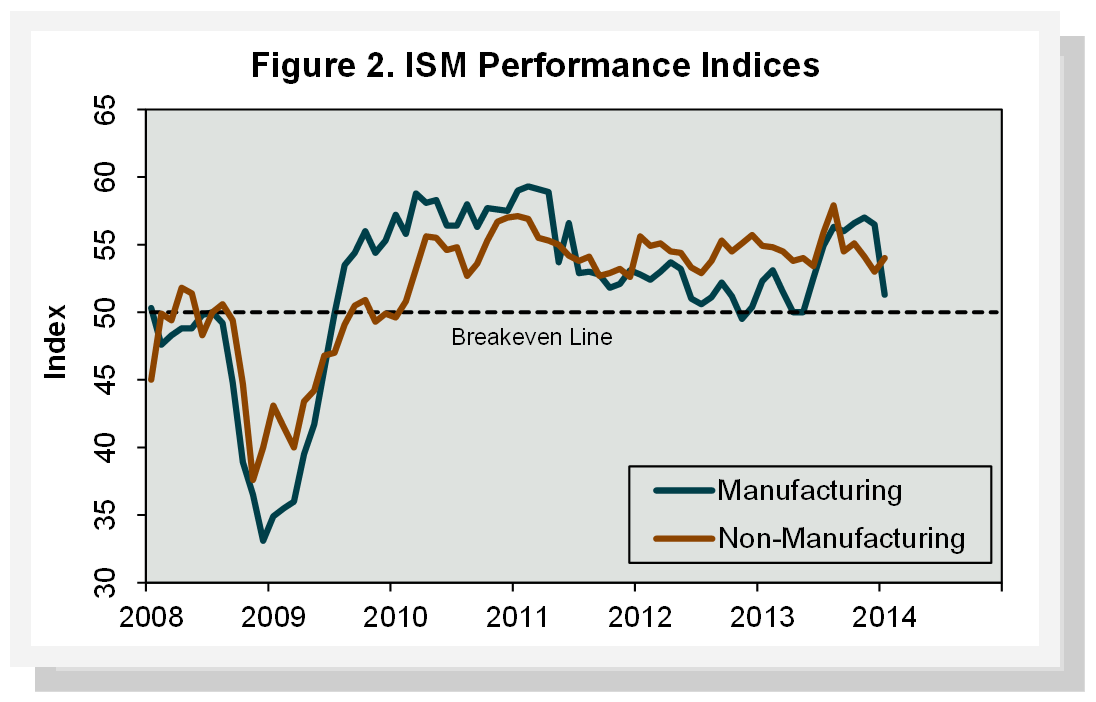

The Institute for Supply Management’s monthly opinion survey showed that expansion of economic activity in the U.S. manufacturing sector picked up speed (to the fastest pace in three years) during July (Figure 2). The PMI registered 57.1%, 1.8 percentage points above June’s reading (50% is the breakpoint between contraction and expansion).

Jumps in the new-orders, production and employment sub-indices were the main sources of support for the expansion (Table 3). Interestingly, the PMI’s rise appears to have resulted more from the seasonal adjustment applied to the new orders sub-index than from an actual uptick in activity. Although the not-seasonally adjusted new orders value for July was tied with June’s value at the lowest level since January, the seasonal adjustment factor pushed the new orders sub-index to the highest value since December.

Wood Products contracted in July thanks to shrinking new, backlogged and export orders. Paper Products expanded on the back of widespread support among the sub-indices.

The pace of growth in the non-manufacturing sector—which accounts for 80% of the economy and 90% of employment—jumped to a new record. The NMI registered 58.7%, a 2.7 percentage point gain. Real Estate and Construction expanded in July, while Ag & Forestry was unchanged.

Forestry Related Industry Performance - February 2014

This post is excerpted from Forest2Market's monthly Economic Outlook, a 24-month forecast of macroeconomic indicators. Industrial Production ...

Forestry Related Industry Performance - March 2014

This post is excerpted from Forest2Market's monthly Economic Outlook, a 24-month forecast of macroeconomic indicators.

Forestry Related Industry Performance - January 2014

by Forest2Market