Global economic indicators have plunged at an alarming rate over the last three weeks as the coronavirus pandemic has tightened its grip on global markets spanning nearly every sector imaginable.

It’s too early to tell how it will impact the US housing market in the near and long terms, however, as the virus-induced panic we’re witnessing is without recent precedent.

While US homebuilding showed signs of moderating in early February, the final numbers weren’t bad… all things considered.

Housing Starts, Permits & Completions

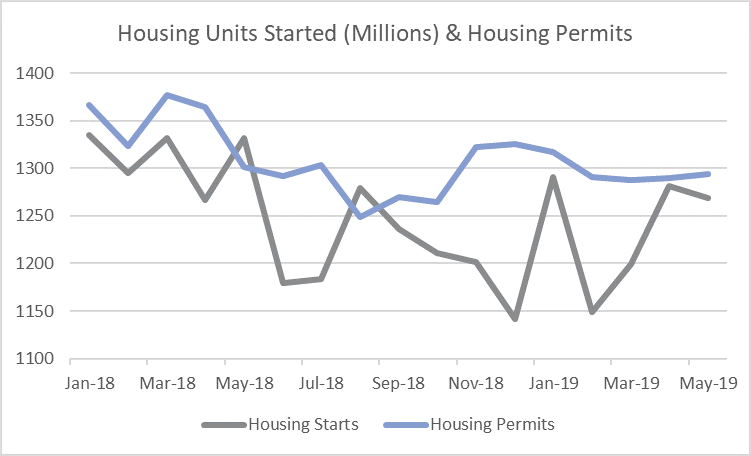

Privately-owned housing starts were down 1.5 percent in February to a seasonally adjusted annual rate (SAAR) of 1.599 million units. Single-family starts increased 6.7 percent to a rate of 1.072 million units; starts for the volatile multi-family housing segment dropped 17 percent to a rate of 508,000 units.

Privately-owned housing authorizations decreased 5.5 percent to a rate of 1.464 million units in February. Single-family authorizations were up 1.7 percent to a pace of 1.004 million units. Privately-owned housing completions were down 0.2 percent to a SAAR of 1.316 million units. Per the US Census Bureau Report, seasonally-adjusted total housing starts by region included:

- Northeast: -41.4 percent (+31.9 percent last month)

- South: +15.2 percent (-5.4 percent last month)

- Midwest: +16.7 percent (-25.9 percent last month)

- West: -18.2 percent (+1.2 percent last month)

Seasonally-adjusted single-family housing starts by region included:

- Northeast: +3.0 percent (+3.1 percent last month)

- South: +18.5 percent (-12.2 percent last month)

- Midwest: +4.9 percent (-15.1 percent last month)

- West: -13.8 percent (+14.2 percent last month)

The 30-year fixed mortgage rate plunged in February from 3.62 to 3.47, the lowest level since 2016. According to the latest National Association of Home Builders (NAHB)/Wells Fargo Housing Market Index (HMI), homebuilder confidence dipped two points lower to 72 in mid-March.

The numbers seem good on paper, however: “It is important to note, half of the builder responses in the March HMI were collected prior to March 4, so the recent stock market declines and the rising economic impact of the coronavirus will be reflected more in next month’s report,” said NAHB chief economist Robert Dietz.

Trends Will Change

For February’s analysis, we’ve chosen to look at the most recent two years’ worth of housing starts data to visualize trailing averages rather than month-over-month (MoM) performance. Trailing averages allow us to compare a measurement against a similar measurement from a prior term to decipher how much growth (or loss) was realized. Based on that growth, trailing averages also provide a more representative snapshot of overall performance over time, as well as growth trajectory.

While a simple trailing average chart is not meant to substitute as a comprehensive forecast, the chart can be used to discern general indications of market direction. What can we determine from the trailing average data in the chart above?

- The trailing 3-month average line naturally demonstrates more volatility than the trailing 12-month average line, which covers a longer period of time and smooths out some of the peaks and valleys. However, monthly housing starts spiked in 4Q2019 and 1Q2020 and the data for both the 3-month and 12-month averages illustrate solid performance.

Judging by the chart above, one would assume housing starts were just entering a significant boom period. However, the data doesn’t account for the surreal developments of the last four weeks.

While the US homeownership rate rose to a six-year high in 4Q2019—led by gains among young people and low-income Americans—the COVID-19 situation is creating a “new normal” in ways previously unimaginable.

- Global supply chains are fraying under tremendous stress.

- The DJIA has shed 33 percent of its value as of this writing amid wildly volatile trading sessions that have demonstrated 3,000-point swings.

- Oil prices have plummeted to their lowest levels in over 20 years to $22.80/barrel.

- Americans are being asked to “shelter in place” to avoid contact with others.

- Millions of workplaces are facing closures that will spawn a massive wave of new unemployment claims in the coming months; Treasury Secretary Mnuchin said unemployment could rise to 20 percent without government intervention.

- General anxiety is exceedingly high and gun/ammunition sales are through the roof as a result. FBI background checks were up 34 percent in February alone, and March numbers will likely be much higher.

Joel Kan, Mortgage Bankers Association's (MBA) associate vice president of Economic and Industry Forecasting, said: "The ongoing situation around the coronavirus led to further stress in the financial markets late last week, with unprecedented volatility and widening spreads.”

The FED took its most dramatic step since the Great Recession of 2008 when it recently announced a cut to its target interest rate near zero, which will take the target range for the federal funds rate down from the 1.25 percent range to the 0.25 percent range. Such a move doesn’t leave much wiggle room should the situation further deteriorate.

Based on the extremely fluid situation and abundance of caution, commercial and residential building is grinding to a halt. The reality of the situation is likely to show up in the forthcoming economic data—including next month’s housing starts numbers.

The trend above will undoubtedly change and track downward in the coming months. Let’s just hope the steady progress the sector has built upon over the last two years is strong enough to sustain even the unthinkable.

US Housing Starts Skyrocket in January, Lose Ground in February

US housing starts skyrocketed in January, increasing more than expected as construction of single-family housing rallied after four straight months...

Housing Starts Take a Step Back in May

Despite some promising signs in April—and on the heels of March data that was revised upward—the US homebuilding industry can’t seem to string...

US Housing Starts Spring to Life in April

Providing a much-needed spark to the sputtering housing market, US housing starts jumped significantly in April as gains were reported in both...