This post on forestry related industry performance is excerpted from Forest2Market's monthly Economic Outlook, a 24-month forecast of macroeconomic indicators.

Industrial Production

Industrial production (IP) continues to be a bright spot in the U.S. economy. Total output increased 0.4% in July, racking up its sixth consecutive monthly gain. Other details from the report showed:

· Manufacturing output advanced 1.0% in July, its largest increase since February.

· Wood Products and Paper output both rose by 0.3%—as good as, or better than, the 0.3 and 0.1% respective gains in June.

· Construction notched an 0.8% increase, a bit higher than June’s +0.7%.

· Consumer Goods climbed 0.5% in July, up from +0.2% in June.

Total industrial capacity utilization crept higher, increasing by 0.1%, 1.7% above prior-year levels but still 0.9% below its long-run (1972-2013) average. Total capacity utilization is among the metrics used to measure “economic slack,” and is thus part of the Federal Reserve’s interest-rate “calculus.” These latest readings indicate that while there has been some tightening in utilization, there are no imminent concerns. The capacity utilization rate for manufacturing jumped by 0.9% in July (to 79.2%). Wood Products capacity utilization edged down by 0.2%, while Paper rose by 0.5%.

Manufacturing capacity expanded by 0.2% again in July. Wood Products capacity extended its upward trend with another 0.4% rise. Paper, on the other hand, contracted by 0.2% yet again—to its lowest point since January 1986.

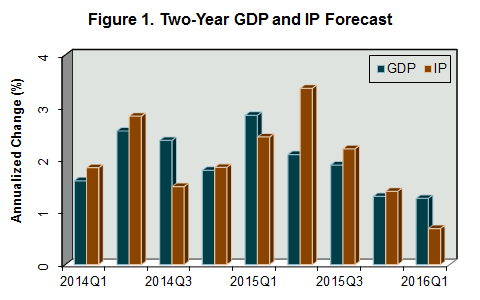

We expect 3Q2014 IP will increase by an annualized rate of 3.3% relative to 2Q (Figure 1). IP growth will subsequently fluctuate between -1.6% and 4.0% through the remainder of the forecast, averaging 1.6% overall.

Manufacturing and Non-manufacturing

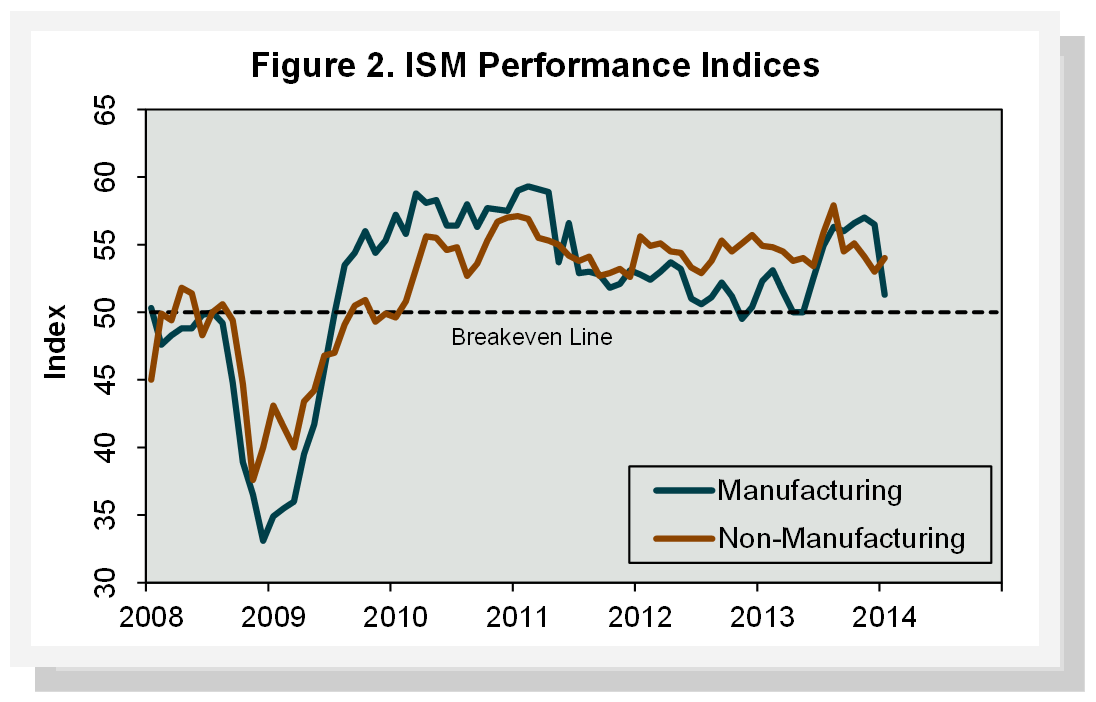

The Institute for Supply Management’s (ISM) monthly opinion survey showed that expansion of economic activity in the U.S. manufacturing sector picked up speed (to the fastest pace since March 2011) in August. The PMI registered 59.0% (Figure 2), an increase of 1.9 percentage points above July’s reading (50% is the breakpoint between contraction and expansion). Jumps in the new-orders, production, export and import sub-indices were the main sources of support for the increase.

Higher production and employment enabled Wood Products to expand in August (Table 3). “International markets are slower due to Eurozone holidays, political unrest and slowing Chinese markets,” countered a Wood Products respondent, however, adding, “North American business [is] off slightly.” Paper Products expanded thanks to higher new orders, production, order backlogs and exports.

The pace of growth in the non-manufacturing sector—which accounts for 80% of the economy and 90% of employment—rose to another all-time record. The NMI registered 59.6%, 0.9 percentage point higher than July; the push higher was concentrated in the Business Activity and Employment sub-indices.

Last month we reported the PMI rose primarily because of seasonal adjustments (instead of genuine activity) to the New Orders sub-index that converted an unadjusted six-month low value into the highest value in seven months. It was the NMI’s turn for similar treatment this month. Declining unadjusted New Orders and Employment sub-index values were turned into some of the highest values of the past several years.

All three service industries we track reported expansion in August, although only Construction had much breadth of support among the sub-indices.

Forestry Related Industry Performance - January 2014

by Forest2Market

Forestry Related Industry Performance - March 2014

This post is excerpted from Forest2Market's monthly Economic Outlook, a 24-month forecast of macroeconomic indicators.

Forestry Related Industry Performance - July 2014

This post is excerpted from Forest2Market's monthly Economic Outlook, a 24-month forecast of macroeconomic indicators.