Suz-Anne Kinney

Suz-Anne Kinney

Wood Products manufacturing fell back by 0.4 percent in October, and remained 5.0 percent below its year-earlier level. Paper rose 1.4 percent, and was 5.5 percent below its October 2008 level.

The capacity utilization rate among Wood Products manufacturers ticked lower (-0.1 percentage point) to 50.5 percent, while Paper jumped 1.1 percentage points (to 74.9 percent). Wood Products and Paper were, respectively, 12.0 and 3.7 percent below their year-earlier levels.

Wood Products shipments increased by 1.1 percent, but were 4.2 percent below the October 2008 level. Paper Products declined for a third consecutive month (by 0.4 percent) and were 12.1 percent below year-earlier levels.

Wood and Paper Products inventories both shrank by 0.8 percent; respective annual changes were -11.5 and -13.4 percent. Interpreting these small monthly inventory changes is difficult at this stage of the business cycle. They may be signaling that production is running ahead of shipping and will require manufacturers to cut back to bring inventories back into alignment. Alternatively, it’s possible manufacturers are responding to other signals in their supply chains and building inventory to meet anticipated oncoming customer demand.

The woes continued for Wood Products in November. About the only ray of sunshine to hit that industry was the report of shrinking customer inventories; a smaller backlog of orders is putting pressure in the opposite direction, however. Paper Products, by contrast, still looked quite healthy – with higher input prices being essentially the only category of not-so-good news.

Construction exhibited fairly consistent strength in November, while Real Estate, Rental & Leasing put in a mixed performance. One Real Estate respondent observed that, “U.S. business remains better than 2007 levels, although it’s been through personnel and cost reductions that we are now profitable. Business continues to be about 8 percent below 2008 levels.” The only information on the Agriculture, Forestry, Fishing & Hunting sector was that input prices declined.

Performance Overview of Wood and Paper Products

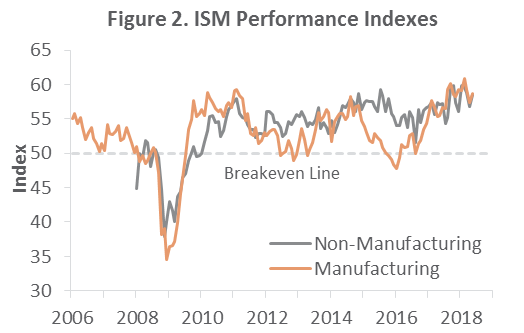

Source: Institute for Supply Management, October 2009

Turning to trade in U.S. forest products, the picture that emerges is one that mixes weak global and domestic demand and a weak U.S. dollar. Weak demand translates into lower trade overall, while the weak U.S. dollar discourages imports to meet domestic demand. Exports of wood pulp, paper and paperboard declined by 5.9 percent between August and September, while imports dropped by 3.4 percent. Exports were 3.9 percent higher than year-earlier levels; imports were a whopping 33.7 percent lower. Another bright spot for American pulp and paper manufacturers is that even though 2009’s year-to-date (YTD) exports have generally deteriorated over the past six months (when compared to YTD 2008), imports have fallen off at an even greater pace. The net result is that the annual YTD change in net exports has improved from -14.0 percent in March to -1.6 percent in September.

Lumber exports fell by 10 percent on a volumetric basis between August and September, while imports decreased by 7.0 percent. Exports in September were 7.0 percent lower than September 2008 levels; imports were off 29.4 percent. Softwood lumber has not shown the same progress in 2009’s YTD net exports (relative to YTD 2008) that pulp and paper has; the annual changes YTD net exports have remained mired between -35 to -40 percent over the past six months.

This summary of the performance of forest-related industries over the most recent period is part of the data upon which Forest2Market’s Economic Outlook is based. The Economic Outlook is produced monthly and provides a 24-month look at the economic factors that affect forest-related industries. Also available is a 24-month forecast of stumpage prices in multiple regions across the U.S. South. For more information, call (704) 540-1440 or click here.

Forestry-Related Industry Performance At a Glance: November 2009

Wood Products manufacturing rose 0.1 percent between August and September, but remained 20.3 percent below its year-earlier level. Paper fell 0.4...

Supply Chain Woes Begin to Pinch US Manufacturing Performance

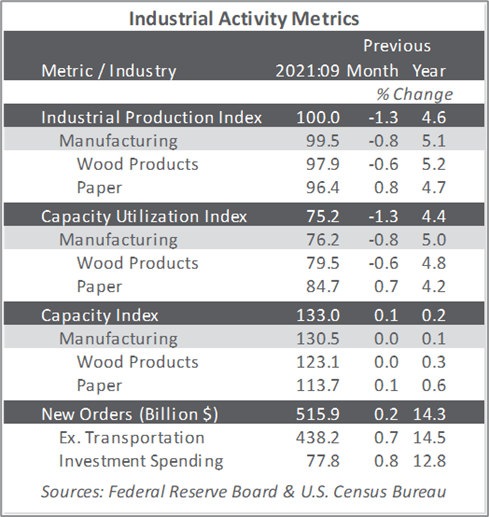

Following a -0.5PP revision to August’s data (to -0.1 percent MoM), total industrial production (IP) fell another 1.3 percent in September (but +4.6...

US Forest Industry Performance: May 2018

US forest industry performance in April and May was recently reported by both the US government and the Institute for Supply Management.