Suz-Anne Kinney

Suz-Anne Kinney

In March 2007, Forest2Market economists Mike Huebschmann and Tom Montzka warned the inverted Treasury yield curve at that time was signaling a likely recession within four calendar quarters.

According to Huebschmann and Montzka, “The yield curve is the slope of the line between short- and long-term interest rates. Most of the time the yield curve has a positive slope because longer-term investments (e.g., two- to 30-year bonds) normally command higher interest rates than short-term investments (e.g., three- and six-month T-bills). However, every so often – as was the case between late 2006 and early 2007 (Figure E1) – the yield curve inverts as investors foresee higher risk levels in the short run. Based on historical correlations, the risk of recession increases as the 10-year yield drops against the three-month yield.”

Three quarters later, in December of 2007, we were in a recession.

The above figure shows yields, as of 1:30pm EST on 8 March 2007, on U.S. Treasuries with maturity dates ranging from three months to 30 years (line chart); and the magnitude of change from the yields 15 minutes previous (bar chart). Source: Bloomberg.com

Learn more about Forest2Market Timber Price Forecasts.

Forest2Market Launches new Websites in Finnish, Swedish & Russian

Forest2Market, Inc., a global provider of data solutions for the forest products industry, announced today the launch of its newly-redesigned...

Forest2Market Launches Enhanced, Redesigned English and Portuguese Websites

Forest2Market announced today the launch of its newly-redesigned English and Portuguese websites. These refreshed websites offer improved navigation,...

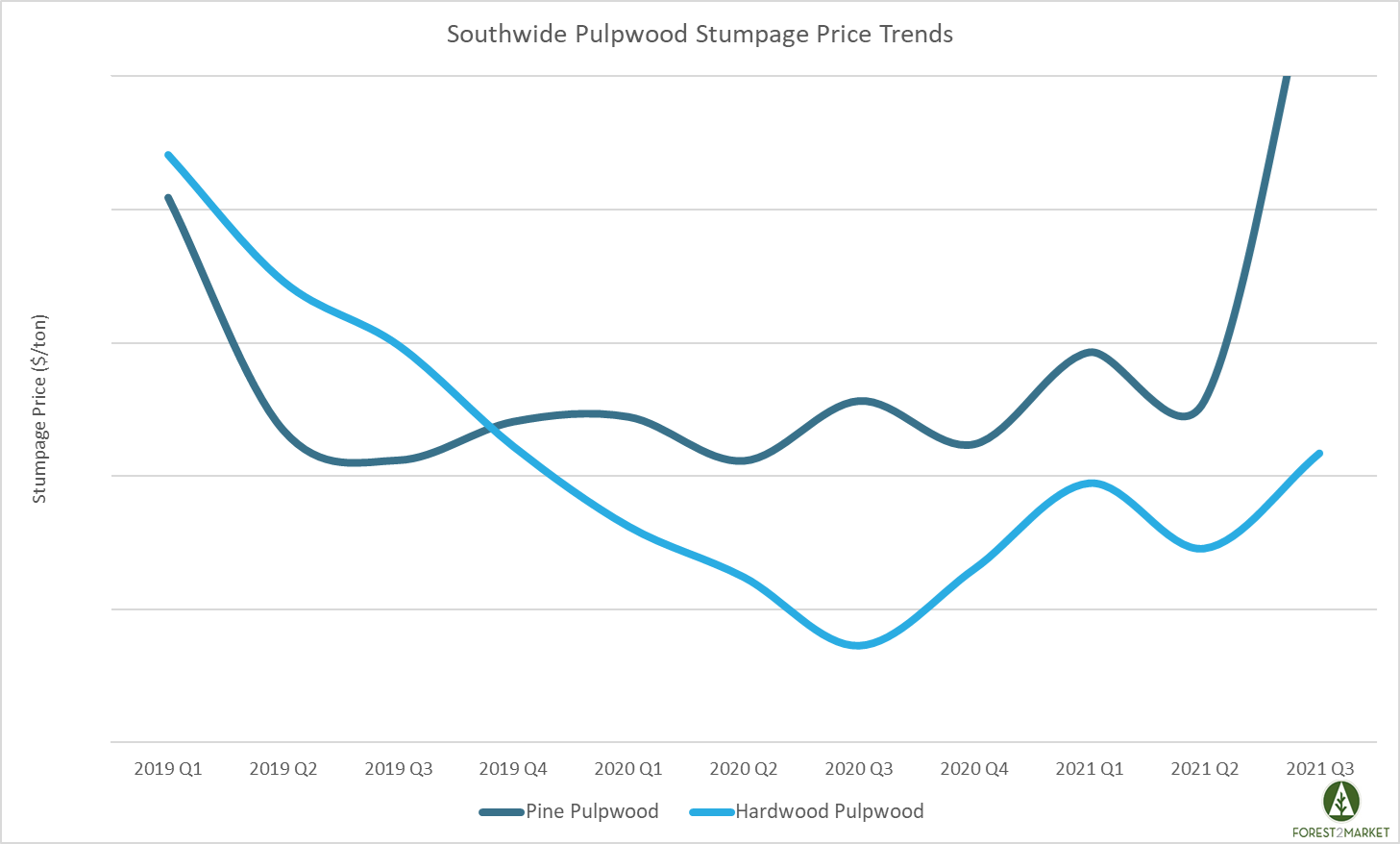

Southern Timber Prices Hit 14-Year High

Led by insatiable demand for small pine and hardwood logs, the weighted average price for southern timber surged to a 14-year high in 3Q2021....