Suz-Anne Kinney

Suz-Anne Kinney

Factory output continues to be a bright spot, but construction spending – especially the residential component – is unlikely to add substantially to GDP growth for quite some time.

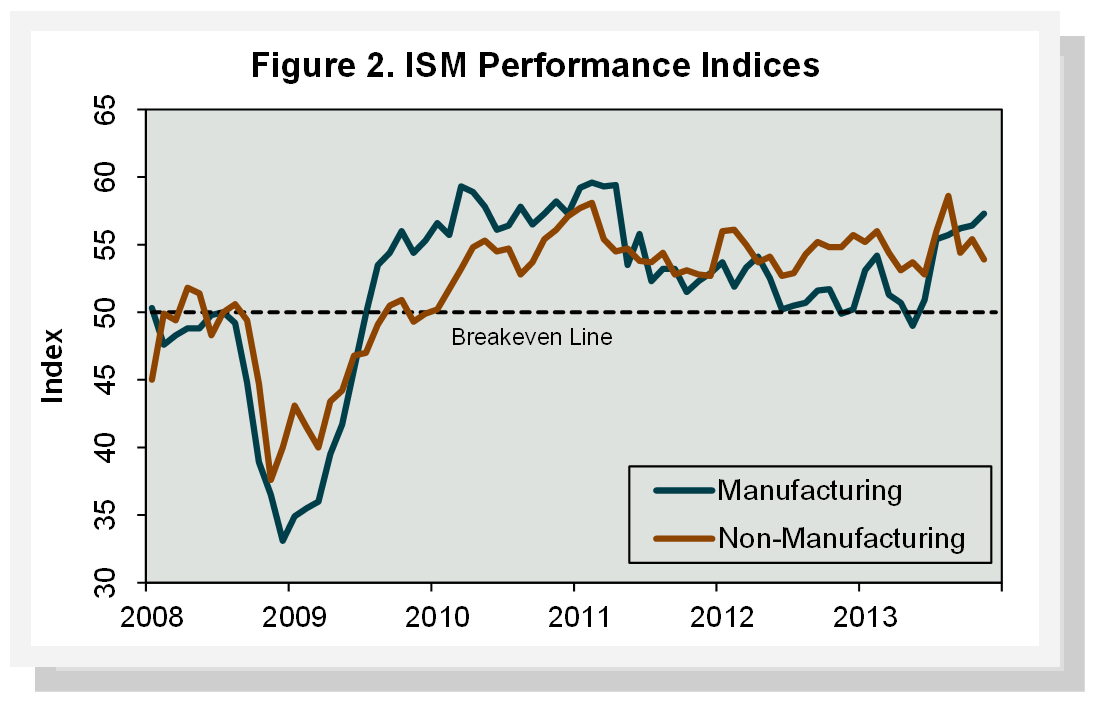

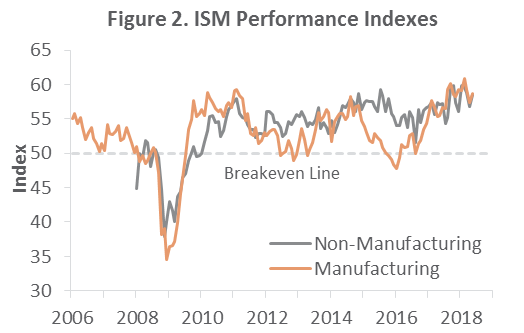

Although the Institute for Supply Management’s reports on manufacturing and service-sector activity showed stable or slightly slower rates of growth in May, new orders across all of the industries related to the forest products sector showed promise (Table 1).

Table 1. Performance overview for Forest-Related Industries.

Data source: Institute for Supply Management

New orders were up across the board in these industries. Most of those new orders were placed by domestic firms, though, as new export orders were less robust. The lack of export orders is not surprising in light of recent dollar strength; continued appreciation will likely undercut U.S. exports and reduce domestic manufacturers’ market share of the U.S. and global markets.

Inputs cost more in May, although the price increases were smaller than in April. Commodities whose prices rose in May included corrugated products and containers, fuel, lumber and wood products, paper and paper products, and pulp.

Across all industries, the U.S. Census Bureau reports that shipments, which have gained ground ten of the last eleven months, increased $2.5 billion or 0.6 percent to $422.3 billion. (Table 2).

Table 2. Shipments, Inventories & New Orders, by Industry.

Data source: U.S. Census Bureau

Shipments of wood products rose 4.9 percent, to $7.3 billion dollars—t he fourth consecutive monthly increase. Paper products shipments took a breather after rising for seven months and remained unchanged (Figure 1).

Figure 1. Value of Shipments, by Industry.

Data source: U.S. Census Bureau

Data from the Association of American Railroads provides another (and in this case, more pessimistic) view of shipping activity in the United States. Rail traffic fell by double-digit percentages in April, relative to March, but most categories are still well ahead of year-earlier volumes (Table 3).

Table 3. US Rail Traffic, by Commodity

Data source: Association of American Railroads

Inventories, up six of the last seven months, increased $2.6 billion (0.5 percent) to $521.7 billion (Figure 2). The inventories-to-shipments ratio was unchanged at 1.24. Inventories of manufactured durable goods increased 0.7 percent, thanks to primary metals. Wood products inventories backed off 0.7 percent, after four months of increases, while paper products rose 1.0 percent.

Figure 2. Value of Inventories, by Industry

Data source: US Census Bureau

If you would like a detailed forecast for forest-related industries, subscribe to Forest2Market’s Economic Outlook, a 24-month forecast of performance in GDP, currency exchange rates, housing starts, oil prices and more.

Let Forest2Market do the groundwork; subscribe to the Economic Outlook and focus your resources on identifying and acting on the strategic advantages you’ll discover there every month.

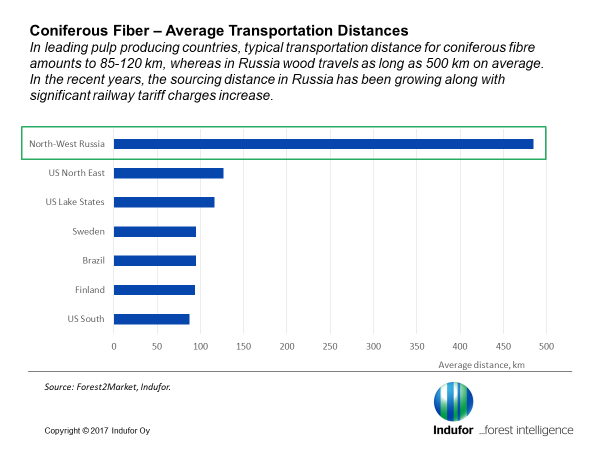

Forest Industry in Finland & Russia: Opportunities & Challenges

With a shared border, similar terrain and climate, tree species and growing seasons, Finland and Russia have dense forests and active forest...

Forestry-Related Industry Performance—November 2013

After edging up by 0.1% in October (revised from -0.1%), the seasonally adjusted industrial production (IP) index gained another 1.1% in November....

US Forest Industry Performance: May 2018

US forest industry performance in April and May was recently reported by both the US government and the Institute for Supply Management.