3 min read

We are approaching the high temperatures and peak fire season of mid-summer, and there are a number of ongoing developments and considerations for those involved in the Pacific Northwest log market trade. As I travel through the territory and discuss day-to-day operations and changing trends with Forest2Market customers and seasoned industry veterans, the conversations typically involve at least one of the following topics: fires, inventories and exports/imports. And in this industry, all three of these topics are closely connected; an imbalance in one area may dramatically affect another.

Fires

-

Number of fires burning: As of this writing, four major active fires are burning along with several other minor incidents in the Inland and Coastal PNW regions. The local fire outlook is “elevated” in most areas, a month earlier than usual due to the exceptionally low humidity, the unpredictable weather patterns and the record low snow pack last winter.

-

Fire restrictions: Existing fires or fire threats have the potential to quickly change harvesting schedules. Access to acreage, logging roads and permits can be cut off due to fire threats, and this will affect both the local logging economy as well as the larger timber market.

-

Increased fire danger: Fires have the potential to destroy forest acreage, wildlife, man-made structures and entire communities. The cost of fighting fires is astronomical (over the last 10 years, the Forest Service has spent an average of $1.13 billion on annual suppression operations). When an increased risk of fire exists, it is actually a good time to have logging contractors in woods (albeit, at a reduced activity level) to respond to fire outbreaks quickly.

Inventories

-

Logs and chips: Current inventories are at some of the highest levels we have seen in recent years. If and when the tide will turn depends on weathering supply constraints—both human- and nature-related.

-

Reduced harvests: Large landowners are reducing harvest levels as prices drop; however, savvy sellers are using Forest2Market’s forecasting intelligence to capitalize on this trend by timing offerings and keeping logging infrastructures intact.

-

Mill closures and curtailments: The West End area’s last production lumber mill recently shuttered, and three other local mills have closed within the last year. As this trend continues, what will be the net effect on inventories and the larger the log trade?

-

Seasonality: Q3 has historically seen the highest log volume being traded due to favorable logging conditions, though often at softened prices. Mills could potentially rely on the level of log trade to build for an upcoming (and typically rainy) Q4 and Q1. But is this strategy feasible this year with reduced volumes being harvested? Also worth consideration is the number of currently-idle logging contractors; mills must take measures now so as not to get caught unprepared in a market upswing.

Imports/Exports

-

Export prices: Prices are down but exporters are accepting lower margins to protect market positions and investment in port facilities. Truly opportunistic operations have all but disappeared with the plan of reappearing when market margins increase.

-

Imports: Log importers are currently benefitting from the strong US dollar. While US housing starts continue to disappoint (hampering domestic production), Canadian lumber imports have remained healthy. With the already-extended Softwood Trade Agreement set to expire in October, could this development provide a boost for domestic producers?

-

China: When analyzing ship schedules across the region, the Chinese market for PNW timber is holding steady. In fact, ships are currently being loaded in areas where they haven’t seen much recent activity. While not as strong as 2014, when there was a 9% increase in log and lumber exports to China, new housing restrictions and unfavorable exchange rates are affecting current exports to China. 2015 will not be a total bust, but we won’t see the kind of growth we have witnessed in that market over the last few years. Still, China will continue to prefer the durability of PNW logs over southern hemisphere fiber.

PNW Regional Outlook

As the regional forest products industry temporarily slows during the summer fire season, the real “fiber at risk” is the the supply of residual saw chips for the pulp and paper sector. As mentioned above, current mill curtailments and closures coupled with log availability tensions could create some market challenges in Q4 and beyond. At the very least, these developments could be the catalyst for creating sustainable fiber procurement discussions. In the near term, the region will see an increased demand for both traditional and chip-n-saw fiber to augment available residual chip volumes. And as always, fires and the ever-changing weather in the PNW will continue to affect harvests and, by extension, domestic and global timber markets alike.

2Q2010 Pine Sawtimber Prices Delivered to Sawmills in the South

Pine sawtimber inventories at mills dropped in the first quarter of 2010, despite heightened lumber demand. As a result of this imbalance, pine...

Product Feature: Forestry Consultant Uses Forest2Market’s Small Business Pricing Service

At the Crossroads of North Mississippi, Tom Vigour of Vigour Forestry Consulting, Inc. does what he’s been doing for decades. As a consulting...

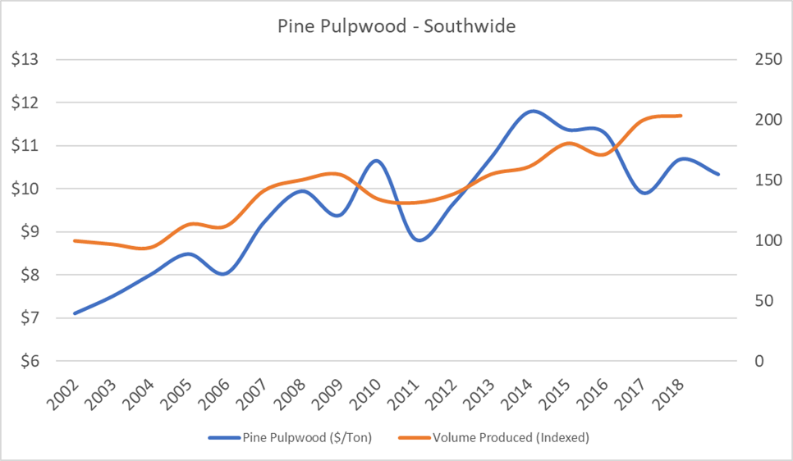

Pine Pulpwood: Driving the Southern Timber Price Rebound

We are more than a decade removed from the depths of the Great Recession and despite 10 years of solid growth, timber prices across the South have...