Tim Woods

Tim Woods

A lifetime ago (in March) like most of the world, Australia was holding its breath, waiting to see the effects of the COVID-19 pandemic. Our main concerns were related to health issues - some of which have dissipated despite remaining very real.

The full economic effects are yet to be felt. That seems unimaginable with literally millions of people losing their jobs, ceasing the search for work, or being supported by the Australian JobKeeper program.

Trade data for March – both imports and exports – appears to have been as expected, pre-pandemic. That will change when new data for May is released, and the same applies for the housing data.

What are the unfolding impacts to individual forest markets?

Woodchip Exports

On the forward indicator front, our long-run vessel tracking indicates that in May, woodchip exports from Australia will be at their lowest monthly level in more than eight years. We project that May exports will fall below 300,000 bdmt, with just eleven vessels expected to leave Australian ports for the month.

A slowdown was already underway in the hardwood chip market, especially for market pulp mills, where the low price of pulp sits very uncomfortably with the relatively high price of Australian hardwood chips.

Announcements by major woodchip exporting businesses that they are shuttering for at least three months fed into that in the third week of May, as did the announcement that Carter Holt Harvey would cease supplying LVL into Australia from its New Zealand operations.

The September quarter will be most telling. Analysis conducted by IndustryEdge during late April and early May suggests the major impacts of the pandemic will be felt in the September quarter of 2020.

Log Exports

Back open for business after one of the world’s most extensive lockdowns, New Zealand log exports are bounding along right now, with delivered prices in China reportedly at year-long highs. Coupled with crashing ocean-freight rates and a low New Zealand dollar, doubtless the returns for growers in New Zealand are great.

But log inventories continue to mount in China and the construction sector is reportedly only at 60% of pre-pandemic levels. Again, it is hard to see a September quarter where demand will be higher than the current quarter. Indeed, the market is just as likely to change before the end of June.

Housing & Softwood Lumber

In March, before the COVID-19 pandemic gripped the global economy, there were 15,386 new dwellings approved in Australia - down less than 1 percent on the prior month. It now seems certain that had the pandemic not impacted confidence in the latter part of the month, approvals would have been higher, heralding the much-anticipated housing sector recovery.

Our sawn softwood apparent consumption model showed March was a strong month, with all the evidence of a recovery being underway.

However, after eight weeks of a COVID-inspired economic shutdown, evidence continues to mount of a very steep downturn in demand for sawn timber in Australia, with the worst effects also unlikely to be felt until the September quarter. That does not bode well for jobs, wages, expenditure and therefore, for demand for any product.

The primary driver for falling timber demand is simple: a slump in dwelling approvals that appears to have commenced late March and that is already in May flowing into reduced building activity. The evolving situation is reportedly similar around the nation, impacting the entire supply-chain, hundreds of businesses and thousands of employees.

Relevant Market Data Provides Market Guidance

We are not alone in expecting a sharp downturn to be at its worst sometime in the September quarter. Our data-centric observations all point to that outcome. But as well as being alarming, these are strange times. So, like the New Zealand log export ‘moment in time’ opportunity, we can expect to see more of the same in different sectors as disruptions wreak their varied havoc.

Taking advantage of the opportunities relies on having access to independent data and fearless analysis and commentary. We continue to focus our attention on this Wood Market Edge data and analysis service for that reason.

To support subscribers with increasing levels of data, next month will see the commencement of New Zealand import and export data being included on the Wood Market Edge data and analysis service and platform. We also expect to add access to Vietnamese woodchip export data in the next few weeks.

PiiMega Adds Forest2Market Data Export Module to PiiMega® ForestPro and TimberPro

Subscribers to Forest2Market’s Baltic Rim Benchmark service who manage their entire supply chain with PiiMega® ForestPro or PiiMega® TimberPro can...

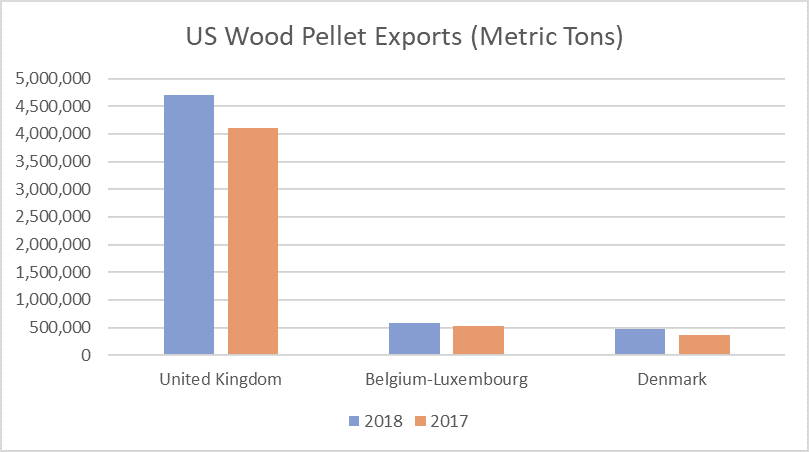

US Wood Pellet Exports Increased 17% in 2018

Per recent data released by the USDA Foreign Agricultural Service (FAS), the US exported over 6 million metric tons of wood pellets in 2018, which...

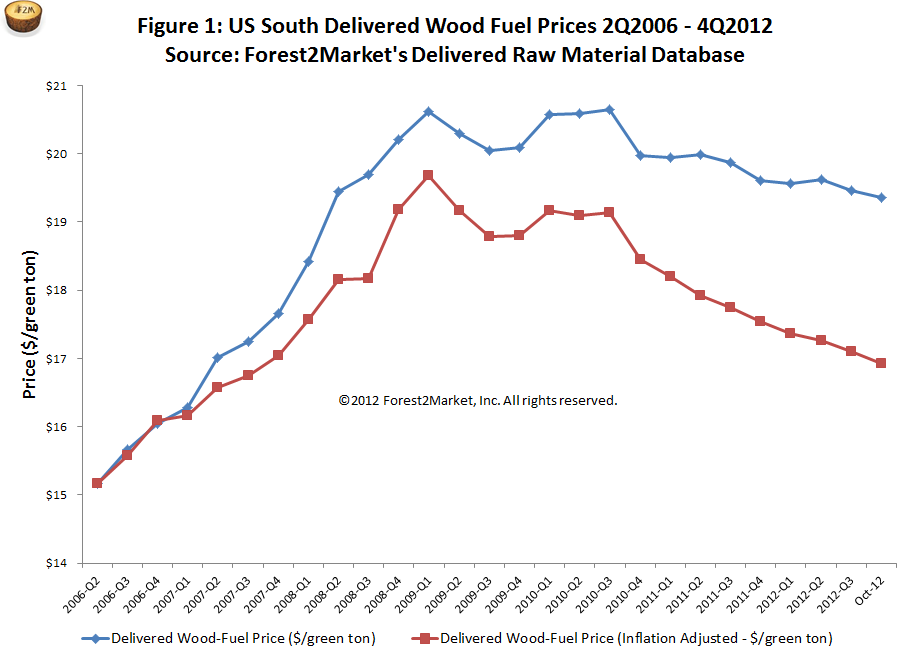

Wood Fuel Prices in US South Continue to Fall

Wood-fuel prices have followed a downward trend since 3Q2010. Based on October 2012 and preliminary November 2012 data, we expect this trend will...